Understanding auditing: a guide for South African SMEs

Executive Summary

- Many South African SME owners believe auditing is only necessary for large or listed companies, but it is essential for building credibility with banks, investors, and regulators. An audit provides independent verification of financial statements, which enhances trust and helps meet legal requirements based on your Public Interest Score. The process involves risk assessment, sampling, and issuing an opinion, but it offers reasonable assurance rather than absolute certainty, and the quality depends on the auditor’s independence, competence, and communication.

Many South African SME owners assume auditing is reserved for listed companies, government entities, or multinationals with hundreds of employees. That assumption is costly. An official professional examination of your financial statements does far more than satisfy a legal checkbox — it builds the kind of credibility that opens doors with banks, attracts investors, and protects your business from regulatory exposure. This guide breaks down what auditing really means for your business, when it applies, and how to use it strategically rather than reluctantly.

Table of Contents

- What auditing means for South African SMEs

- Types of audits and legal requirements in South Africa

- What auditors actually do: The process explained

- Limitations of audits: What they do — and don’t — guarantee

- What is audit quality — and why does it vary?

- A practical perspective: What SME owners should really take away from auditing

- Enhance your SME’s financial management with expert support

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Auditing builds trust | Audits offer independent assurance to stakeholders and boost business credibility. |

| Legal rules vary | Whether you need an audit depends on South African legal thresholds like your company’s Public Interest Score. |

| Audits have limits | Audits aim for reasonable assurance but may not catch all errors or fraud, so set proper expectations. |

| Audit quality matters | Choosing a skilled, ethical auditor impacts the value you actually get from the process. |

| Owner mindset is key | Using audit feedback proactively helps drive business improvement, not just compliance. |

What auditing means for South African SMEs

Auditing is not simply about checking whether the numbers add up. It is an independent, evidence-based process where a registered professional examines your financial records and confirms whether they are fairly presented and comply with applicable standards. The key word is independent. Your accountant helps produce your financial statements; an auditor independently verifies them. These are fundamentally different roles, and understanding the difference between accountant and auditor is the first step to navigating your obligations correctly.

“An audit is an official, professional examination of an organisation’s financial statements and records to provide assurance on whether they are fairly presented and comply with applicable standards and regulations.”

For SME owners, this matters in very practical ways. When you apply for business finance, a bank’s credit committee wants confidence in your numbers. When a potential partner or investor evaluates your business, they want assurance your financials reflect reality. Even your suppliers and key clients may assess your financial credibility before entering long-term contracts. An audit provides that assurance in a way that self-prepared or accountant-prepared statements simply cannot.

Common misconceptions worth addressing:

- Audits only apply to large companies. Not true. Your legal structure, shareholder composition, and Public Interest Score determine whether you need one.

- An audit means your accountant has made mistakes. Auditing is verification, not accusation. It confirms accuracy, not incompetence.

- Auditors check every single transaction. They use sampling and risk-based approaches, which we will cover in detail shortly.

- Passing an audit means your business is financially healthy. An audit opinion confirms fair presentation, not profitability or sustainability.

Maintaining financial integrity with ethical accounting practices lays the groundwork that makes any audit process smoother and more credible. If your records are inconsistent or your internal controls are weak, auditors will identify those risks and your audit opinion may reflect that.

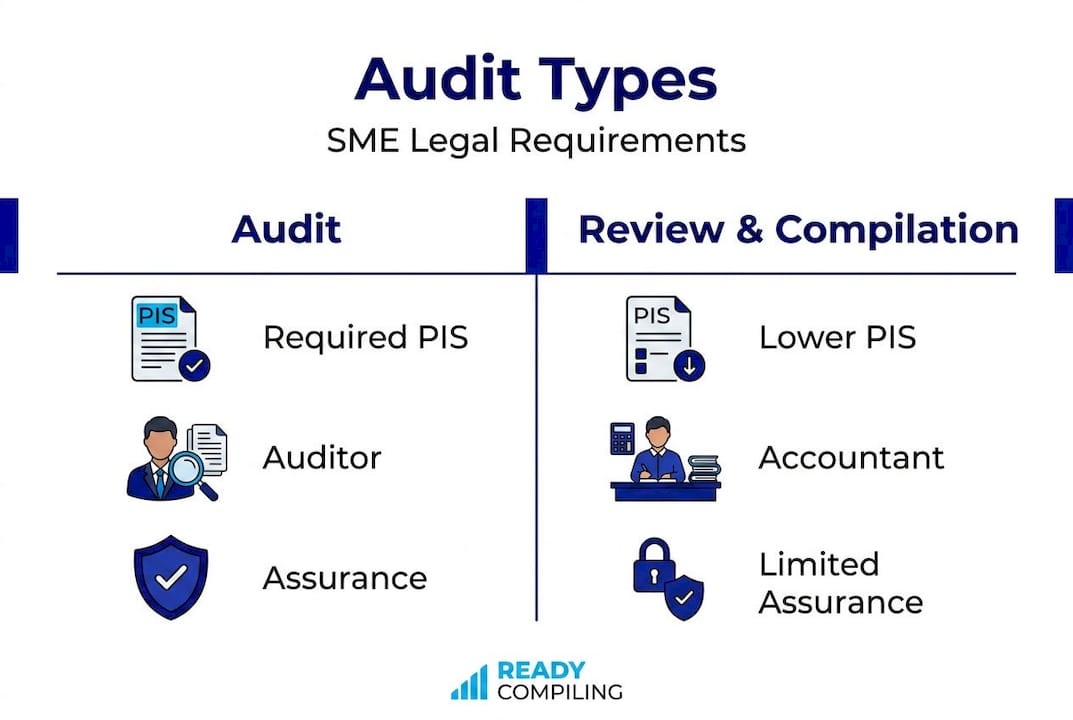

Types of audits and legal requirements in South Africa

Understanding what triggers an audit under South African law is genuinely important because the consequences of getting it wrong include regulatory penalties and reputational damage. The Companies Act audit requirements are structured around a Public Interest Score system that most SME owners have never heard of.

Here is how the three tiers of financial reporting requirements compare for private companies:

| Requirement | When it applies | Who performs it |

|---|---|---|

| Audit | PIS of 350 or more, or if MOI requires it | Registered auditor (IRBA registered) |

| Independent review | PIS between 100 and 349, or if MOI requires it | Registered accountant or auditor |

| Compilation only | PIS below 100 and all shareholders are directors | Accounting officer or accountant |

Your Public Interest Score is calculated using four factors: the number of employees (1 point per employee), third-party liabilities in millions of rands (1 point per R1 million), turnover in millions (1 point per R1 million), and the number of individuals who have a beneficial interest in the company’s securities. A business with 50 employees, R10 million in turnover, and R5 million in third-party liabilities already sits at 65 points before counting shareholders.

Pro Tip: Always check your Memorandum of Incorporation (MOI). Even if your PIS falls below the audit threshold, a poorly drafted or standard-template MOI may contain a clause requiring an annual audit regardless. Many SMEs unknowingly commit to annual audit costs simply because they never reviewed this document when incorporating.

The legal framework governing how audits are conducted matters too. South Africa’s registered auditors apply ISAs.pdf) and South African guidance practice statements set by the Independent Regulatory Board for Auditors (IRBA). This alignment with international standards means that an audit opinion from a South African registered auditor carries credibility with international investors and financial institutions.

Steps to determine your compliance requirement:

- Calculate your current Public Interest Score using the four factors above.

- Review your company’s MOI for any mandatory audit or independent review clauses.

- Check whether any shareholders, lenders, or major contracts require audited statements.

- Confirm whether your registered accountant holds the right qualifications for an independent review if that is your threshold.

- Engage with a professional who understands the annual financial statements requirements in South Africa before your financial year closes.

Understanding whether you need an audit, an independent review, or a compilation is not just about saving costs. It is about being correctly positioned for the level of scrutiny your business actually faces from banks, investors, and regulators.

What auditors actually do: The process explained

When an external auditor examines records, tests internal controls, gathers evidence, and issues an opinion, it follows a structured methodology that most SME owners have never seen from the inside. Knowing what to expect removes anxiety and helps you prepare properly.

Here is what the audit process typically looks like for an SME:

- Planning and risk assessment. Auditors begin by understanding your business, industry, and control environment. They identify key risks — areas where material misstatements are most likely to occur.

- Internal control evaluation. They assess whether your processes and controls are designed and operating effectively. Weak controls increase the risk of material misstatement.

- Substantive testing. This is the fieldwork phase. Auditors request supporting documents, reconciliations, contracts, and bank statements to verify balances and transactions.

- Sampling. Not every transaction is reviewed. Auditors use statistical and judgmental sampling to draw conclusions about the entire population from a representative subset.

- Fraud risk procedures. Under updated standards, auditors apply specific procedures to assess fraud risk, not just error. We cover this in more detail in the next section.

- Finalisation and opinion. Once testing is complete, auditors issue an audit report expressing one of four opinions: unmodified (clean), qualified, adverse, or disclaimer of opinion.

| Audit opinion | What it means for your business |

|---|---|

| Unmodified | Financial statements are fairly presented. Strongest outcome. |

| Qualified | Statements are fairly presented except for specific issues identified. |

| Adverse | Statements are materially misstated overall. Serious consequence. |

| Disclaimer | Auditor could not obtain sufficient evidence to form an opinion. |

An unmodified opinion does not mean zero errors exist. It means no material misstatements were found. The concept of materiality is central to understanding auditing financial statements protocols. Auditors define a materiality threshold — often a percentage of revenue or total assets — and errors below that threshold may not affect the opinion even if detected.

Pro Tip: Prepare a complete audit file before your auditors arrive. This should include signed bank reconciliations, a fixed asset register, all loan agreements with outstanding balances, a debtors and creditors age analysis, and management accounts for the year. Every hour an auditor spends chasing documents is an hour you pay for at professional rates.

The role distinction between your accountant and auditor becomes very visible during this phase. Your accountant provides the records; your auditor interrogates them. Both roles serve your business, but they must remain independent of each other for the audit to have any credibility.

Limitations of audits: What they do — and don’t — guarantee

This is where many SME owners feel let down after their first audit experience. They expect the process to uncover every irregularity, reconcile every discrepancy, and essentially act as an internal investigation. That is not what an audit delivers.

Audits offer reasonable assurance, not absolute assurance. The distinction matters enormously. Reasonable assurance means a high but not absolute level of confidence that financial statements are free from material misstatement. Because auditors use sampling and risk-based testing, some errors and even some fraudulent transactions may not surface during a standard audit.

“Audits focus on material misstatement risk and may not detect every error or fraud because assurance is ‘reasonable’ and evidence is tested, often using sampling.”

This is not a flaw in the system. It is a practical, cost-effective approach to verification. Reviewing every single transaction in a business that processes thousands of entries monthly would be prohibitively expensive and still not guarantee absolute certainty.

That said, South Africa is tightening fraud-related expectations. IRBA adopted ISA 240 (Revised 2025) with stronger requirements around fraud risk assessment, requiring auditors to apply greater skepticism and more targeted procedures when fraud indicators exist. This is meaningful progress, but it does not transform audits into forensic investigations.

Key boundaries SME owners should understand:

- An audit is not a forensic investigation. If you suspect fraud, commission a forensic audit separately.

- An audit does not express an opinion on your business strategy or future viability.

- Auditors are not responsible for preparing or correcting your financial statements.

- An audit does not replace strong internal controls. Your first line of defence is always your own processes.

If your audit findings reveal consistent control weaknesses, recurring adjustments, or unusual transactions, treat that as signal, not noise. Those findings are often the most valuable output of the entire engagement.

What is audit quality — and why does it vary?

Two businesses of similar size, in the same industry, can have dramatically different audit experiences. One walks away with meaningful insights, clean documentation, and a process that strengthened their financial management. The other gets a generic report, a bill, and no lasting value. The difference is audit quality.

Interestingly, there is no single universally agreed definition of audit quality despite decades of global standards and regulation. What we do know is that high-quality audits consistently demonstrate several key characteristics:

- Independence: The auditor has no financial, personal, or business relationship that compromises objectivity.

- Competency: The engagement team understands your specific industry, applicable standards, and South African regulatory environment.

- Professional scepticism: Auditors actively question evidence rather than simply accepting explanations at face value.

- Communication quality: You receive timely, clear feedback about findings, not just a final signed report months after fieldwork.

- Ethical conduct: No shortcuts, no pressure to issue favourable opinions without sufficient evidence.

“Audit quality is a distinct topic: even with decades of standards and regulation, there is no single universally agreed definition of ‘audit quality.’”

Your involvement as a business owner also shapes audit quality. Owners who engage constructively, provide complete records promptly, and take management letters seriously consistently report better audit experiences and more useful outcomes. Audit quality is a two-way dynamic.

When selecting an auditor, ask about their experience with businesses in your sector, their IRBA registration status, and how they communicate findings during the year. Firms that only appear at year-end tend to deliver less value than those who maintain periodic contact with your team. Strong financial reporting integrity built throughout the year makes the audit itself faster, cleaner, and more insightful.

A practical perspective: What SME owners should really take away from auditing

Most business owners experience their first audit as a stressor. Documents disappear, queries multiply, and the final bill feels disproportionate to the outcome. But that experience usually reflects a misalignment in expectations, not a flaw in auditing itself.

The most valuable insight we can offer from working with scaling South African SMEs is this: treat your audit as a diagnostic, not a verdict. The process surfaces how your financial infrastructure actually performs under external scrutiny. If it struggles, that is information you need regardless of whether the auditor finds it.

Auditing should inform strategic decisions. When auditors identify that your revenue recognition is inconsistent, that your debtors are poorly controlled, or that your provisions are inadequately supported, those findings point directly to operational and financial risks that affect your growth trajectory. Most SME owners file the management letter and forget it. The ones who act on those findings systematically are the ones who come back twelve months later with cleaner books, stronger controls, and better financial insight.

There is also a trust dimension that is underappreciated. Audited financial statements are a form of credibility currency. In South Africa’s competitive funding environment, having audited statements when your peer businesses only have compiled statements is a measurable advantage when approaching banks, investors, or government procurement processes.

The owner mindset is also critical. Owners who view auditing as adversarial create friction that slows the process and often leads to more conservative audit opinions. Owners who view auditors as a second set of expert eyes on their business consistently extract more value from the same engagement. Shift the mindset from compliance to learning, and the return on your audit investment changes completely.

Understanding financial reporting as an ongoing strategic tool rather than a year-end obligation is what separates businesses that scale from those that stagnate.

Enhance your SME’s financial management with expert support

Audit readiness does not start the week before your auditors arrive. It is built into how your business records, classifies, and reports financial information every single month. At Ready Accounting, we replace manual, error-prone bookkeeping with cloud infrastructure and automated workflows that keep your financial records audit-ready throughout the year. When auditors arrive, your documentation is complete, your reconciliations are current, and your team is not scrambling. Our real-time dashboards also show you how automation improves cash flow visibility, which directly supports cleaner audit trails. If you want to improve financial reporting across your business while reducing the administrative burden, we are ready to build that infrastructure with you.

Frequently asked questions

Does my South African SME have to be audited every year?

It depends on your Public Interest Score threshold, your company’s legal structure, and any requirements in your MOI or shareholder agreements. Many small businesses fall below the audit threshold and may only require an independent review or compilation.

What is a Public Interest Score (PIS)?

PIS is a points-based compliance tool used under the South African Companies Act to determine whether your company requires a full audit, an independent review, or can simply compile financial statements without external verification.

Will an audit detect all fraud in my business?

No. Audits provide reasonable, not absolute assurance and rely on risk-based sampling, which means some fraud or errors may go undetected. If you suspect fraud specifically, a separate forensic audit is the appropriate response.

What main standards guide audits in South Africa?

South African registered auditors apply ISAs.pdf) alongside South African guidance practice statements issued by IRBA, ensuring alignment with international reporting requirements and local legal obligations.

How is an audit different from accounting or bookkeeping?

Bookkeeping and accounting produce your financial statements; auditing independently verifies those statements for accuracy, fair presentation, and compliance with applicable standards. They are complementary but distinctly separate functions.

Recommended

- Integrity in financial reporting: practical steps for SA SMEs | Ready Accounting

- Execution Framework: Audit Financial Records: Easy Protocol for SA Businesses | Ready Accounting

- Auditing financial statements: protocol for South African Corporate Assets | Ready Accounting

- Reporting irregularities: protect your SA business in 2026 | Ready Accounting