Tax implications of selling a business in south africa

Executive Summary

- Structuring a business sale as a share or asset transfer significantly impacts the applicable taxes in South Africa. Proper tax planning before signing agreements helps maximize proceeds by avoiding unnecessary VAT, transfer duties, or CGT liabilities. Early engagement with tax professionals ensures eligibility for exclusions and compliance, which can be crucial for deal success.

The tax implications of selling a business in South Africa are determined primarily by one decision: whether you structure the deal as a share sale or an asset sale. That single choice dictates whether you face capital gains tax (CGT) on shares or individual assets, whether VAT at 15% applies, and whether transfer duty becomes payable. The effective CGT rate is 18% for individuals and 21.6% for companies in the 2026/2027 fiscal year. Getting the structure right before you sign anything is not optional. It is the difference between walking away with the proceeds you planned for and handing a significant portion to SARS.

What are the capital gains tax rates when selling a business?

Capital gains tax is the most significant tax cost in most South African business sales. SARS calculates CGT by applying an inclusion rate to your capital gain, then taxing that included amount at your marginal income tax rate.

The inclusion rates and effective CGT rates for 2026 are as follows:

| Taxpayer Type | Inclusion Rate | Effective CGT Rate |

|---|---|---|

| Individual | 40% | 18% |

| Company | 80% | 21.6% |

| Trust | 80% | 36% |

Trusts face the highest effective rate at 36%. That figure should inform every trust-held business owner’s decision about sale timing and structure well before a buyer appears.

The r2.7 million lifetime exclusion for small business owners

The 2026 budget introduced a meaningful update for qualifying sellers. Individuals aged 55+ selling a small business with a market value up to R15 million can claim a lifetime CGT exclusion of R2.7 million. The qualifying threshold increased from R10 million to R15 million, bringing more businesses into eligibility.

This exclusion applies to the disposal of active business assets, not passive investments. You must be 55 or older, or dispose of the business due to ill health or other qualifying circumstances. If you meet the criteria, this exclusion can eliminate or dramatically reduce your CGT liability. A tax planning guide for 2026 outlines how to position your business to qualify before you go to market.

Pro Tip: If you are approaching 55 and considering a sale, delaying the transaction by even a few months to cross that age threshold could save you hundreds of thousands of rands in CGT.

How do share sales and asset sales differ in tax treatment?

The structural choice between a share sale and an asset sale carries fundamentally different tax consequences for both buyer and seller. Understanding these differences is the foundation of any sound selling a business tax advice.

Share sales: simpler for sellers, riskier for buyers

In a share sale, you sell your ownership stake in the company. CGT applies to the gain on the shares. Securities Transfer Tax at 0.25% applies on the transfer of shares, but no VAT and no transfer duty are triggered. The tax treatment is cleaner and generally more favorable for the seller.

The trade-off is that the buyer inherits the company’s full history, including any undisclosed tax liabilities, PAYE arrears, or VAT disputes. Share sales are more tax-efficient for sellers but require buyers to conduct extensive due diligence to protect themselves from inherited risk. That scrutiny often translates into longer negotiations and stronger warranty demands.

Asset sales: more complex, more taxes

In an asset sale, the company sells individual assets rather than shares. Each asset disposal can trigger its own CGT calculation. VAT at 15% applies to most asset transfers unless the going concern zero-rating applies. Transfer duty rates on immovable property range from 0% to 13%, calculated on the higher of market value or purchase price under the Transfer Duty Act 40 of 1949.

The key tax consequences in each structure are:

- Share sale: CGT on shares, Securities Transfer Tax at 0.25%, no VAT, no transfer duty

- Asset sale: CGT on individual assets, VAT at 15% (unless zero-rated), transfer duty on property, potential recoupment of depreciation taxed as income

Pro Tip: Sellers almost always prefer share sales. Buyers almost always prefer asset sales because they avoid inheriting historical liabilities. Your negotiating position determines which structure wins. Know your tax exposure in both scenarios before you enter that room.

What is the VAT treatment on a business sale in south africa?

VAT is where many South African business sales go wrong. The standard VAT rate of 15% applies to asset sales. On a R10 million transaction, that is R1.5 million in VAT. That cash flow impact can derail a deal if it is not planned for in advance.

The solution is the going concern zero-rating under section 11(1)(e) of the VAT Act. VAT at 15% applies unless the transaction meets specific going concern conditions. When those conditions are met, VAT is charged at 0%, eliminating the immediate cash flow burden.

Conditions required for going concern zero-rating

To qualify for VAT zero-rating as a going concern, all of the following must be true:

- Both the seller and the buyer must be registered VAT vendors

- The business must be an income-earning enterprise at the time of transfer

- All assets necessary for the business to continue operating must be included in the sale

- The sale agreement must explicitly state that the transaction is a going concern

Failing to meet these conditions often forces the seller to pay 15% VAT, with SARS commonly denying zero-rating when documentation is incomplete. The financial consequence is immediate and significant. If the buyer is not VAT-registered, zero-rating is unavailable regardless of any other conditions being met.

For sellers who are uncertain about their VAT registration status or eligibility, the VAT registration guide from Readyaccounting covers the criteria and compliance steps in detail.

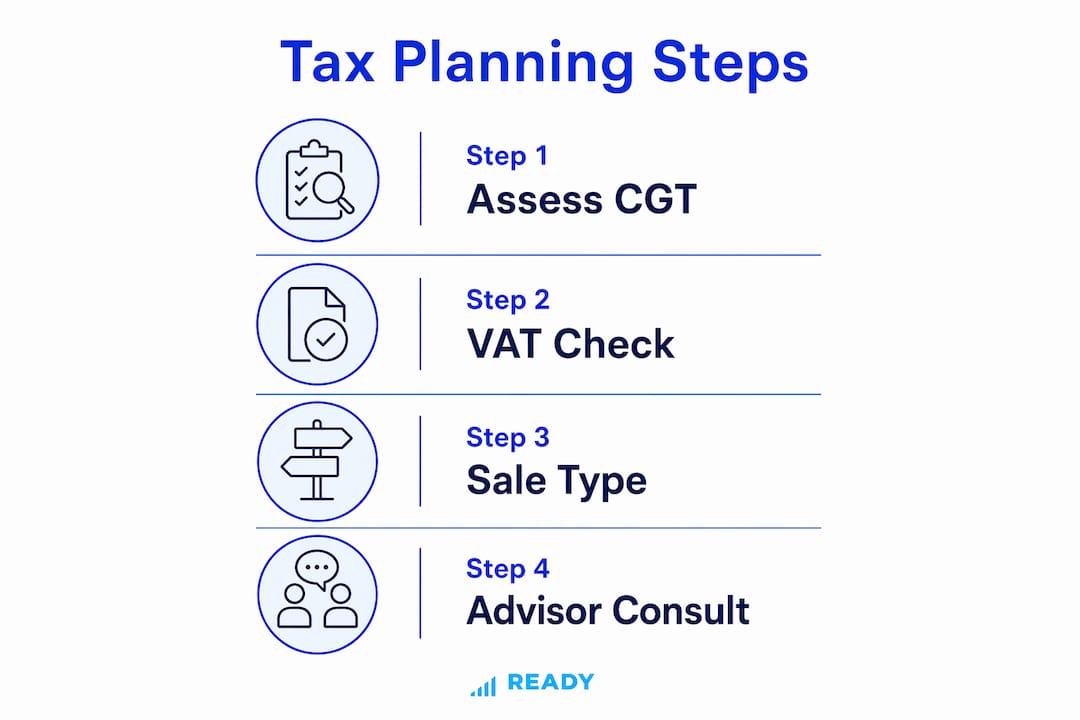

What tax planning steps should you take before selling your business?

Tax structuring needs to happen at the term sheet stage for optimal outcomes. Sellers who wait until the sale agreement is being drafted have already lost significant leverage and may face avoidable tax costs.

Here is the sequence that protects your proceeds:

-

Engage a tax advisor before any deal structure is agreed. The choice between share and asset sale, the timing of the transaction, and the allocation of purchase price across assets all affect your final tax bill. A qualified tax advisor can model the after-tax proceeds under each scenario before you commit.

-

Prepare audited financial statements and confirm SARS compliance. Accurate, audited financial records and up-to-date SARS compliance are non-negotiable before any sale. Buyers will conduct financial due diligence, and any gaps in your records or outstanding tax obligations will either kill the deal or reduce your price.

-

Include tax warranties and indemnities in the sale agreement. A tax indemnity clause is standard in South African buy-sell agreements. It protects buyers from latent tax liabilities relating to pre-closing periods, covering income tax, VAT, PAYE, SDL, UIF, dividends tax, penalties, and interest. As a seller, you need to understand exactly what you are indemnifying before you sign.

-

Document the going concern status if VAT zero-rating applies. Prepare the written agreement language explicitly, confirm both parties’ VAT registration, and verify that all operational assets are included in the transfer. Incomplete documentation is the most common reason SARS rejects zero-rating claims.

-

Run a full tax compliance check with your advisor. Confirm that all income tax returns, VAT returns, PAYE submissions, and provisional tax payments are current. Outstanding obligations surface during due diligence and give buyers grounds to reduce the purchase price or walk away.

Pro Tip: Ask your tax advisor to prepare a tax exposure memo before you approach buyers. It forces you to identify and resolve issues proactively rather than reactively during negotiations, where every problem costs you money.

Finding the right advisor matters as much as the timing. The guide to finding a tax consultant outlines what to look for when selecting someone to guide you through a transaction of this scale.

Key takeaways

Structuring a South African business sale correctly requires understanding CGT rates, VAT zero-rating conditions, and the tax consequences of share versus asset sales before any agreement is signed.

| Point | Details |

|---|---|

| Sale structure determines tax | Share sales trigger CGT and Securities Transfer Tax; asset sales add VAT at 15% and transfer duty. |

| CGT rates vary by taxpayer | Individuals pay 18%, companies 21.6%, and trusts 36% effective CGT in 2026. |

| R2.7 million exclusion available | Sellers aged 55+ with businesses valued under R15 million can claim a lifetime CGT exclusion. |

| VAT zero-rating requires strict compliance | Both parties must be VAT vendors, the business must be a going concern, and the agreement must state it explicitly. |

| Early tax planning protects proceeds | Engage a tax advisor at the term sheet stage to model after-tax outcomes before committing to a structure. |

The uncomfortable truth about selling a business and tax

I have worked with enough South African business owners through sale transactions to say this plainly: most sellers focus almost entirely on the headline price and almost nothing on the after-tax number. That is a costly mistake.

I have seen sellers lose hundreds of thousands of rands because they agreed to an asset sale without modeling the VAT and transfer duty consequences. I have seen going concern zero-rating claims rejected by SARS because the sale agreement did not include the required explicit wording. These are not edge cases. They are common outcomes when tax planning happens too late.

The deal success often depends more on tax structuring than price. A buyer offering R12 million in a share sale may deliver more to your pocket than a buyer offering R13 million in an asset sale, once you account for VAT, transfer duty, and the CGT differences. You cannot know that without running the numbers early.

My consistent advice is this: treat the tax structure as a non-negotiable part of your deal preparation, not an afterthought. Get your SARS compliance current, prepare audited financials, and understand your CGT exposure before you speak to a single buyer. Transparent negotiations, backed by clean financial records and clear indemnity language, protect both parties and close deals faster.

The sellers who walk away satisfied are the ones who prepared. The ones who feel shortchanged almost always say the same thing: “I wish I had spoken to someone sooner.”

— Johan

How Readyaccounting helps you sell with confidence

Readyaccounting works with South African business owners at every stage of a sale transaction. From modeling your CGT exposure under share versus asset sale structures to preparing audited financial statements that survive buyer due diligence, the team acts as your Fractional CFO through the entire process. Readyaccounting also guides sellers on VAT registration, going concern zero-rating eligibility, and the tax warranty language that protects you post-closing. If your financial records need to be sale-ready, the tax liability reduction service is the right starting point. You can also explore how automation improves cash flow visibility, giving buyers the real-time financial transparency that builds confidence and supports your asking price.

FAQ

What is the CGT rate for individuals selling a business in south africa?

The effective CGT rate for individuals is 18% in the 2026/2027 fiscal year, based on a 40% inclusion rate applied to the capital gain. Companies pay an effective rate of 21.6%, and trusts pay 36%.

Does VAT apply when selling a business in south africa?

VAT at 15% applies to asset sales unless the transaction qualifies for zero-rating as a going concern under section 11(1)(e) of the VAT Act. Both parties must be registered VAT vendors and the sale agreement must explicitly state the going concern status.

What is the lifetime CGT exclusion for small business owners?

Individuals aged 55 or older can claim a lifetime CGT exclusion of R2.7 million when selling a qualifying small business with a market value up to R15 million. This threshold increased from R10 million in the 2026 budget.

Are share sales or asset sales better for sellers in south africa?

Share sales are generally more tax-efficient for sellers because CGT applies only to the shares, with no VAT or transfer duty triggered. Asset sales attract VAT at 15% and transfer duty on immovable property, increasing the overall tax cost.

What does a tax indemnity clause cover in a south african sale agreement?

A tax indemnity clause protects the buyer from pre-closing tax liabilities, covering income tax, VAT, PAYE, SDL, UIF, dividends tax, penalties, and interest. It is standard in South African buy-sell agreements and should be reviewed carefully by both parties before signing.

Recommended

- Tax planning guide for South African SMEs in 2026 | Ready Accounting

- Top Tax Planning Strategies for South African Businesses 2025 | Ready Accounting

- Top Tax Questions Small Business Owners Ask in 2025 - Ready Accounting

- Tax efficient structures for South African Corporate Assets in 2026 | Ready Accounting