Strengthen agency risk management for SMEs and startups

Executive Summary

- Agency risk affects businesses of all sizes by causing financial leakage, record distortion, and tax exposure. Managing it involves defining clear roles, implementing monitoring controls, and aligning incentives to minimize information asymmetry and operational mistakes. Regular review, automation, and stage-appropriate controls help South African SMEs build resilient, trustworthy financial systems.

Agency risk is not a boardroom problem reserved for listed companies with armies of compliance officers. It quietly drains cash, distorts financial records, and creates tax exposure in businesses of every size. For South African SME owners and VC-backed founders, the gap between what you expect from your team and what actually happens with your money is often where growth quietly dies. This guide breaks down practical, right-sized frameworks for identifying, measuring, and controlling agency risk so your finance function becomes a competitive weapon rather than a hidden liability.

Table of Contents

- What is agency risk management and why does it matter for SMEs?

- The core pillars: Role clarity, monitoring, and incentives

- Tailored agency risk frameworks for different business sizes

- Building a strong internal control environment

- Advanced agency risk tactics for VC-backed startups

- Practical risk edge cases: South African SME pitfalls

- What most South African SMEs get wrong about agency risk

- Agency risk management made effortless with automation

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Clarify roles and approvals | Spell out who can approve, spend, or pay to reduce confusion and risk. |

| Adopt layered controls | Implement monitoring and incentive systems matched to your business’s size and stage. |

| Strengthen internal and IT controls | Invest in better controls to improve financial accuracy and cut exposure to fraud or tax issues. |

| Use governance for growth | For scaling or VC-backed ventures, staged financing and active oversight are critical safety nets. |

| Resolve SME edge-case risks | Act early on cashflow, data, and resource issues to avoid expensive surprises. |

What is agency risk management and why does it matter for SMEs?

Agency risk management is the practice of reducing the financial and operational damage that occurs when the people running your business do not act fully in your interest. The classic framing is the principal-agent problem: as the owner (principal), you delegate authority to managers, contractors, or accountants (agents), and their incentives do not always match yours. The gap between your goals and their behaviour is where money leaks.

In corporate giants, this shows up in executive pay packages and shareholder dilution. In an SME or startup, it looks more mundane but equally painful. A bookkeeper who rounds figures “for simplicity.” A sales manager who approves their own expense claims. A contractor paid for hours they cannot account for. These are not rare edge cases; they are the default state of under-governed small businesses.

South African SMEs face compounding pressures that make this worse. Load shedding disrupts reconciliation cycles. Staff turnover is high in a volatile labour market. Many founders wear every hat simultaneously and simply do not have the bandwidth to monitor what they have delegated. That combination creates exactly the information asymmetry the principal-agent conflict thrives on.

The core issues agency risk creates in your business include:

- Financial misreporting: Agents control the data you rely on to make decisions. If they manage it to protect themselves, your numbers are unreliable.

- Misaligned incentives: Staff optimise for what they are measured on, not what you actually need. If your bookkeeper is measured on speed, accuracy suffers.

- Approval gaps: Without clear sign-off chains, payments get authorised by the wrong people or not at all.

- Tax exposure: Inaccurate records mean inaccurate VAT returns and income tax submissions, which SARS algorithms are increasingly good at flagging.

Understanding your director responsibilities for SMEs is the first honest step toward acknowledging that agency risk sits squarely in your lap as the principal. You cannot delegate that accountability away.

The core pillars: Role clarity, monitoring, and incentives

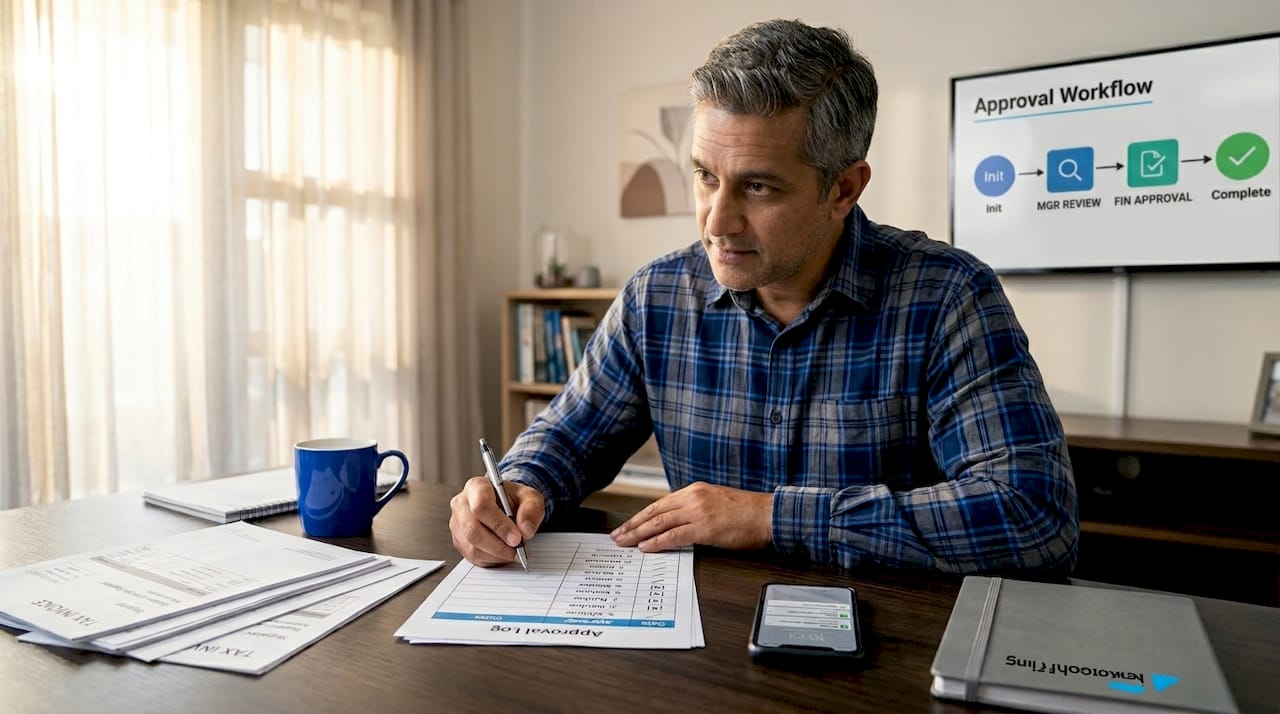

Once you accept that agency risk is your problem to solve, the question becomes: where do you start? Good agency risk implementation covers three non-negotiable pillars: role clarity, monitoring and validation, and incentive alignment. These three controls attack the principal-agent problem at its roots by reducing information asymmetry and aligning behaviour.

1. Role clarity

Define exactly who can approve, spend, commit, or pay. Write it down. This is not bureaucracy; it is the baseline. Without it, every agent operates on their own interpretation of their authority, and interpretations tend to drift toward self-interest over time.

2. Monitoring and validation controls

Reconciliations, review gates, and spot checks are the feedback loops that tell you whether your agents are performing as expected. Monthly bank reconciliations, surprise petty cash counts, and two-person payment approval are not signs of distrust. They are the architecture that makes trust sustainable.

3. Incentive alignment

Tie your KPIs to what you actually need. If your financial manager’s bonus depends partly on the accuracy of monthly reporting rather than just on volume of entries processed, you have suddenly aligned their financial interest with yours.

Here is a practical implementation blueprint for SMEs starting from scratch:

- Map every financial role in your business and document approval limits in writing.

- Implement a dual-authorisation rule for all payments above a defined threshold.

- Run monthly bank reconciliations as a non-negotiable process, not an optional task.

- Set one financial accuracy KPI for every person who touches your books.

- Schedule a quarterly review of all standing payments and recurring contracts.

Pro Tip: The single fastest way to reduce fraud risk and confusion in a small business is to separate the person who initiates a payment from the person who approves it. Even if that means the owner approves everything above R5 000, the discipline this creates is worth the time.

| Area | Without agency risk controls | With structured controls |

|---|---|---|

| Payment approvals | Ad hoc, single sign-off | Documented limits, dual authorisation |

| Reconciliations | Monthly or never | Weekly, with review gates |

| Staff incentives | Activity-based only | Accuracy and compliance KPIs included |

| Tax exposure | High (data errors undetected) | Low (errors caught early) |

| Fraud risk | High (no separation of duties) | Significantly reduced |

Understanding risk management in accounting is the foundation that makes these pillars stick. If you are unsure where to begin on the reporting side, financial reporting for SA SMEs is a useful starting point for building the data integrity your controls depend on.

Tailored agency risk frameworks for different business sizes

Not every business needs the same level of control sophistication. Applying an enterprise governance framework to a five-person startup wastes resources and creates paralysis. The key is right-sizing your controls to your current stage while building toward the next level. Research on South African SMMEs confirms this: a three-stage operational risk model, covering identification, analysis, and treatment, was tested across 208 tourism SMMEs and found to work best when scaled to the firm’s actual capacity rather than imposed at full sophistication from day one.

The risk framework effectiveness varies significantly by organisational maturity. Smaller, younger businesses that try to implement board-level governance before they have stable processes usually end up with beautiful policy documents that nobody follows. Stage-based progression is more durable.

| Business size | Typical capacity | Recommended control sophistication | Key priority |

|---|---|---|---|

| Micro (1-5 staff) | Founder does most tasks | Basic: role clarity, bank recons, payment limits | Separation of duties |

| Small (6-20 staff) | Dedicated bookkeeper/admin | Intermediate: KPIs, monthly reviews, basic audit trail | Incentive alignment |

| Scale-up or VC-backed | Finance team, board | Advanced: board governance, staged financing, IT controls | Information asymmetry reduction |

Minimum controls by stage:

- Micro businesses: Written payment authority, weekly bank balance check, one person reviews all outgoing payments.

- Small businesses: Monthly reconciliation review, dual payment authorisation above threshold, at least one financial accuracy KPI per finance staff member.

- Expanding firms: Quarterly board or management review of financial controls, IT system access controls, formal risk register updated at least twice a year.

Pro Tip: Do not wait until you hit 20 staff to formalise your controls. A founder who implements basic agency risk controls at five employees builds the habits and culture that make scaling far smoother. Start simple, improve every quarter.

Tracking the right financial KPIs for SMEs makes it far easier to spot when an agent’s behaviour is drifting away from your goals, because the numbers will tell you before the relationships do.

Building a strong internal control environment

Controls on paper mean nothing if your systems cannot enforce them. South African audit data shows that internal controls and IT controls vary materially across entities, and weak controls correlate directly with worse financial management outcomes. That is the empirical case for taking your control environment seriously, not just your policies.

“Weak IT and internal controls are not just a compliance risk. They are a tax risk, a fraud risk, and a growth risk. Every gap in your control environment is a window your agents can exploit, knowingly or not.” — Ready Accounting

Your control environment covers two interconnected layers. The first is process controls: who does what, when, and with what oversight. The second is IT controls: who has access to your accounting software, who can create new suppliers, and who can edit past transactions. Both matter equally.

Immediate internal control upgrades most SMEs can adopt without large investment:

- Lock user access in your accounting platform so only authorised users can create supplier accounts or adjust prior-period entries.

- Enable audit trail logging in your cloud accounting software and review it monthly for unexpected changes.

- Implement two-step approval for supplier onboarding to prevent ghost vendor fraud.

- Reconcile your VAT output and input accounts against your bank statements monthly, not just at submission time.

- Conduct a quarterly access review to remove ex-staff system permissions immediately upon exit.

Knowing how to detect financial fraud in your business starts with these IT controls. Combined with strong expense management practices, these upgrades significantly reduce the surface area for agency risk to cause real damage.

Advanced agency risk tactics for VC-backed startups

Venture-backed startups face a specific version of the principal-agent problem. Investors are the principals. Founders are agents. And the founders’ own employees and contractors are agents within that chain. The whole structure is a nested set of competing incentives, and governance mechanics are the primary tool for managing it.

VC risk management typically takes the form of milestone-based capital disbursement and active board oversight. This is not investors being difficult. It is a structurally sound approach to limiting uncontrolled financial exposure when information asymmetry between founders and funders is high.

A practical board-level governance checklist for VC-backed startups:

- Define and agree specific, measurable milestones that trigger each funding tranche.

- Establish a monthly management accounts pack that goes to the board, covering cash runway, burn rate, and key operational metrics.

- Appoint at least one independent board member with financial oversight experience.

- Require board approval for any unbudgeted expenditure above an agreed threshold.

- Implement a conflicts of interest register that is reviewed at every board meeting.

- Schedule a semi-annual review of all controls, not just when something goes wrong.

Startups that implement staged governance early report fewer financial surprises at audit and stronger investor relationships. The discipline of milestone accountability also forces founders to keep their own incentives aligned with the business outcomes rather than personal preferences about how to deploy capital.

Practical risk edge cases: South African SME pitfalls

Even businesses with good intentions and reasonable controls can fall into agency risk edge cases that turn into real tax and operational exposure. In the South African context, the most common triggers are cashflow timing mismatches, data integrity failures, and capacity constraints.

Common edge-case risks South African SME owners face:

- Cashflow timing mismatch: Invoices raised in one period, cash received in another, with VAT calculated on the wrong basis. This creates SARS exposure even when the underlying transaction was legitimate.

- Reconciliation backlogs: When your bookkeeper falls behind, small errors compound. A R500 discrepancy in month one becomes a R6 000 discrepancy by year-end and triggers a query.

- Staff capacity gaps: When one person handles purchasing, payments, and reconciliation, you have a single point of failure for both fraud and error.

- Informal contractor arrangements: Paying freelancers or gig workers without proper contracts creates PAYE and UIF risk if SARS reclassifies them as employees.

- Software access creep: Former staff retaining access to cloud accounting platforms is a common and completely avoidable risk.

Each of these edge cases is preventable. The controls discussed in earlier sections address most of them directly. Avoiding bookkeeping mistakes is often simply a matter of building the habit of timely, accurate record-keeping before the backlog becomes unmanageable.

What most South African SMEs get wrong about agency risk

Here is the uncomfortable truth: most SME owners who do implement agency risk controls treat it as a project they complete once and forget. They run a control workshop, write a policy, and then leave it untouched for three years while the business changes completely around it.

The business environment in South Africa moves fast. Tax regulation evolves. SARS enforcement patterns shift. Staff turn over. Software updates change how access controls work. A static risk framework that was fit for purpose in year one is actively misleading in year three, because it gives you false confidence without giving you real protection.

The right approach is to treat agency risk management as a living operating rhythm, not a document. That means quarterly reviews of your controls, annual policy updates, and a genuine culture where flagging a process gap is rewarded rather than ignored. Businesses that build in regular review cycles adapt faster when something unexpected happens, and something unexpected always happens.

Technology accelerates this significantly. Cloud accounting platforms, automated reconciliations, and real-time approval workflows do not eliminate the need for judgement, but they make it much harder for agency risk to hide. When your numbers are always current, anomalies surface in days rather than months.

If you want to go deeper on building this kind of resilience, deeper risk management strategies offers a more detailed framework for embedding risk thinking into your daily operations.

Agency risk management made effortless with automation

Manual controls are better than no controls, but they have a ceiling. They break under pressure, rely on individual discipline, and scale poorly as your business grows. Automating your reconciliations, payment approvals, and access controls removes the single biggest variable in your agency risk framework: human inconsistency.

Ready Accounting builds custom cloud infrastructure and approval workflows that make agency risk controls the default state of your finance function rather than an extra task on someone’s to-do list. Our automation and cash flow solutions ensure your numbers are always current, your approvals always documented, and your exposure always visible. Explore our accounting automation guide to see what a fully automated control environment looks like in practice, and discover exactly how we help South African SMEs reduce tax liability through cleaner, better-governed financial data.

Frequently asked questions

What is the principal-agent problem in the context of SMEs?

It is the risk that managers or staff act in their own interest rather than the owner’s, often leading to financial misreporting or value leakage. South African SMEs can treat this as a measurable set of controls covering authority, accountability, and incentive alignment.

How can startups with limited resources manage agency risk effectively?

They should start with basic controls such as clear role definitions and simple approval gates, then build out as the business scales. Stage-based frameworks designed for smaller firms work better than complex enterprise models imposed too early.

Why are internal IT controls essential for SME financial health?

Weak IT and internal controls are directly linked to poor financial outcomes; strengthening these systems reduces exposure to errors and fraud significantly. South African audit data confirms this correlation across a range of entities.

How does staged financing reduce risk for venture-backed startups?

By linking capital releases to specific milestones with active board oversight, staged financing limits uncontrolled financial exposure throughout the funding cycle. This is a core VC governance mechanic that protects both investor and founder interests.

What are common agency risk triggers in South African SMEs?

Typical triggers include cashflow timing mismatches, poor data integrity, and limited staff capacity. Each of these common edge cases can amplify financial or tax risk significantly if left unaddressed.