Tax efficient structures for South African Corporate Assets in 2026

Many South African SMB owners believe tax savings are out of reach or too complex to pursue. The truth is that proper tax structuring can save your business thousands of rands annually. South Africa offers specific tax frameworks designed for small businesses, including Small Business Corporation status and Turnover Tax. This guide explains these structures, who qualifies, and how to leverage them effectively for maximum benefit.

Table of Contents

- Key takeaways

- Understanding tax-efficient structures for small businesses

- Comparing small business tax options: SBC versus turnover tax

- Navigating nuances and compliance for effective tax structuring

- Practical steps to implement the right tax-efficient structure

- Explore expert accounting services for your SMB

- What is a tax efficient structure for small businesses?

Key Takeaways

| Point | Details |

|---|---|

| SBC advantages | SBC status provides graduated tax rates and accelerated depreciation, enabling growing businesses to reduce tax and deduct asset costs more quickly. |

| Turnover Tax option | Turnover Tax is a simplified levy for micro businesses with annual turnover up to R1 million, replacing income tax, provisional tax, and VAT. |

| Eligibility nuances | Your choice between SBC and Turnover Tax depends on criteria such as company type, turnover, shareholder structure, and investment income limits. |

| Proactive planning | Strategic timing of capital expenditure and proactive review of eligibility maximize the tax benefits offered by SBC and Turnover Tax. |

Understanding tax-efficient structures for small businesses

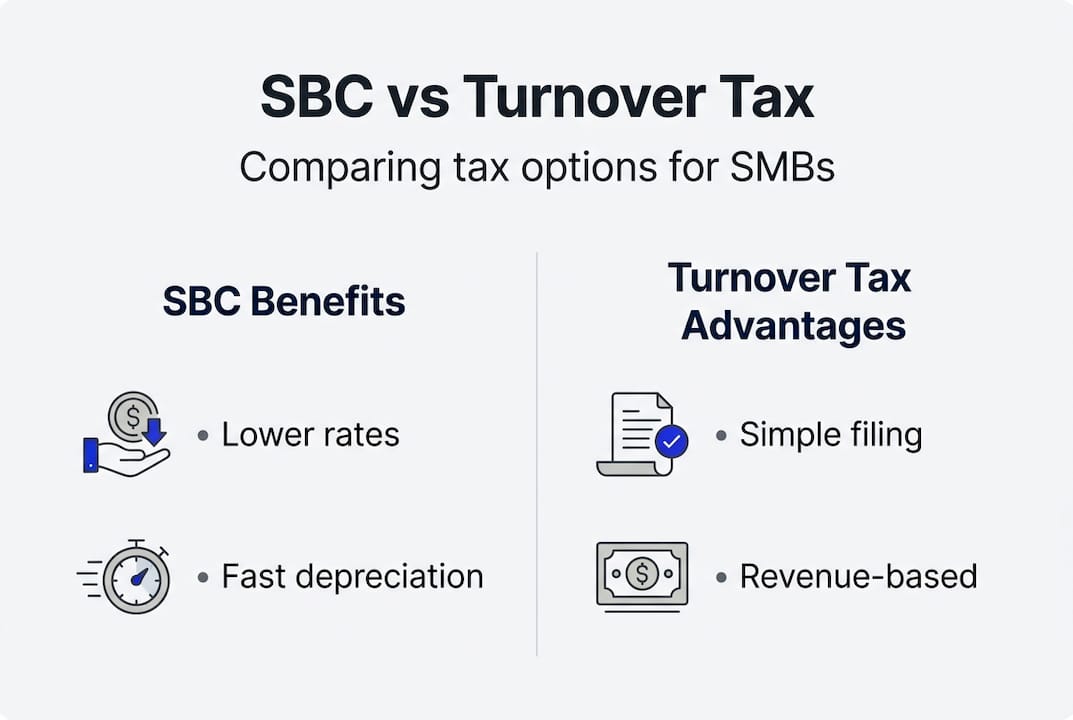

South African tax law provides two primary frameworks for small businesses. The Small Business Corporation (SBC) under Section 12E offers graduated tax rates and accelerated depreciation, making it attractive for growing companies. Turnover Tax serves micro businesses with annual revenue up to R1 million, replacing income tax, provisional tax, and VAT with a single simplified levy.

SBC status applies automatically if your company meets specific criteria. Your business must be a close corporation or private company with gross income below R20 million. All shareholders must be natural persons, and no more than 20% of income can come from investment or personal services. These small business tax guide requirements ensure the benefits reach genuine small enterprises.

Turnover Tax operates differently as an elective system. You choose to register and pay tax on gross revenue rather than profit. This eliminates the need for complex accounting since you calculate tax on total sales without deducting expenses. The system suits businesses with low overheads and simple operations.

Key eligibility requirements include:

- Annual turnover must not exceed R1 million

- Business cannot have more than one owner or controlling group

- No other tax registrations like VAT or employees’ tax allowed

- Cannot operate as a company, trust, or partnership

Accelerated depreciation under SBC status lets you write off assets faster than standard rates. New equipment, vehicles, and technology purchases reduce taxable income immediately rather than spreading deductions over many years. This benefit works best when you time capital expenditure strategically before year end.

Comparing small business tax options: SBC versus turnover tax

The tax savings difference between SBC and standard corporate rates is substantial. SBC saves up to R91,000 in tax at higher income levels compared to standard rates, making it valuable for profitable small companies. Standard corporate tax applies a flat 27% rate to all taxable income, while SBC uses graduated brackets that protect lower earnings.

| Income bracket | SBC rate | Standard rate | Your savings |

|---|---|---|---|

| R0 to R95,750 | 0% | 27% | R25,853 |

| R95,751 to R365,000 | 7% | 27% | R53,850 |

| R365,001 to R550,000 | 21% | 27% | R11,100 |

| Above R550,000 | 27% | 27% | R0 |

Turnover Tax uses its own rate schedule based on gross revenue. A business earning R500,000 annually pays just R5,500 in tax, calculated at 1% on the portion between R335,001 and R500,000. The first R335,000 is tax free, making this extremely beneficial for micro enterprises. Compare this to SBC where the same business might pay significantly more after accounting for expenses and profit margins.

Despite these advantages, low awareness and misconceptions limit Turnover Tax adoption despite its simplicity. Many owners worry about losing future tax benefits or misunderstand eligibility rules. Others fear SARS scrutiny or believe the system is temporary. These concerns prevent thousands of qualifying businesses from accessing legitimate savings.

Common disqualifiers that block SBC status:

- Investment income exceeds 20% of total revenue

- Personal service income dominates business activities

- Shareholders include trusts, companies, or foreign entities

- Gross income surpasses R20 million threshold

Accelerated depreciation provides immediate cash flow benefits. Standard depreciation spreads a R100,000 equipment purchase over five years at R20,000 annually. SBC allows full deduction in year one for qualifying assets, reducing taxable income by the entire amount immediately. This timing advantage improves working capital and funds reinvestment faster.

Pro tip: Review your SBC eligibility every February before year end. If you are approaching the R20 million gross income limit or planning to bring in corporate investors, structure these changes to preserve benefits for the current tax year. Timing matters because disqualification applies for the entire year, not just from the date you exceed limits.

The choice between SBC and Turnover Tax depends on your profit margins and administrative capacity. High margin businesses with significant expenses benefit more from SBC since tax applies only to profit. Low margin, high turnover operations may prefer Turnover Tax despite paying on gross revenue, because administrative simplicity reduces accounting costs. Run the numbers with your smart tax saving strategies to determine your optimal path.

Navigating nuances and compliance for effective tax structuring

Personal service provider (PSP) classification kills SBC eligibility instantly. SBC disqualification occurs with >20% investment income, PSP status, or insufficient employees. SARS defines PSPs as businesses where services are rendered personally by owners or connected persons, and those individuals would be employees if the company did not exist. Consulting, legal, medical, and creative services commonly face this restriction.

You can overcome PSP disqualification by employing three or more full time employees who are not connected persons throughout the year. Connected persons include family members, business partners, and entities you control. The employees must perform genuine work, not exist solely to meet the threshold. SARS audits these arrangements closely, so maintain proper employment contracts, payroll records, and PAYE submissions.

Record keeping requirements extend well beyond tax filing. Owners must track 5 to 7 year records for SARS compliance, covering all financial transactions, supporting documents, and tax submissions. This includes invoices, receipts, bank statements, asset registers, and correspondence with SARS. Digital records are acceptable if you maintain proper backups and can produce them on demand.

The annual eligibility retest happens automatically each tax year. Your SBC status is not permanent; you must qualify fresh every year based on the prior year’s results. A single year of excessive investment income or gross revenue over R20 million removes all benefits for that period. You cannot retroactively claim SBC treatment after year end if you failed to monitor compliance during the year.

Critical compliance steps to maintain eligibility:

- Track gross income monthly to avoid exceeding R20 million threshold

- Monitor investment income as a percentage of total revenue

- Document employee headcount and payroll for PSP exemption

- Review shareholder structure before admitting new investors

- File accurate financial statements supporting SBC claims

- Retain all source documents for the required retention period

Pro tip: Schedule a mid year tax review with your accountant in December. This timing lets you make corrective moves before February year end, such as deferring investment income, accelerating deductible expenses, or restructuring shareholder arrangements. Waiting until March when financials are final eliminates planning opportunities.

“The difference between tax avoidance and tax evasion is the thickness of a prison wall. Proper structuring within the law saves money; cutting corners creates liability.”

Penalties for incorrect SBC claims are severe. SARS charges understatement penalties up to 200% of the tax shortfall for intentional disregard of tax laws. Even negligent errors attract 25% to 50% penalties. These amounts compound with interest, turning a R50,000 tax saving into a R150,000 liability quickly. Your tax penalty prevention tips should include professional review before claiming special status.

Turnover Tax compliance is simpler but still requires diligence. You file returns every six months and pay tax on actual revenue received. The system prohibits registered vendors from claiming input VAT or deducting any expenses. Once you elect Turnover Tax, you must remain in the system for at least one full year unless you exceed the R1 million threshold or cease operations.

Maintaining SARS record keeping rules protects you during audits. SARS can request records up to five years after assessment, or indefinitely if they suspect fraud. Cloud accounting systems automatically timestamp and backup transactions, providing audit trails that paper systems cannot match. This digital evidence proves transaction dates, amounts, and authenticity when questions arise.

Practical steps to implement the right tax-efficient structure

Start by calculating your effective tax rate under each system. Take your last year’s financials and apply SBC graduated rates to taxable income, then compare against Turnover Tax applied to gross revenue. Include the value of accelerated depreciation by estimating your planned capital expenditure and calculating the tax saving from immediate deduction versus standard rates.

Register for Turnover Tax through SARS eFiling within 60 days of starting business or converting from another tax system. The online process requires your ID number, business details, and estimated annual turnover. SARS approves most applications within 21 business days if you meet eligibility criteria. You cannot backdate registration, so timing matters if you want benefits from your business start date.

SBC status applies automatically when you file your first company tax return, provided you meet all requirements. You do not register separately; simply complete the SBC section of your ITR14 return and claim the graduated rates. SARS may query your claim and request supporting documents, so prepare evidence of shareholder structure, income sources, and employee details before filing.

Capital expenditure timing dramatically affects your tax position. Purchasing a R200,000 vehicle in February versus March shifts R54,000 in tax deductions between years for SBC companies using accelerated depreciation. Plan major acquisitions to maximize immediate deductions in high income years, or defer them to years when you need deductions to stay within SBC thresholds.

Eligibility checklist for SBC status:

- Gross income below R20 million in prior year

- All shareholders are natural persons

- Investment income under 20% of total income

- Not classified as personal service provider, or employ 3+ full time staff

- Registered as close corporation or private company

- No shareholders hold more than 20% in another company

Turnover Tax registration requirements:

- Annual turnover does not exceed R1 million

- Sole proprietor or individual operating business

- No existing VAT, PAYE, or other tax registrations

- Not operating as partnership, company, or trust

- Business activities qualify under permitted categories

Proactive consultation and use of SARS eFiling is key for successful TOT registration and SBC eligibility checks. Tax professionals identify disqualifiers you might miss and structure transactions to preserve benefits. A R5,000 consultation fee is minor compared to R50,000 in annual tax savings or avoiding R100,000 in penalties from incorrect claims.

Ongoing compliance best practices include monthly management accounts to track income against thresholds, quarterly reviews of shareholder structure and income sources, annual depreciation schedules for asset purchases, and immediate consultation when business changes might affect eligibility. Your year end tax planning guide should incorporate SBC status verification as a standard checklist item.

Document your tax position contemporaneously. When you make decisions based on tax considerations, record the analysis, calculations, and reasoning in writing. This documentation proves to SARS that you acted reasonably and in good faith if they later challenge your position. Courts and tax tribunals give significant weight to contemporaneous records versus reconstructed explanations created during audits.

Integrate tax structuring with your overall tax compliance guide processes. Tax efficiency is not a one time decision but an ongoing management function. Review your structure annually, adjust as your business grows, and maintain the discipline to track compliance metrics monthly rather than scrambling at year end.

Explore expert accounting services for your SMB

Navigating tax efficient structures becomes simpler with professional support. Cloud accounting benefits include real time income tracking, automated compliance alerts, and instant access to financial data for tax planning decisions. These systems flag when you approach SBC thresholds or Turnover Tax limits, giving you time to respond strategically.

Ready Accounting specializes in helping South African SMBs optimize their tax positions while maintaining full compliance. Our team provides proactive tax compliance guide services, year end planning, and ongoing monitoring to preserve your SBC status or Turnover Tax benefits. We handle the technical details so you can focus on growing your business with confidence.

Whether you need help selecting the right structure, registering with SARS, or managing ongoing compliance, Ready Accounting financial services delivers tailored solutions for your specific situation. Book a consultation to discover how much you could save through proper tax structuring and professional financial management.

What is a tax efficient structure for small businesses?

A tax efficient structure is a legal business framework that minimizes your tax liability while maintaining full compliance with SARS regulations. For South African SMBs, this typically means qualifying for Small Business Corporation status or electing Turnover Tax instead of standard corporate tax rates. The right structure depends on your revenue, profit margins, ownership composition, and administrative capacity.

These structures are not loopholes but deliberate incentives created by government to support small business growth. Using them appropriately is smart tax planning, not tax avoidance. The key is understanding eligibility rules and maintaining proper records to support your claims.

How does the Small Business Corporation (SBC) status reduce tax liability?

SBC offers tax rates as low as 0% on first R95,750 and accelerated asset depreciation, creating immediate savings compared to the standard 27% corporate rate. The graduated rate structure protects lower income brackets, so a business earning R300,000 in taxable income pays just R14,297 in tax versus R81,000 under standard rates.

Accelerated depreciation lets you deduct the full cost of qualifying assets immediately rather than spreading deductions over multiple years. This timing benefit improves cash flow and reduces taxable income in high earning years when tax savings deliver maximum value.

Who qualifies for Turnover Tax and when is it beneficial?

Turnover Tax applies to micro businesses with turnover up to R1 million and is calculated on gross revenue. Only sole proprietors qualify; companies, trusts, and partnerships are excluded. You cannot have any other tax registrations like VAT or employees’ tax while using this system.

Turnover Tax works best for service businesses with minimal expenses and simple operations. A consultant earning R600,000 annually with few deductible costs pays R7,833 in Turnover Tax versus potentially R50,000 or more under SBC after accounting for limited expense deductions. The administrative simplicity alone saves thousands in accounting fees. Check our top tax questions for SMBs for more guidance.

What common pitfalls should SMB owners avoid when choosing tax structures?

Misunderstanding disqualifiers and poor compliance cause SBC disqualification and penalties. The most frequent error is failing to monitor investment income as a percentage of total revenue. Exceeding 20% investment income for even one year eliminates SBC status for that entire period, creating unexpected tax bills.

Personal service provider classification catches many professional service firms by surprise. Without three full time employees, your consulting or professional practice likely cannot claim SBC benefits. Plan your staffing and structure before assuming eligibility.

Maintain comprehensive records for the full retention period. SARS audits can reach back five years, and missing documentation shifts the burden of proof to you. Digital systems with automated backups provide the best protection. Review our guide to avoid tax penalties for complete prevention strategies.