What is a valid tax invoice: essential 2026 protocol

Many South African business owners believe handwritten invoices are automatically invalid, but SARS rules prove otherwise. If your invoice contains the right elements, format matters less than content. This guide clarifies SARS requirements for valid tax invoices, explains invoice types based on transaction value, and provides practical checklists to help you issue compliant invoices, claim input VAT correctly, and avoid costly penalties.

Table of Contents

- Understanding SARS Tax Invoice Requirements

- Full Vs Abridged Tax Invoices: When And What To Issue

- Elements Of A Valid Tax Invoice

- Consequences Of Non-Compliance With SARS Requirements

- Common Mistakes And Misconceptions About Tax Invoices

- Practical Checklist For SMEs To Issue Valid Tax Invoices

- Future Trends: Electronic Invoicing And SARS Mandates

- How Ready Accounting Supports Your Tax Invoice Compliance

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Legal compliance | Valid tax invoices must comply with SARS VAT Act Section 20 requirements to enable input VAT deductions. |

| Invoice types | Choose full, abridged, or no invoice based on transaction value thresholds to meet SARS rules efficiently. |

| Timing matters | Issue invoices within 21 days of supply date to maintain eligibility for input VAT claims and avoid compliance issues. |

| Non-compliance risks | Invalid invoices trigger input VAT denial and penalties up to 200% of unpaid VAT amounts. |

| Practical tools | Use checklists and cloud accounting software to verify invoice validity before issuing and reduce manual errors. |

Understanding SARS tax invoice requirements

South Africa’s VAT system requires tax invoices for input deduction purposes with specific prescribed details under VAT Act Section 20. These documents serve as proof of VAT paid on purchases, allowing registered vendors to claim input tax credits against output VAT collected from customers.

SARS mandates that vendors issue a tax invoice within 21 days of the supply date. This timing ensures accurate VAT accounting and prevents delays in input deduction claims. Without a valid tax invoice, you cannot legally deduct input VAT, regardless of whether you genuinely paid tax on the purchase.

The key principles governing tax invoices include:

- All VAT vendors must issue compliant invoices for taxable supplies

- Invoice validity depends on content accuracy, not format or medium

- Buyers need valid invoices to claim input VAT on their returns

- SARS uses invoices to verify VAT collection and prevent fraud

These requirements create a paper trail that supports transparent VAT administration. When planning your year-end tax strategy, ensuring invoice compliance protects your input tax claims and reduces audit risk. The detailed SARS guidelines specify exactly what information must appear on invoices to satisfy legal standards.

Full vs abridged tax invoices: when and what to issue

SARS uses a three-tier system that matches invoice complexity to transaction size. This approach balances compliance with practical business needs. Understanding which invoice type applies to each sale prevents unnecessary paperwork while maintaining VAT compliance.

For supplies exceeding R5,000 VAT inclusive, you must issue a full tax invoice containing comprehensive supplier and recipient details. This includes both parties’ names, physical addresses, and VAT registration numbers. Full invoices provide complete audit trails for high-value transactions.

Abridged invoices apply to transactions between R50 and R5,000, allowing you to omit recipient details like the buyer’s name, address, and VAT number. This simplified format speeds up retail and small-scale B2B transactions without compromising VAT tracking.

For supplies of R50 or less, no formal invoice is required, though you must provide a till slip or sales docket showing VAT charged. These minimal requirements reduce administrative burden on micro-transactions while still documenting VAT for input claims.

| Invoice type | Transaction value | Required details | Typical use |

|---|---|---|---|

| Full tax invoice | Above R5,000 incl. VAT | Full supplier and recipient info, VAT numbers, addresses | Wholesale, equipment, professional services |

| Abridged invoice | R50 to R5,000 incl. VAT | Supplier details only, no recipient info required | Retail sales, small B2B purchases |

| Till slip/docket | R50 or less incl. VAT | Supplier VAT number, VAT amount shown | Coffee shops, stationery, fuel |

Pro tip: Match your invoice type precisely to the transaction value. Issuing full invoices for small sales wastes time, while using abridged formats for large transactions violates SARS rules and invalidates input claims.

This tiered system lets you scale invoice complexity with transaction importance. Reviewing your small business tax deductions becomes easier when invoices follow the correct format. Refer to the complete SARS guide for detailed breakdowns of each invoice type.

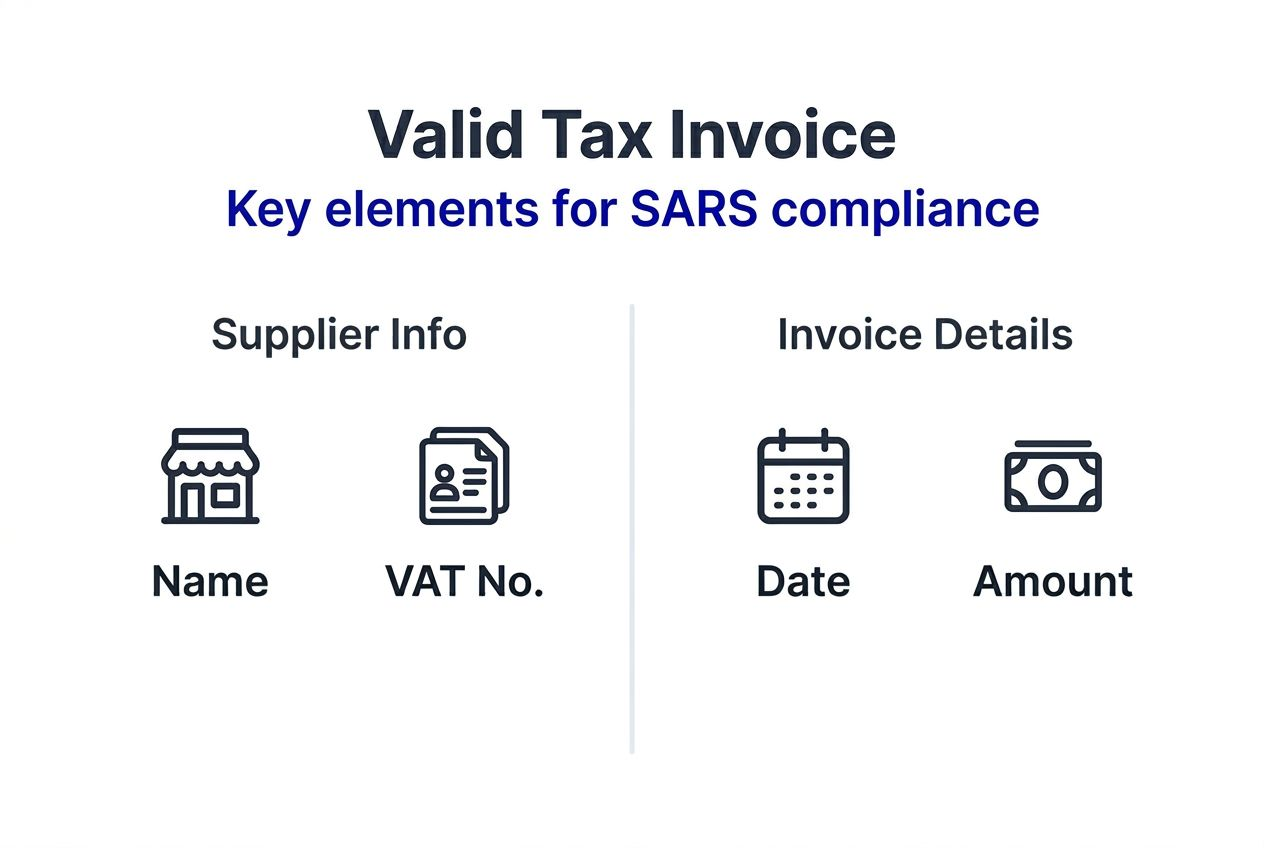

Elements of a valid tax invoice

Every valid tax invoice must contain specific fields that SARS uses to verify VAT transactions. Missing even one element can disqualify your input claim, so understanding these requirements is critical for compliance.

A valid tax invoice must include these core elements: the words ‘Tax Invoice’, supplier’s full name and address, VAT registration number, invoice number, date of issue, description of goods or services, quantity, value, and VAT charged. Each field serves a verification purpose during SARS audits.

The mandatory fields include:

- Document title: Must state ‘Tax Invoice’ or ‘VAT Invoice’ prominently

- Supplier information: Full legal name, physical address, and VAT registration number

- Recipient details: Name, address, and VAT number (full invoices only)

- Invoice number: Unique sequential identifier with no duplicates or gaps

- Date of issue: The day the invoice was created, not the supply date

- Supply description: Clear description of goods or services provided

- Quantity and pricing: Number of units and unit price for each line item

- VAT calculation: 15% VAT amount shown separately from the base price

- Total amount: Final price inclusive of VAT

The VAT amount must be distinctly displayed so buyers can verify the exact tax paid. Simply showing a VAT-inclusive total without breaking out the 15% component fails SARS requirements. This separation is crucial for accurate input tax calculations.

Your invoice numbering system must be sequential and permanent. You cannot skip numbers or reuse identifiers, as gaps suggest missing transactions that trigger audit flags. Following proper SARS record-keeping practices ensures your numbering system withstands scrutiny.

Both electronic and paper invoices are acceptable if they contain these elements. The medium does not matter, content does. Review the full mandatory field requirements to ensure your templates cover every necessary detail.

Consequences of non-compliance with SARS requirements

Issuing invalid tax invoices carries serious financial and operational risks that extend beyond immediate VAT claim denials. Understanding these consequences motivates rigorous compliance practices.

Failure to comply invalidates input VAT claims, meaning you lose the right to deduct VAT paid on purchases. This creates an immediate cash flow hit, as you must fund the full VAT liability without offsetting input credits. For businesses with thin margins, this can be devastating.

Penalties can reach 200% of the VAT value when SARS determines willful non-compliance or fraud. Even unintentional errors attract penalties starting at 10% of the tax shortfall. These fines multiply quickly across multiple invalid invoices, creating substantial unexpected liabilities.

Non-compliance significantly increases your audit risk. SARS flags vendors with frequent invoice errors for detailed examinations, diverting your time and resources into responding to queries and providing documentation. Audits can extend months and disrupt normal business operations.

Other consequences include:

- Delayed or denied VAT refunds when your input claims are questioned

- Reputational damage with suppliers and customers who doubt your professionalism

- Accumulated interest charges on unpaid VAT amounts

- Potential criminal prosecution in cases of deliberate fraud

Invalid invoices do not just cost you immediate VAT deductions. They create cascading compliance issues that expose your business to penalties, audits, and cash flow disruptions that can threaten operational stability.

Maintaining strict VAT compliance protects you from these risks. The investment in proper invoicing systems pays dividends through avoided penalties and smoother SARS interactions. Review the detailed penalty structures to understand the full scope of non-compliance costs.

Common mistakes and misconceptions about tax invoices

Many South African SMEs hold incorrect beliefs about tax invoices that lead to compliance failures. Clearing up these misconceptions helps you avoid preventable errors.

Handwritten invoices can be valid if they meet SARS content rules. The misconception that only printed or digital invoices qualify causes businesses to reject legitimate handwritten documents. Format does not determine validity, content does.

Some believe all sales require full tax invoices, but abridged or no invoice applies depending on transaction value. This misunderstanding creates unnecessary administrative work for small sales and risks over-documentation that obscures important records.

Common mistakes include:

- Omitting VAT registration numbers for either supplier or buyer on full invoices

- Incorrect VAT calculations that do not precisely show 15% of the base amount

- Missing invoice numbers or using non-sequential numbering systems

- Failing to state ‘Tax Invoice’ on the document, leaving status ambiguous

- Not issuing invoices within 21 days, causing input claim timing issues

- Believing electronic invoices are invalid, contradicting SARS acceptance of digital formats

- Overlooking till slip validity for purchases below R50, missing legitimate input claims

Electronic invoices are fully accepted under current rules, with SARS planning mandatory e-invoicing by 2028. The belief that digital formats lack legal standing prevents businesses from adopting efficiency-boosting technology.

Till slips satisfy requirements for transactions under R50, yet many SMEs discard these documents or fail to retain them for input claims. This leaves money on the table through unclaimed VAT deductions.

Address these misconceptions by consulting authoritative resources and asking common tax questions before making assumptions. Education prevents costly compliance errors.

Practical checklist for SMEs to issue valid tax invoices

A systematic verification process ensures every invoice you issue meets SARS standards before it reaches your customer. This checklist approach significantly reduces VAT rejection risk and penalties.

Follow these steps for each invoice:

-

Verify all mandatory fields are present: Check that your invoice includes the document title, both parties’ details (if required), invoice number, date, supply description, pricing breakdown, VAT amount, and total.

-

Confirm VAT registration number validity: Ensure your VAT number and the recipient’s number (for full invoices) are current and correctly formatted. Invalid numbers trigger automatic claim rejections.

-

Ensure unique sequential numbering: Check that the invoice number follows your previous invoice without gaps or duplicates. Maintain a log to track number assignment.

-

Issue within 21 days of supply date: Mark your calendar for the supply date and issue the invoice promptly. Late invoices can disqualify input claims for your customers.

-

Calculate and display VAT separately: Break out the 15% VAT amount on a separate line. Never show only a VAT-inclusive total without the component calculation.

-

Retain copies for five years minimum: Store invoice copies following SARS record-keeping regulations. Use cloud backup to prevent data loss.

-

Match invoice type to transaction value: Apply full, abridged, or no invoice requirements based on the R50 and R5,000 thresholds.

Pro tip: Use cloud accounting software templates that pre-populate required fields and automatically calculate VAT. This eliminates manual errors and ensures consistent compliance across all invoices.

Integrating this checklist with your year-end tax planning streamlines audit preparation. Regularly review your invoicing process against the official SARS checklist to catch emerging issues early. Connecting your invoicing to your complete tax deductions strategy maximizes your VAT position while maintaining full compliance.

Future trends: electronic invoicing and SARS mandates

Electronic invoicing becomes mandatory around 2028 as SARS introduces real-time reporting to improve tax compliance and audit accuracy. Understanding this shift helps you prepare infrastructure and processes now.

The upcoming e-invoicing mandate will require:

- Real-time invoice submission to SARS through certified service providers

- Standardized electronic formats replacing varied paper and digital styles

- Interoperability between your accounting system and SARS platforms

- Digital signatures and authentication to prevent tampering

- Automated VAT validation catching errors before invoice finalization

SARS expects e-invoicing to dramatically reduce manual errors and create instant audit trails. The system will flag discrepancies in real time, preventing invalid invoices from circulating. This shift moves compliance from periodic checks to continuous verification.

Early adoption benefits include:

- Smoother SARS audits with instant access to validated invoice data

- Faster VAT refund processing through automated verification

- Reduced administrative burden once initial setup is complete

- Competitive advantage in B2B relationships requiring digital integration

SMEs should begin preparing by adopting cloud accounting platforms that support electronic invoicing standards. This positions you ahead of the 2028 mandate and reduces future migration costs. Review the complete e-invoicing mandate guide to understand technical requirements and timeline details.

While mandatory implementation remains two years away, proactive preparation prevents last-minute scrambles and system disruptions. The transition to e-invoicing represents a fundamental shift in VAT administration that will define compliance practices for decades.

How Ready Accounting supports your tax invoice compliance

Navigating SARS invoicing requirements becomes simpler with expert guidance and automated systems. Ready Accounting provides South African SMEs with tailored solutions that ensure VAT compliance while reducing administrative overhead.

Our cloud accounting platforms automate valid invoice generation with pre-built templates that include all mandatory SARS fields. You avoid manual errors and ensure consistent compliance across every transaction. The system updates automatically when regulations change, protecting you from outdated practices.

We help you implement practical checklists that catch invoice issues before they reach customers. Our team reviews your invoicing workflows, identifies common mistakes, and designs verification processes aligned with your business operations. This proactive approach prevents the penalties and audit complications that arise from non-compliance.

Ready Accounting supports seamless VAT input tax claims by ensuring your purchase invoices meet SARS record-keeping standards. We organize documentation for five-year retention, prepare audit-ready files, and maximize your legitimate tax deductions. Our expertise transforms compliance from a burden into a competitive advantage that enhances your financial efficiency and confidence.

Frequently asked questions

What is a valid tax invoice in South Africa?

A valid tax invoice meets all SARS VAT Act Section 20 requirements, including the document title ‘Tax Invoice’, both parties’ details, VAT registration numbers, unique invoice number, supply description, and 15% VAT shown separately. Without these elements, the invoice cannot support input VAT claims.

Can I use handwritten invoices for my business?

Yes, handwritten invoices are valid if they contain all mandatory SARS fields. Format does not determine compliance, content does. Ensure your handwritten documents include every required element before issuing them to customers.

How long do I have to issue a tax invoice after making a sale?

You must issue a tax invoice within 21 days of the supply date. Missing this deadline can disqualify your customer’s input VAT claim and expose you to compliance penalties. Set calendar reminders to ensure timely invoice generation.

What happens if my invoice is missing the VAT registration number?

An invoice missing the supplier’s or recipient’s VAT registration number (on full invoices) is invalid and cannot support input tax deductions. SARS will reject the claim, and you may face penalties. Always verify VAT numbers before finalizing invoices.

Do I need a full tax invoice for every sale?

No, invoice type depends on transaction value. Full invoices apply above R5,000 inclusive VAT, abridged invoices for R50 to R5,000, and till slips for R50 or less. Using the correct type based on value ensures compliance without unnecessary complexity.

Are electronic invoices accepted by SARS?

Yes, SARS accepts electronic invoices that contain all mandatory fields. Digital formats offer the same legal standing as paper invoices. With mandatory e-invoicing planned for 2028, adopting electronic systems now prepares you for future requirements.

Recommended

- Top Tax Questions Small Business Owners Ask in 2025 – Ready Accounting

- Year-End Tax Planning Guide for Small Businesses – Ready Accounting

- The Ultimate VAT Compliance Guide for South African Small Businesses in 2025 – Ready Accounting

- How to Prepare for Tax Season: Essential Steps for 2025 – Ready Accounting

- International Shipping Documentation: A Complete Guide for Businesses – ORNER

- Business Validation Guide for New Founders | siift.ai in 2026