Prepare annual financial statements for your company

Executive Summary

- Most South African SME owners underestimate the detailed preparation needed for compliant annual financial statements. Properly compiling AFS provides an honest business snapshot and ensures adherence to CIPC and SARS requirements. Staying organized throughout the year and consulting registered professionals simplifies the year-end process significantly.

Every South African business owner eventually hits the same wall: year-end arrives, and the question of how to prepare annual financial statements for my company becomes urgent, stressful, and confusing all at once. The Companies Act 71 of 2008 makes AFS compliance non-negotiable for registered companies, yet most SME owners underestimate how much preparation, sequencing, and verification goes into getting it right. Done properly, your Annual Financial Statements (AFS) do more than satisfy SARS and CIPC. They give you a clear, honest picture of where your business actually stands.

Table of Contents

- Key takeaways

- Prerequisites for preparing annual financial statements

- Step-by-step guide to preparing your core statements

- Reconciliation and review before you finalise

- Filing requirements and submitting to CIPC

- My honest take on AFS preparation for South African SMEs

- How Readyaccounting helps you get this right

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Know your Public Interest Score | Your PIS determines whether you need an audit, independent review, or simpler compilation. |

| Gather documents before you start | A complete trial balance, asset register, and bank reconciliations prevent errors downstream. |

| Follow the correct preparation sequence | Build your income statement first, then balance sheet, then cash flow statement. |

| Reconcile everything before filing | Cross-checking figures across all three statements catches errors before CIPC or SARS does. |

| File within 30 business days | CIPC annual returns are due within 30 business days of your company anniversary date. |

Prerequisites for preparing annual financial statements

Before you write a single number, you need to gather the right materials. Skipping this step is the reason most SME owners hit errors mid-preparation, then waste days backtracking.

Documents you need on hand

The foundation of any solid AFS is your trial balance, which summarises all ledger accounts at year-end. Beyond that, you need:

- Signed bank reconciliations for every business account

- A fixed asset register showing cost, accumulated depreciation, and carrying values

- Debtors and creditors age analysis reports

- VAT reconciliation matching your SARS VAT201 submissions

- Payroll summaries for the full financial year

- Loan agreements and any outstanding liability schedules

Your asset register feeds depreciation notes directly into the AFS, so gaps in that register create cascading problems across multiple statements.

The Public Interest Score explained

One concept that catches SME owners off guard is the Public Interest Score (PIS). Many assume preparing financial statements is simply a numbers exercise. In reality, PIS dramatically shapes your audit obligations. Your PIS is calculated using factors like turnover, number of employees, third-party liabilities, and whether you have shareholders who are not directors.

| PIS range | Requirement |

|---|---|

| Below 100 | Compilation acceptable (no mandatory audit or review) |

| 100 to 349 | Independent review required (or audit, depending on compilation method) |

| 350 and above | Full audit required, including XBRL filing |

Platforms like IntelliAudit can help you understand exactly what level of assurance your PIS demands before you engage an auditor or reviewer.

Financial year-end and CIPC deadlines

Your chosen year-end date is not arbitrary. Changing your financial year-end requires formal CIPC approval, and any period covered must not exceed 15 months. If you change year-end without updating CIPC, your filings get rejected and penalties follow. Align your year-end strategically with your business cycle, and document the reason for any change in the notes to your AFS.

Pro Tip: Set a calendar reminder 60 days before your financial year-end. That gives you time to run preliminary reconciliations and identify any missing records before the crunch begins.

Step-by-step guide to preparing your core statements

This is where the actual annual financial report preparation work happens. The sequence matters. Preparing statements out of order creates inconsistencies that are hard to trace later.

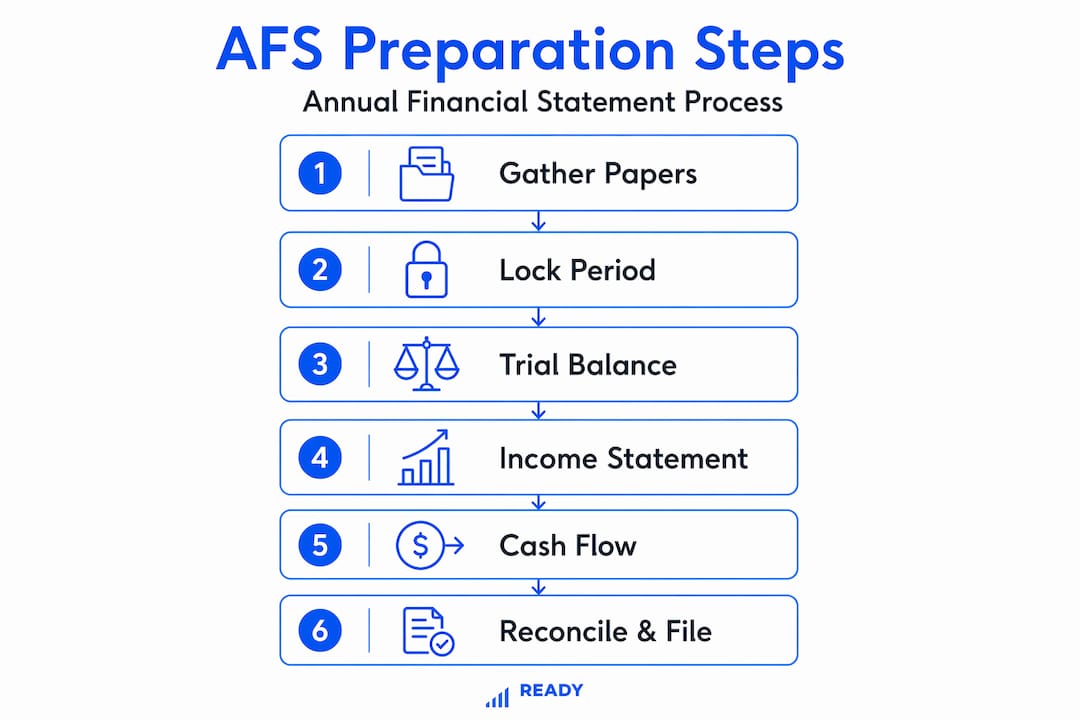

Step 1: Lock in your reporting period and trial balance

Clarity on your reporting period affects every decision downstream. Confirm your financial year start and end dates, then extract a final, adjusted trial balance from your accounting system. Every entry should be posted and all suspense accounts cleared before you proceed.

Step 2: Prepare the income statement

The income statement records your company’s financial performance over the period. Work through it in this order:

- Start with gross revenue and deduct returns or discounts to get net revenue.

- Subtract cost of sales to calculate gross profit.

- Deduct operating expenses (salaries, rent, depreciation, marketing) to reach operating profit.

- Add non-operating income (interest received) and subtract interest paid.

- Apply your income tax charge to arrive at net profit after tax.

Your income statement for South African SMEs should reflect SARS-aligned tax calculations, especially where provisional tax payments have been made during the year.

Step 3: Prepare the balance sheet

The balance sheet is a snapshot of what your company owns and owes on the last day of the financial year. Organise it as follows:

- Assets: List current assets (cash, debtors, inventory) first, then non-current assets (property, equipment, investments).

- Liabilities: Current liabilities (creditors, short-term loans, VAT payable) followed by long-term liabilities (bonds, deferred tax).

- Equity: Share capital plus retained earnings, adjusted for the current year’s profit or loss.

The golden rule is that assets must equal liabilities plus equity. If they do not, something is wrong in your ledger.

Step 4: Prepare the cash flow statement

The cash flow statement explains the movement of actual cash, which is different from profit. You have two methods available:

| Method | How it works | Best for |

|---|---|---|

| Direct method | Lists actual cash receipts and payments | Businesses with simple transaction volumes |

| Indirect method | Starts with net profit, adjusts for non-cash items | Most SMEs using accrual accounting |

Most South African SMEs use the indirect method because it works directly from the income statement and balance sheet figures you have already prepared.

Pro Tip: The most common cash flow error is double-counting. If you paid off a loan during the year, the repayment appears in financing activities. Do not also include it in operating expenses.

Reconciliation and review before you finalise

Getting numbers on a page is not the finish line. This is where many SMEs make costly mistakes by treating preparation and filing as the same step. They are not.

A well-maintained reconciliation trail is the single biggest efficiency gain in the entire process. When your bank reconciliations, creditor schedules, and debtor age analyses are clean and current, your auditor or reviewer can verify data without recreating records from scratch. This saves you money and time.

Before you sign off on any set of statements, work through this verification checklist:

- Confirm that net profit on the income statement matches the movement in retained earnings on the balance sheet.

- Check that closing cash on the cash flow statement matches the cash balance on the balance sheet.

- Verify all loan balances against signed agreements and bank statements.

- Confirm that VAT balances on the balance sheet reconcile to your outstanding VAT201 returns.

- Review asset values against the fixed asset register, and confirm depreciation rates are consistent with prior years.

Cross-checking consistency across all three statements is not optional. SARS and CIPC both have systems that flag inconsistencies, and the last thing you want is a query letter after submission.

Pro Tip: Ask someone outside your finance team to read through the notes to your AFS. If they cannot understand what a number refers to, your notes need more detail.

Filing requirements and submitting to CIPC

Once your statements are finalised and signed, you need to file. CIPC annual returns are due within 30 business days after your company’s anniversary date, and the system is rolling. Missing this window attracts penalties and, in serious cases, deregistration.

What you upload depends on your PIS:

- PIS below 350 (no audit required): You may submit a Financial Accountability Supplement (FAS) instead of full audited statements, which reduces compliance burden for smaller companies.

- PIS 350 and above: Full audited AFS must be uploaded, along with XBRL-tagged data.

- All companies: The annual return fee is calculated on your authorised share capital. Confirm this amount before filing to avoid underpayment.

Practical tips for a smooth CIPC submission:

- Keep PDF copies of your signed AFS on file before uploading. The CIPC portal sometimes loses documents during submission.

- Screenshot your proof of payment and confirmation receipt. These are your audit trail if any queries arise.

- Confirm that your company’s registered address and director details are current on the CIPC database before submitting. Outdated details cause rejections.

- If your financial year-end has changed, confirm the updated date reflects correctly on the CIPC system before filing.

My honest take on AFS preparation for South African SMEs

I have worked with enough South African business owners to know that the biggest AFS problems are not technical. They are timing and mindset.

The companies that breeze through year-end are not the ones with the most sophisticated software. They are the ones that keep their records clean throughout the year. Bank reconciliations done monthly. Invoices captured weekly. Asset registers updated when equipment is purchased. When those habits are in place, preparing a full set of annual financial statements takes days, not weeks.

What I have also learned is that most SME owners wait too long to ask for help. They assume that engaging a SAICA or SAIPA-registered accountant is an expense they can delay. Then they hit their anniversary date, realise their records are a mess, and pay three times more to fix it under pressure.

My genuine recommendation: align your financial reporting process with your business rhythm from the start of the financial year. Treat your AFS preparation as a 12-month project, not a 2-week scramble. And if your PIS is trending toward the audit threshold, build that relationship with a registered auditor before you legally need one.

Automation helps too. Cloud accounting tools that reconcile bank feeds daily remove the single biggest source of year-end chaos. The goal is to arrive at year-end with nothing to find.

— Johan

How Readyaccounting helps you get this right

Readyaccounting works with South African SMEs and VC-backed startups that are tired of year-end financial chaos. We replace manual bookkeeping with cloud-based infrastructure that keeps your records audit-ready throughout the year, not just when a deadline is approaching.

Our team handles the full cycle: from trial balance through to signed AFS, CIPC filing, and SARS compliance. If your PIS requires an independent review or audit, we coordinate that process too, so nothing falls through the gaps.

We have also built practical resources to support your financial strategy beyond compliance. Read how automating your accounting improves your cash position, or explore our guide on setting financial goals that your AFS can actually support. When your financial statements are accurate and current, they stop being a compliance exercise and start being a decision-making tool.

Contact Readyaccounting to find out how we can take the complexity out of your annual financial report preparation.

FAQ

What documents do I need to prepare annual financial statements?

You need a finalised trial balance, bank reconciliations, a fixed asset register, VAT reconciliations, and debtor and creditor schedules. Missing any of these causes delays and errors during preparation.

How does my Public Interest Score affect my AFS requirements?

Your PIS determines whether you need a full audit, an independent review, or a simpler compilation. Companies scoring 350 or above require a full audit and XBRL filing with CIPC.

When is the CIPC annual return deadline?

CIPC annual returns are due within 30 business days after your company’s anniversary date. Late submissions attract penalties and risk deregistration.

What is a Financial Accountability Supplement?

A Financial Accountability Supplement (FAS) is a simplified document that lower-PIS companies can submit to CIPC instead of full audited financial statements, reducing the compliance burden for smaller businesses.

Can I prepare my own annual financial statements?

Yes, but accuracy depends entirely on the quality of your underlying records. Most SMEs benefit from working with a registered accountant, particularly for the reconciliation, notes, and SARS-aligned tax calculations that regulators scrutinise most closely.