Enterprise Operations tax in South Africa: essential 2026 protocol

Many small business owners in South Africa assume managing tax obligations is complex and overwhelming, but this belief often stems from unclear information rather than actual difficulty. Understanding your tax responsibilities is simpler than you think when you grasp the core concepts. This guide breaks down small business tax essentials for 2026, covering key tax types, who must pay, important exceptions, and practical compliance strategies. Whether you’re navigating provisional tax for the first time or seeking clarity on deductions, you’ll find actionable insights to optimize your tax compliance and support sustainable business growth.

Table of Contents

- Understanding Small Business Tax Obligations In South Africa

- Who Must Pay Provisional Tax And Who Is Exempt?

- Managing Compliance: Practical Steps For Small Business Tax In 2026

- Common Tax Deductions And Saving Strategies For Small Businesses In South Africa

- Simplify Your Small Business Accounting With Ready Accounting

- Frequently Asked Questions About Small Business Tax

Key takeaways

| Point | Details |

|---|---|

| Provisional tax nature | It’s an advance payment on income tax, not a separate tax category |

| Who qualifies | Small businesses with non-remuneration income, companies, and notified taxpayers must comply |

| Important exclusions | PBOs, certain clubs, and individuals below tax thresholds are exempt |

| Compliance benefits | Proper tax management prevents penalties and maintains healthy cash flow |

| Strategic deductions | Legitimate expense claims significantly reduce your taxable income |

Understanding small business tax obligations in South Africa

Small business tax in South Africa encompasses multiple tax types that business owners must navigate to remain compliant and financially healthy. At its core, small business taxation includes income tax obligations, VAT considerations, payroll taxes, and the often misunderstood provisional tax system. Many business owners confuse these categories or assume provisional tax represents an additional tax burden when it’s simply a payment mechanism.

Provisional tax is a mechanism for paying income tax during the tax year, acting as an advance payment. Instead of paying your entire annual income tax liability in one lump sum after year end, provisional tax spreads this obligation across two payments during the year. This system helps SARS collect revenue consistently while allowing businesses to manage cash flow more predictably.

Understanding different types of business taxes is essential for proper financial planning. Here are the core tax obligations small businesses face:

- Income tax on business profits, calculated annually based on taxable income

- Provisional tax payments made twice yearly as advance income tax installments

- Value Added Tax (VAT) for businesses exceeding the registration threshold

- Pay As You Earn (PAYE) withholding tax on employee salaries

- Skills Development Levy and Unemployment Insurance Fund contributions

- Capital Gains Tax on asset disposals above exemption thresholds

Consider this practical example of how provisional tax works. Your business expects to earn R500,000 taxable income in 2026. Rather than paying the full tax liability in 2027 when you file your annual return, you make two provisional payments during 2026. The first payment in August 2026 covers an estimate of your first six months’ income. The second payment in February 2027 adjusts based on your full year projection. This approach smooths your cash flow and keeps you current with SARS.

The SARS provisional tax guide provides detailed technical specifications, but the fundamental concept remains straightforward. You’re prepaying tax you’ll owe anyway, not creating an additional obligation. This distinction matters because many small business owners initially view provisional tax as an extra burden rather than a practical payment schedule that actually benefits their financial planning.

Who must pay provisional tax and who is exempt?

Determining whether your small business falls under provisional taxpayer requirements is critical for 2026 compliance. SARS defines specific criteria that trigger provisional tax obligations, and understanding these parameters helps you plan appropriately and avoid unexpected penalties.

A provisional taxpayer includes individuals earning non-remuneration income, companies, and those notified by the SARS Commissioner. Non-remuneration income encompasses business profits, rental income, investment returns, and other earnings not subject to PAYE withholding. If you receive a salary from an employer who deducts PAYE, that portion doesn’t trigger provisional tax obligations, but your side business income likely does.

Here are the key criteria defining provisional taxpayer status:

- Natural persons deriving income from sources other than remuneration exceeding the tax threshold

- All companies and close corporations regardless of income level

- Trusts earning income subject to normal tax rates

- Individuals specifically notified by SARS to register as provisional taxpayers

- Anyone whose taxable income exceeds their remuneration by a material amount

Equally important are the exclusions that exempt certain entities from provisional tax requirements. Certain entities are excluded from provisional tax payments, such as Public Benefit Organisations (PBOs) and recreational clubs approved by SARS. These exemptions recognize that some organizations operate under special tax treatment or have minimal tax liability.

Specific exclusions from provisional tax include:

- Public Benefit Organisations with approved PBO status

- Recreational clubs meeting SARS approval criteria

- Body corporates established under sectional title legislation

- Natural persons whose only income source is remuneration subject to PAYE

- Individuals whose taxable income falls below the annual tax threshold

- Persons aged 65 or older with income below the higher age-related threshold

Your provisional tax returns guide status may change as your business grows or your income sources shift. A freelancer earning R200,000 annually becomes a provisional taxpayer once income exceeds the threshold, even if they previously only had PAYE employment. Similarly, starting a rental property portfolio while employed triggers provisional tax obligations for the rental income portion.

Pro Tip: Verify your provisional taxpayer status early in the tax year by reviewing your income sources and comparing them against current thresholds. Registering proactively prevents penalties and gives you time to plan cash flow for the payment deadlines. If you’re uncertain about your status, consult the SARS provisional tax taxpayer criteria or seek professional guidance before the first payment deadline.

Managing compliance: practical steps for small business tax in 2026

Effective tax compliance requires systematic record keeping, timely filing, and strategic planning throughout the year. Small businesses that treat tax management as an ongoing process rather than a year end scramble consistently achieve better outcomes and avoid costly penalties.

Maintaining comprehensive financial records forms the foundation of tax compliance. SARS expects you to retain supporting documentation for all income and expenses, including invoices, receipts, bank statements, and contracts. Your SARS record keeping rules obligations extend five years from the date of submission for your latest tax return, meaning 2026 records must remain accessible until at least 2032.

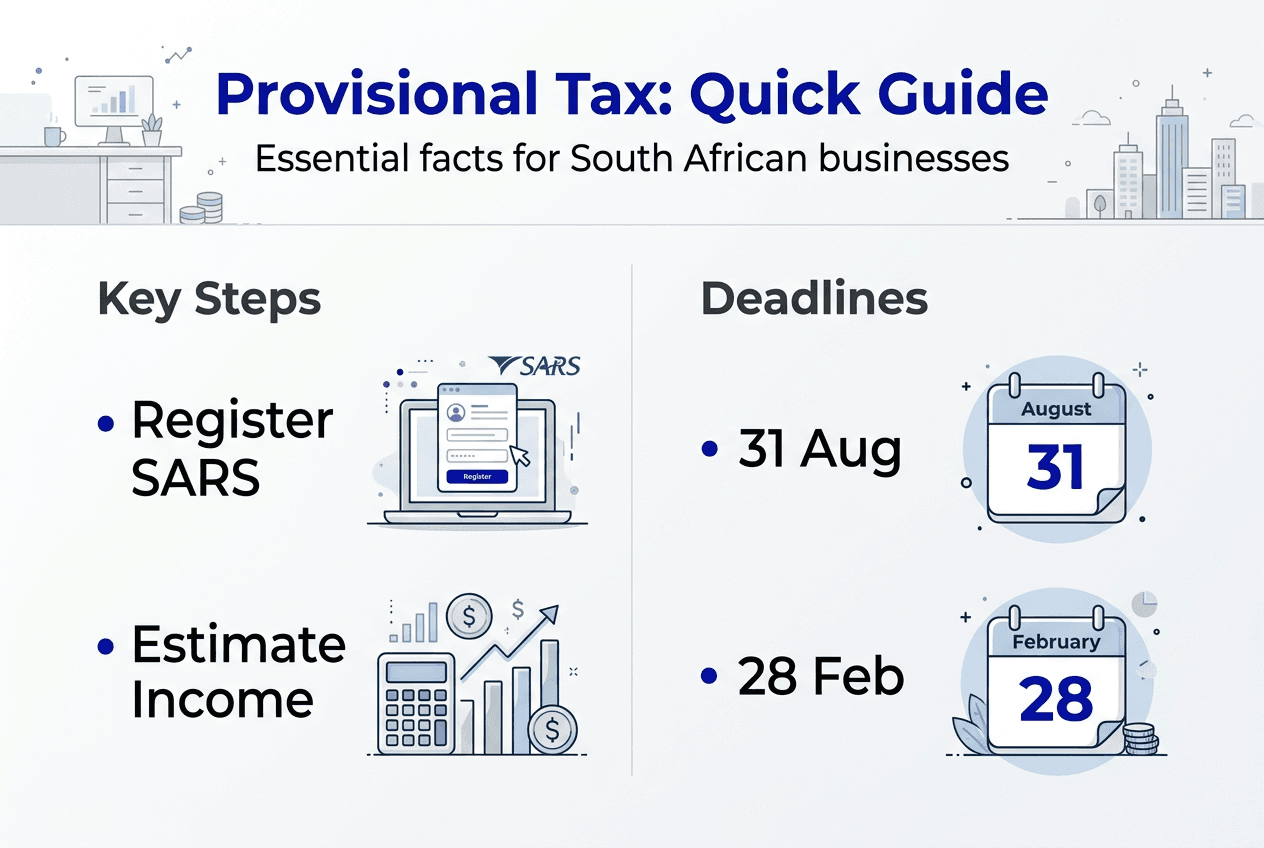

Provisional tax filing deadlines for 2026 require careful attention to avoid penalties:

| Payment Period | Filing Deadline | Payment Due Date | Coverage |

|---|---|---|---|

| First Provisional | 31 August 2026 | 31 August 2026 | Estimated income for first 6 months |

| Second Provisional | 28 February 2027 | 28 February 2027 | Full year income estimate and adjustment |

| Third Voluntary | 30 September 2027 | 30 September 2027 | Final adjustment after annual return |

Provisional tax is a critical aspect of tax compliance for small businesses in South Africa, ensuring that income tax liabilities are met throughout the year. Missing these deadlines triggers penalties calculated as a percentage of the unpaid amount, plus interest charges that compound over time. The financial impact extends beyond the penalties themselves because late payments disrupt cash flow planning and may signal compliance issues to SARS.

Practical tax compliance strategies for small businesses include:

- Implement cloud accounting software that tracks income and expenses in real time

- Schedule monthly financial reviews to monitor profitability and estimate tax liability

- Set aside provisional tax funds in a separate account to ensure payment availability

- Reconcile bank statements monthly to catch errors before they compound

- Maintain digital copies of all tax-related documents with secure backup systems

- Review your year-end tax planning guide quarterly to optimize deductions

- Submit returns early to allow buffer time if technical issues arise

- Monitor SARS communications for changes to rates, thresholds, or requirements

Managing provisional tax payments effectively prevents cash flow crises that plague many small businesses. Calculate your expected annual tax liability at the start of the year, then divide by two for each provisional payment. Build a buffer of 10 to 15 percent above your estimate to account for business growth or unexpected income. This conservative approach means you’ll likely receive a refund after filing your annual return rather than facing an unexpected payment.

Pro Tip: Leverage digital tools and cloud accounting platforms to automate tax calculations and deadline reminders. Modern accounting software integrates with your bank accounts, categorizes transactions automatically, and generates provisional tax estimates based on actual financial performance. This automation reduces manual errors and frees your time for strategic business activities rather than administrative tasks. Consider partnering with accounting professionals who specialize in small business tax to ensure you’re maximizing deductions while maintaining full SARS provisional tax compliance.

Common tax deductions and saving strategies for small businesses in South Africa

Strategic tax planning extends beyond compliance to actively reducing your tax liability through legitimate deductions and smart financial decisions. Small businesses that understand available deductions and structure expenses appropriately can significantly lower their effective tax rate while remaining fully compliant.

Deductible business expenses reduce your taxable income directly, meaning every rand you legitimately claim saves you approximately 28 cents in corporate tax or your marginal rate for sole proprietors. The key is ensuring expenses meet SARS criteria: they must be incurred in the production of income, not be capital in nature, and have proper supporting documentation.

| Deduction Category | Common Examples | Tax Impact | Documentation Required |

|---|---|---|---|

| Operating Expenses | Rent, utilities, supplies | Direct reduction of taxable income | Invoices, receipts, lease agreements |

| Vehicle Expenses | Fuel, maintenance, insurance | Proportional to business use | Logbook, receipts, business km records |

| Professional Fees | Accounting, legal, consulting | Fully deductible when business-related | Invoices, proof of payment |

| Marketing Costs | Advertising, website, promotions | Immediate deduction | Contracts, invoices, campaign records |

| Equipment Depreciation | Computers, machinery, furniture | Spread over asset lifespan | Purchase invoices, asset register |

Your small business tax deductions checklist should include often overlooked items that add up substantially. Home office expenses become deductible when you use a dedicated space exclusively for business, calculated as a percentage of total home costs. Professional development including courses, books, and industry memberships qualify when they enhance your business skills. Even bank charges, insurance premiums, and bad debts written off represent legitimate deductions many small businesses miss.

Tax saving strategies extend beyond claiming deductions to timing and structuring decisions:

- Accelerate deductible expenses into the current tax year when you expect higher income

- Defer income to the following year if you anticipate lower tax rates or reduced earnings

- Maximize retirement annuity contributions which provide immediate tax deductions

- Structure asset purchases to optimize depreciation allowances and section 12E benefits

- Separate personal and business expenses completely to simplify deduction claims

- Review expense categories quarterly to identify potential deduction opportunities

- Consider timing of major purchases around year end for optimal tax treatment

The difference between tax avoidance and tax evasion is critical. Legitimate tax planning arranges your affairs to minimize tax within the law, while evasion involves illegal concealment or misrepresentation. Claiming personal expenses as business costs, inflating deductions, or omitting income crosses into evasion territory with serious consequences including penalties, interest, and potential criminal charges.

Implementing smart tax saving strategies requires understanding the interplay between different tax provisions. Section 12E allowances for manufacturing assets, research and development incentives, and small business corporation tax rates all offer opportunities for businesses meeting specific criteria. The small business corporation regime provides preferential rates for companies with gross income below R20 million and meeting other requirements, potentially saving tens of thousands in tax annually.

Pro Tip: Schedule an annual tax planning session with a qualified tax professional who specializes in small business taxation. They can identify deductions specific to your industry, advise on optimal business structure, and develop multi-year strategies that compound savings over time. The cost of professional advice typically pays for itself many times over through legitimate tax savings you wouldn’t have identified independently. A fresh expert perspective often reveals deduction opportunities hiding in plain sight within your existing operations.

Simplify your small business accounting with Ready Accounting

Navigating small business tax obligations becomes significantly easier when you have expert support and modern tools working for you. Ready Accounting specializes in helping South African small businesses manage tax compliance efficiently while optimizing financial performance through strategic planning.

Our cloud accounting benefits for small business approach delivers real-time visibility into your financial position, making provisional tax estimates accurate and stress-free. You’ll always know where your business stands financially, enabling confident decision-making and eliminating surprises at tax time. Our team handles the technical complexity while you focus on growing your business.

Explore our comprehensive cloud-based accounting guide to understand how modern financial management transforms tax compliance from a burden into a strategic advantage. We combine cutting-edge technology with personalized service, ensuring your specific business needs receive the attention they deserve. From provisional tax calculations to maximizing deductions using our tax deductions checklist, we’re your partner in financial success.

Frequently asked questions about small business tax

Why does provisional tax matter for small businesses?

Provisional tax helps small businesses spread their annual income tax liability across manageable payments during the year rather than facing a large bill after year end. This payment structure improves cash flow predictability and ensures you remain current with SARS obligations, avoiding penalties and interest charges that damage profitability.

What is the difference between provisional tax and annual income tax?

Provisional tax represents advance payments toward your annual income tax liability, not a separate tax type. You estimate your yearly taxable income and pay it in two installments during the tax year. When you file your annual return, SARS calculates your actual tax liability and either refunds overpayments or collects any shortfall.

How do I know if my small business must register for VAT?

You must register for VAT when your taxable supplies exceed R1 million in any consecutive 12-month period, or you reasonably expect to exceed this threshold. Voluntary registration is available for businesses below the threshold who want to claim input VAT on expenses. Registration creates obligations to charge VAT, file returns, and maintain specific records.

What are the key tax deadlines small business owners should remember for 2026?

The critical deadlines include 31 August 2026 for first provisional tax, 28 February 2027 for second provisional tax, and your annual return deadline based on your year end date. VAT vendors must file returns monthly or bi-monthly depending on turnover. Missing these dates triggers automatic penalties, so setting calendar reminders well in advance protects your business.

What record-keeping practices support effective tax compliance?

Maintain comprehensive records of all income and expenses with supporting documentation like invoices, receipts, and bank statements. Organize records systematically using accounting software or clearly labeled files, and retain everything for at least five years. Regular reconciliation of accounts catches errors early, while separating business and personal finances simplifies deduction claims and audit defense. Review our top tax questions for small business for additional guidance on common compliance concerns.

Recommended

- Top Tax Questions Small Business Owners Ask in 2025 – Ready Accounting

- Year-End Tax Planning Guide for Small Businesses – Ready Accounting

- Dividends tax in South Africa: essential guide for SMEs 2026 – Ready Accounting

- How to save tax in South Africa: smart strategies for SMEs in 2026 – Ready Accounting

- The Essential South African SEO Strategy for Business Growth – LSA SEO Agency