What is financial due diligence: a protocol for Corporate Asset owners

Many South African SMB owners believe financial due diligence is optional or too complex for smaller deals. Yet 70-80% SME failure rates underscore how critical it is to verify financial health before acquisitions. Without proper due diligence, hidden liabilities, tax shortcuts, and inaccurate earnings can destroy investments. This guide explains what financial due diligence is, why it matters, and how South African SMB owners can apply it to protect their capital and make smarter investment decisions.

Table of Contents

- Key takeaways

- What is financial due diligence and why it matters

- Core methods used in financial due diligence

- Financial due diligence focus areas for South African SMBs

- Common pitfalls and real risks of skipping financial due diligence

- Empower your financial decisions with professional accounting help

- How long does financial due diligence typically take?

- Can small business owners perform financial due diligence themselves?

- What are the biggest risks uncovered by financial due diligence in South Africa?

- How can financial due diligence findings affect deal pricing?

Key Takeaways

| Point | Details |

|---|---|

| Due Diligence Importance | Verifying financial health before acquisitions helps prevent hidden liabilities and costly losses. |

| Three Core Docs | The process analyzes profit and loss, balance sheets, and cash flow while cross checking bank statements, tax returns, and operational records. |

| Earnings Normalization and Tax | Normalizing earnings removes one time items and owner perks to reveal sustainable profitability while confirming VAT, PAYE, and SARS compliance to uncover hidden liabilities. |

| Local SA Risks | In South Africa SMBs must address local risks such as SARS compliance and owner dependence to avoid overestimating value after a deal. |

| Expert Teams Advantage | Expert teams and specialized tools improve due diligence accuracy and increase confidence to negotiate better terms or walk away. |

What is financial due diligence and why it matters

Financial due diligence is a detailed investigation of a target company’s financial statements, trends, forecasts, cash flows, debts, taxes, and working capital to verify accuracy, identify risks, normalize earnings, and support deal pricing in acquisitions or investments. It goes far beyond simply reviewing numbers on a balance sheet. The process reconstructs the true financial reality of a business by examining multiple years of data, typically three or more, to spot patterns, anomalies, and red flags.

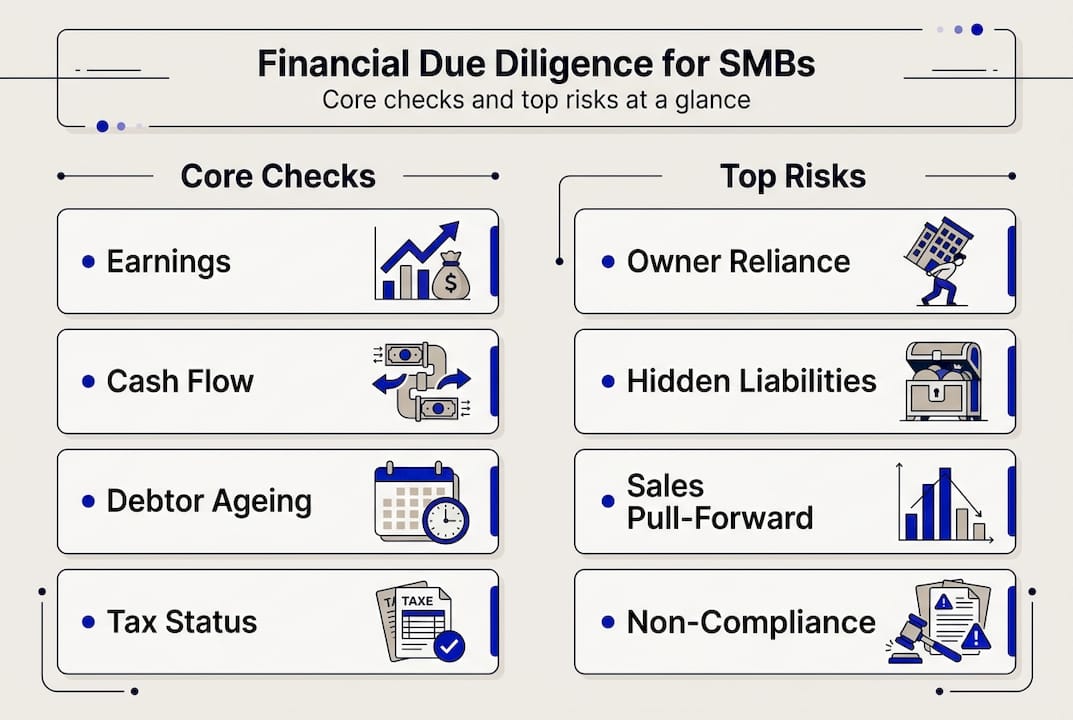

Professional due diligence teams analyze three core financial documents. Profit and loss statements reveal revenue trends, cost structures, and profitability patterns. Balance sheets expose asset quality, debt levels, and liquidity positions. Cash flow statements show whether the business generates actual cash or relies on accounting adjustments to appear profitable. Each document must be cross-referenced against bank statements, tax returns, and operational records to validate reported figures.

The process focuses heavily on normalizing earnings. This means stripping out one-time events, related party transactions, and owner perks to reveal sustainable profitability. For example, if an owner paid themselves below market salary or charged personal expenses to the business, adjustments must reflect true economic costs. Similarly, non-recurring gains from asset sales or insurance claims get removed to show ongoing operational performance.

Tax compliance verification forms another critical pillar. Teams examine VAT returns, PAYE submissions, and SARS correspondence to confirm the business meets all obligations. Unpaid taxes or aggressive interpretations of tax law create hidden liabilities that can explode after acquisition. Understanding how to read financial statements helps buyers spot inconsistencies between reported profits and tax filings.

The ultimate goal is accurate deal pricing. Due diligence findings directly impact valuation by revealing true earnings power, necessary working capital, and risk adjustments. A business claiming R5 million in profit might only generate R3 million after normalizations, dramatically changing what a buyer should pay. Expert teams provide buyers with leverage to renegotiate terms or walk away from bad deals.

“Financial due diligence transforms opaque financial claims into verified facts, giving buyers the confidence to proceed or the wisdom to retreat before committing capital.”

Core methods used in financial due diligence

Professional due diligence relies on several proven methodologies, each designed to uncover specific risks and validate financial claims. Understanding these techniques helps SMB owners know what to expect and how to prepare.

-

Quality of Earnings analysis: This examines whether reported profits come from sustainable operations or temporary factors. Analysts review revenue recognition policies, expense timing, and accounting choices to assess earnings quality. High-quality earnings come from repeatable customer transactions, not one-time events or aggressive accounting.

-

EBITDA normalization: Teams adjust earnings before interest, taxes, depreciation, and amortization to reflect true operating performance. This removes owner compensation adjustments, related party transactions, non-recurring items, and discretionary expenses. Core methodologies include QoE analysis, EBITDA normalization, working capital assessment, KPI review, and reconstructing revenues from bank deposits and tax returns.

-

Working capital evaluation: Analysts calculate the capital needed to run daily operations by examining accounts receivable, inventory, and accounts payable cycles. Insufficient working capital means buyers must inject cash immediately after closing to keep operations running.

-

Key performance indicator review: Beyond financial statements, teams analyze operational metrics like customer retention rates, gross margin trends, employee turnover, and sales pipeline health. These indicators reveal business momentum and sustainability.

-

Revenue reconstruction: Perhaps the most powerful technique, this involves matching reported sales to actual bank deposits and tax filings. Discrepancies signal potential fraud, cash skimming, or inaccurate record keeping.

The R.E.M.A.P. framework provides a systematic approach: reconstruct reality from source documents, evaluate sustainability of earnings and operations, map all identified risks with financial impact, assess people and operational dependencies, and prepare comprehensive findings for decision making.

| Method | Primary focus | Key outcome |

|---|---|---|

| Quality of Earnings | Revenue and profit sustainability | True operational profitability |

| EBITDA normalization | Adjusting for non-recurring items | Comparable earnings power |

| Working capital analysis | Cash conversion cycle | Capital requirements post-deal |

| KPI review | Operational health metrics | Business momentum assessment |

| Revenue reconstruction | Validating reported sales | Fraud detection and accuracy |

Pro Tip: Engage multidisciplinary teams including finance professionals, tax advisors, and legal experts to cover all risk angles effectively. Tax compliance expertise proves especially valuable in South African contexts where SARS issues can derail deals.

Financial due diligence focus areas for South African SMBs

South African SMBs face unique compliance and operational risks that demand special attention during due diligence. Local regulations, enforcement patterns, and business practices create specific vulnerabilities that buyers must scrutinize.

For South African SMBs, focus on poor governance, tax shortcuts, B-BBEE compliance, VAT/PAYE/UIF obligations, and owner-dependent earnings using three years of audited financials and asset condition assessments. SARS compliance tops the risk list. Many smaller businesses take shortcuts on tax reporting, delay VAT payments, or misclassify workers to reduce PAYE obligations. These practices create massive hidden liabilities. A single SARS audit can uncover years of unpaid taxes plus penalties and interest, wiping out deal value.

Specific tax areas requiring verification include:

- VAT registration status and timely filing of returns

- PAYE compliance for all employees and contractors

- UIF contributions and proper worker classification

- Corporate income tax returns matching financial statements

- Withholding taxes on payments to non-residents

Governance weaknesses plague many SMBs. Lack of board oversight, poor internal controls, and mixing personal and business finances create operational risks. Buyers must assess whether systems exist to prevent fraud, ensure accurate reporting, and maintain compliance after the owner exits.

Owner dependence represents another critical risk. If the business relies entirely on the current owner’s relationships, expertise, or daily involvement, value may evaporate post-acquisition. Due diligence must evaluate customer concentration, employee capabilities, and operational documentation to assess transferability.

B-BBEE compliance affects deal structure and future operations. Buyers need to verify current B-BBEE certification levels, understand how ownership changes impact scoring, and assess reliance on government contracts or corporate clients with supplier requirements. Avoiding tax penalties requires understanding both current compliance status and historical issues.

Financial documentation requirements include three years of audited or independently reviewed financial statements. Buyers should verify asset conditions through physical inspections, especially for equipment, inventory, and property. Contracts with customers, suppliers, and employees need review to confirm terms, expiration dates, and change of control provisions.

| Risk category | Specific checks | Red flags |

|---|---|---|

| SARS compliance | VAT, PAYE, UIF, income tax | Outstanding assessments, late filings |

| Governance | Internal controls, segregation of duties | Owner approval for all transactions |

| B-BBEE | Current certification, contract dependencies | Expired certificates, heavy government reliance |

| Owner dependence | Customer relationships, operational knowledge | Single point of failure for key functions |

| Financial quality | Audited statements, asset verification | Qualified opinions, obsolete inventory |

Cash flow analysis deserves special emphasis. A business might show accounting profits while burning cash due to aggressive revenue recognition, slow collections, or inventory buildup. Post-acquisition solvency depends on positive operating cash flow, not just reported earnings. VAT compliance directly impacts cash flow through timing of input claims and output obligations.

Pro Tip: Prepare clean, audited financial statements well before seeking funding or buyers. This accelerates due diligence, builds confidence, and often results in better deal terms. Professional preparation signals operational maturity and reduces buyer risk perception.

Common pitfalls and real risks of skipping financial due diligence

Rushing or skipping financial due diligence exposes buyers to catastrophic risks. Understanding common pitfalls helps SMB owners recognize red flags and avoid costly mistakes.

Edge cases and pitfalls include owner dependence, cash accounting quirks, customer concentration over 30%, pulled-forward sales, aging debtors, auditor qualification issues, and hidden tax liabilities. Each represents a potential deal killer if not identified and addressed before closing.

Owner dependence manifests in multiple ways. The owner might be the primary salesperson, technical expert, or relationship manager for key accounts. Without transition planning and knowledge transfer, revenue can collapse immediately after acquisition. Smart buyers assess whether documented processes, capable staff, and diversified relationships exist to sustain operations.

Cash accounting creates distorted financial pictures. Businesses using cash basis accounting might recognize revenue when collected rather than when earned, making seasonal patterns difficult to assess. They may also fail to record accrued expenses or contingent liabilities. Converting to accrual accounting during due diligence often reveals lower true profitability.

Pulled-forward sales represent a particularly insidious risk. Desperate sellers sometimes offer deep discounts or extended terms to boost revenue before a sale. This creates an artificial spike in reported sales followed by a post-acquisition cliff. Analyzing monthly sales patterns and customer payment terms helps detect this manipulation.

Aging debtors signal collection problems or revenue recognition issues. If significant receivables exceed normal payment terms, they may be uncollectible. This reduces actual cash available and may require write-offs that impact post-acquisition profitability. Tax compliance reviews often uncover mismatches between reported sales and collected cash.

Auditor qualifications in financial statements should trigger immediate deep dives. When auditors express concerns about going concern status, material misstatements, or scope limitations, buyers face elevated risk. These qualifications mean even professionals couldn’t verify financial accuracy.

Hidden tax liabilities lurk in many SMB acquisitions. Outstanding SARS assessments, disputed positions, or aggressive deductions can create massive unexpected costs. Buyers may inherit these liabilities depending on deal structure, making thorough tax due diligence essential.

Customer concentration above 30% creates vulnerability. Losing one or two major clients can devastate revenue. Due diligence must assess contract terms, relationship strength, and likelihood of retention post-acquisition.

“One luxury property buyer ignored due diligence warnings about structural issues and regulatory violations, resulting in over €2 million in unexpected repairs and legal costs within the first year. The property value dropped 40% before issues were resolved.” Luxury property case study

Site visits and third-party verification provide crucial validation. Physically inspecting operations, interviewing key employees, and speaking with major customers reveals realities that financial statements miss. Professional advisors bring objectivity and experience to spot warning signs that emotionally invested buyers overlook.

Empower your financial decisions with professional accounting help

Navigating financial due diligence requires expertise, objectivity, and local knowledge. Ready Accounting specializes in helping South African SMBs maintain clean financial records, ensure tax compliance, and prepare for growth opportunities. Our cloud accounting solutions provide real-time visibility into financial performance, making due diligence preparation seamless. Whether you’re preparing your business for sale or evaluating acquisition targets, our team delivers the financial clarity needed for confident decisions. We combine deep tax compliance expertise with practical business advisory to help you avoid costly mistakes. Explore our guides on reading financial statements to strengthen your financial literacy and make informed strategic choices.

How long does financial due diligence typically take?

How long does financial due diligence typically take?

Financial due diligence duration varies from two weeks for simple SMB transactions to three months for complex deals with multiple entities or international operations. The timeline depends on financial record quality, business complexity, identified issues requiring investigation, and responsiveness of sellers and advisors. Buyers should build adequate time into deal schedules to avoid rushed analysis that misses critical risks.

What does financial due diligence cost?

Costs range from R50,000 for basic SMB reviews to R500,000 or more for comprehensive engagements involving multiple advisors and extensive analysis. While significant, these fees represent insurance against much larger losses from bad acquisitions. Most buyers view due diligence as an essential investment that typically pays for itself through better deal terms, risk mitigation, or avoiding disastrous transactions. Tax compliance verification alone often uncovers liabilities exceeding advisory fees.

What happens if due diligence uncovers major problems?

Buyers have several options when due diligence reveals significant issues. They can renegotiate purchase price downward to reflect identified risks, require sellers to fix problems before closing, structure earnouts or holdbacks to protect against undisclosed liabilities, or terminate the transaction entirely if risks outweigh benefits. Professional advisors help quantify financial impact and negotiate appropriate remedies or adjustments.

What is the difference between buyer and seller due diligence?

Buyer due diligence focuses on validating seller claims, identifying risks, and supporting valuation decisions to protect the buyer’s investment. Seller due diligence, often called vendor due diligence, involves sellers proactively investigating their own business before marketing it. This accelerates transactions, builds buyer confidence, and allows sellers to address issues on their own timeline rather than under deal pressure. Both perspectives add value to transaction processes.

Can small business owners perform financial due diligence themselves?

Can small business owners perform financial due diligence themselves?

While owners can conduct preliminary reviews using checklists and financial statement analysis guides, professional expertise proves essential for thorough risk assessment. Accountants, tax advisors, and legal professionals bring objectivity, technical knowledge, and experience spotting red flags that owners miss. The complexity of normalizing earnings, verifying tax compliance, and assessing legal risks typically exceeds owner capabilities. Most successful acquisitions involve professional due diligence teams.

What are the biggest risks uncovered by financial due diligence in South Africa?

What are the biggest risks uncovered by financial due diligence in South Africa?

Common risks include tax non-compliance like SARS shortcuts, owner-dependent earnings, hidden liabilities, aggressive revenue recognition, and poor governance. Tax issues top the list because many SMBs take shortcuts that create massive exposure. Owner dependence follows closely, as businesses often cannot sustain performance without the current owner’s involvement. Tax compliance verification frequently reveals years of accumulated risk that sellers either ignored or actively concealed.

How can financial due diligence findings affect deal pricing?

How can financial due diligence findings affect deal pricing?

Buyers often use due diligence disclosures to renegotiate offers, adjust valuation for risk, or walk away from bad deals. Identified issues translate directly into price reductions, earnout structures, or indemnification provisions. For example, discovering R1 million in unpaid taxes typically reduces purchase price by at least that amount plus a risk premium. Normalized earnings adjustments similarly impact valuation multiples. Due diligence provides factual basis for negotiation rather than subjective opinions, giving buyers leverage to achieve fair pricing that reflects true business value and risk.

Recommended

- What are financial statements: guide for South African SMBs – Ready Accounting

- Financial Statement Basics: A Guide for Business Owners – Ready Accounting

- How to Read Financial Statements: Easy Guide for 2025 – Ready Accounting

- Examples of financial statements for South African SMEs – Ready Accounting

- Build Custom Business Software Without Long-Term Debt