Optimize investment property ownership in South Africa

Many South African business owners hold investment properties personally, believing it’s the simplest approach. This common misconception exposes them to higher tax rates and liability risks they could easily avoid. A strategic ownership structure using a trust that owns a company, which then holds the property, delivers superior asset protection and tax efficiency. This article explains how this layered model works, why it benefits small to medium-sized enterprises, and the practical steps to implement it correctly in 2026.

Table of Contents

- Understanding The Trust And Company Structure For Property Ownership

- Tax Advantages Of Using A Trust And Company To Own Investment Property

- Legal And Compliance Considerations For Trust-Company Property Ownership

- Practical Steps To Set Up And Manage The Trust-Company Property Structure Effectively

- How Ready Accounting Supports You In Optimizing Your Investment Property Ownership

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Enhanced asset protection | A trust owning a company that holds property separates personal liability from business assets |

| Tax efficiency opportunities | This structure enables income splitting and strategic distribution planning to reduce overall tax burden |

| Compliance requirements | Proper legal documentation and separate accounting records are essential to maintain benefits |

| Dividends tax considerations | Understanding the 20% dividends tax on distributions helps optimize cash flow planning |

| Professional guidance needed | Expert accounting and legal support ensures correct setup and ongoing compliance |

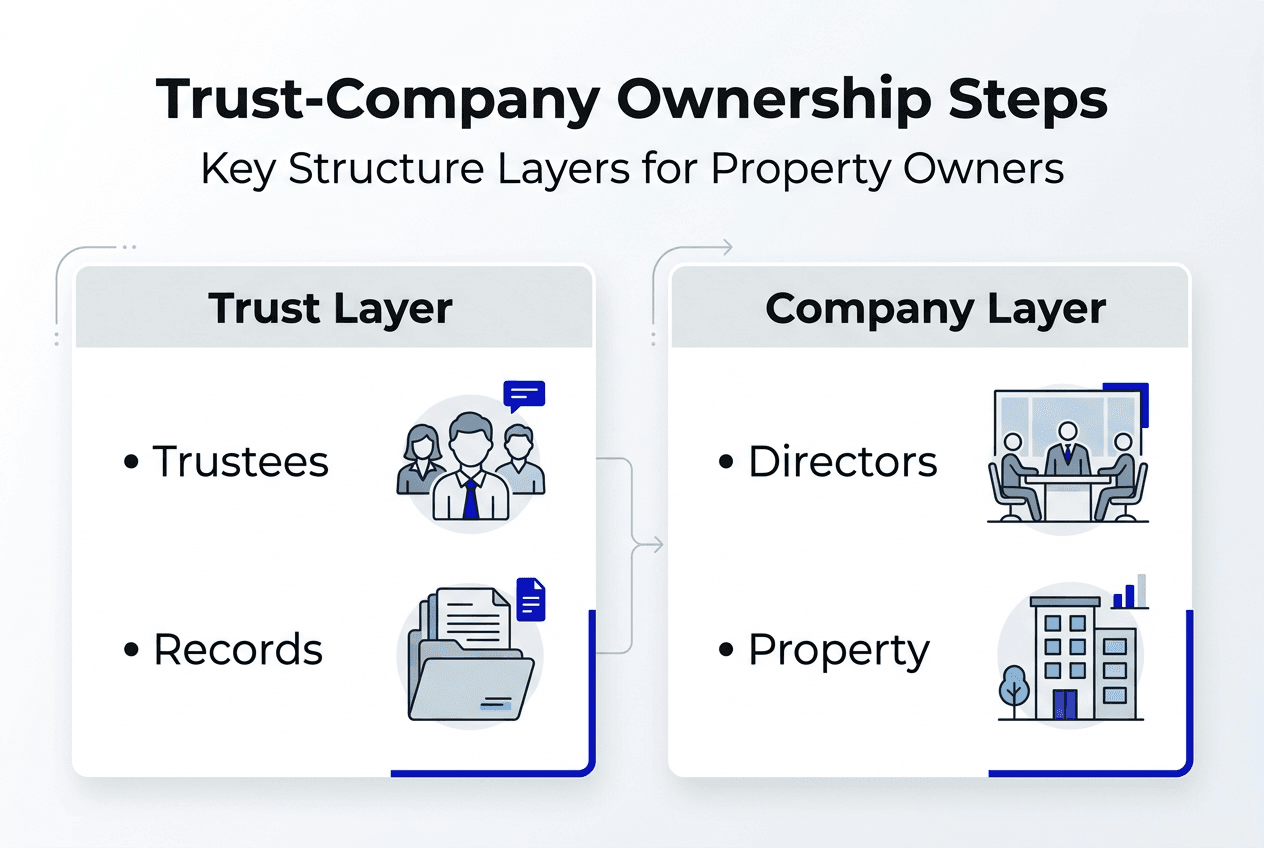

Understanding the trust and company structure for property ownership

The ownership model we’re discussing involves three distinct legal layers. A trust holds shares in a private company, and that company owns the physical investment property. Each entity serves a specific purpose and operates under different legal frameworks in South Africa.

A trust is a legal arrangement where trustees hold and manage assets for beneficiaries. The company is a separate legal entity that can own property, enter contracts, and generate income independently from its shareholders. A trust owning a company that holds property provides separation of liability and can protect assets from creditors.

This structure delivers several concrete advantages:

- Limited liability protection shields personal assets from property-related claims

- Clear governance through formal trustee and director roles

- Flexibility in distributing income among multiple beneficiaries

- Estate planning benefits that simplify wealth transfer

- Professional credibility when dealing with tenants and lenders

Trustees control the trust and vote the company shares. Directors manage the company’s daily operations and property decisions. Beneficiaries receive distributions according to the trust deed. These roles can overlap, but maintaining proper documentation separating each function is crucial.

The legal separation between entities creates a protective barrier. If the property faces a lawsuit, only the company’s assets are at risk. Your personal wealth and the trust’s other holdings remain protected. This separation only works if you maintain distinct accounting records, separate bank accounts, and formal decision-making processes for each entity. Mixing personal and business transactions destroys this protection.

Understanding record keeping requirements becomes essential when managing multiple entities. Each layer requires its own financial statements, tax returns, and compliance documentation.

Tax advantages of using a trust and company to own investment property

Tax efficiency represents the most compelling financial reason to adopt this structure. Personal income tax in South Africa reaches 45% at the highest marginal rate. Companies pay a flat 27% on taxable income. Trusts can distribute income to beneficiaries in lower tax brackets, potentially reducing the overall family tax burden significantly.

Consider how rental income flows through each structure:

| Ownership type | Tax rate | Additional considerations |

|---|---|---|

| Personal ownership | Up to 45% marginal rate | No flexibility in income allocation |

| Company ownership | 27% flat rate | Dividends tax applies on distributions |

| Trust distributions | Beneficiary’s marginal rate | Allows strategic income splitting |

The company collects rental income and deducts allowable expenses like maintenance, rates, and interest. It pays 27% corporate tax on the profit. When distributing profits to the trust as dividends, dividends tax at 20% applies on company distributions, but proper planning within a trust can minimize overall tax burden.

The trust then allocates income among beneficiaries. If you have family members in lower tax brackets, distributing to them reduces the combined tax bill. A beneficiary earning R100,000 annually pays far less tax than someone in the 45% bracket. This income splitting creates substantial savings over time.

Capital gains tax adds another dimension. When selling property, companies pay CGT at an effective rate of 21.6% (80% of 27%). Individuals face rates up to 18% (40% inclusion rate times 45% marginal rate). The company structure may result in slightly higher CGT, but the ongoing income tax savings typically outweigh this difference over a property’s holding period.

Using a trust that owns a company can reduce exposure to high personal income tax rates on rental income by distributing profits efficiently. Strategic timing of distributions, careful expense tracking, and proper loss utilization all contribute to tax optimization.

Key tax planning strategies include:

- Retaining profits in the company during high-income years

- Distributing to beneficiaries when they have lower income

- Maximizing deductible expenses through proper documentation

- Timing property sales to align with favorable tax positions

- Using debt strategically to create interest deductions

Pro Tip: Keep accurate financial records to maximize allowable deductions and reduce tax risk. SARS scrutinizes trust and company structures carefully, so immaculate documentation protects you during audits.

The interaction between corporate tax, dividends tax, and personal income tax creates planning opportunities. Working with experienced tax professionals helps you navigate these layers and identify savings specific to your situation. Year-end tax planning becomes particularly important when managing multiple entities.

Legal and compliance considerations for trust-company property ownership

Operating this structure correctly requires understanding your legal obligations as both trustee and director. The Trust Property Control Act governs trustees’ duties, while the Companies Act regulates directors’ responsibilities. These laws impose fiduciary duties, meaning you must act in the best interests of beneficiaries and shareholders.

Trustees must maintain proper trust records, hold regular meetings, and document all decisions in writing. Directors face similar requirements for company governance. You cannot simply make informal decisions. Every significant action needs formal minutes, resolutions, and supporting documentation.

Proper compliance with SARS and Companies Act rules is critical to preserve asset protection and tax benefits. Failure to maintain corporate formalities can result in piercing the corporate veil, where courts ignore the separate legal entities and hold you personally liable.

Essential documentation includes:

- Trust deed and amendments filed with the Master of the High Court

- Company registration documents and share certificates

- Property title deeds registered in the company’s name

- Separate bank accounts for trust, company, and personal use

- Annual financial statements for both trust and company

- Tax returns filed on time for each entity

- Meeting minutes documenting all major decisions

Common compliance pitfalls destroy the structure’s benefits. Mixing funds between entities, failing to hold formal meetings, or neglecting annual returns can trigger penalties and eliminate asset protection. SARS may recharacterize transactions if you cannot demonstrate legitimate business purposes.

Recordkeeping and governance of trusts and companies require specialised processes to avoid legal and tax risks. You must maintain accounting records for at least five years. Property-related documents like lease agreements, maintenance records, and insurance policies need systematic organization.

The Companies and Intellectual Property Commission requires annual returns from all companies. Missing this deadline results in deregistration, which creates massive complications for property ownership. Trusts must file annual income tax returns even if no tax is payable. These administrative tasks demand consistent attention throughout the year.

Another critical consideration involves transfer duties and related costs. When moving an existing property into this structure, you may trigger transfer duty, capital gains tax, and conveyancing fees. Planning the initial setup carefully minimizes these transition costs.

Pro Tip: Engage professionals experienced in trust and company law to help navigate complex compliance requirements. The cost of expert guidance is far less than the penalties and lost benefits from incorrect implementation.

Tax compliance strategies must align with your legal obligations. Regular reviews with your accountant and attorney ensure you remain compliant as laws change and your circumstances evolve.

Practical steps to set up and manage the trust-company property structure effectively

Implementing this ownership model involves several sequential steps. Rushing through setup creates problems that take years to fix. Follow this process methodically:

- Consult with a qualified attorney to draft a trust deed tailored to your goals and family situation

- Register the trust with the Master of the High Court and obtain a trust registration number

- Apply for a tax reference number for the trust from SARS

- Establish a company through CIPC with the trust as the sole or majority shareholder

- Open separate bank accounts for both the trust and company

- Transfer existing property or acquire new property in the company’s name

- Implement proper accounting systems and recordkeeping procedures

- Schedule regular trustee and director meetings to maintain compliance

Stepwise guidance simplifies the process to establish a trust owning a company that holds investment property. Each step requires specific documentation and professional input.

Setup costs and timelines vary based on complexity:

| Component | Estimated cost | Timeline |

|---|---|---|

| Trust establishment | R8,000 to R15,000 | 4 to 6 weeks |

| Company registration | R2,000 to R5,000 | 1 to 2 weeks |

| Property transfer | 1% to 3% of property value | 8 to 12 weeks |

| Initial accounting setup | R5,000 to R10,000 | 2 to 4 weeks |

Ongoing administration requires consistent effort. Monthly bookkeeping, quarterly management accounts, and annual financial statements keep you compliant and informed. Budget for annual costs including accounting fees, audit fees if required, company annual returns, and professional advisory services.

Best practices for effective management include:

- Maintaining completely separate finances for each entity

- Documenting every transaction with proper invoices and receipts

- Holding formal meetings at least quarterly with written minutes

- Reviewing financial statements monthly to track performance

- Planning tax obligations proactively rather than reactively

- Updating trust deeds and company documents as laws change

Working with accountants and legal advisors specialized in this field proves invaluable. They help you avoid costly mistakes, identify tax-saving opportunities, and ensure ongoing compliance. The right professionals pay for themselves through the value they deliver.

Smart tax strategies require proactive planning throughout the year, not just at tax season. Regular check-ins with your advisory team keep your structure optimized as your property portfolio grows.

Modern business record keeping tools streamline administration significantly. Cloud-based systems provide real-time visibility into your finances and simplify collaboration with your accounting team.

How Ready Accounting supports you in optimizing your investment property ownership

Navigating the complexities of trust and company structures requires specialized expertise. Ready Accounting brings deep experience helping South African SMB owners implement and manage these ownership models effectively. Our team understands the unique tax planning opportunities and compliance requirements specific to property investment structures.

We offer comprehensive services including trust and company accounting, tax return preparation, and strategic advisory support. Our cloud accounting solutions simplify managing multiple entities by centralizing financial data and automating routine tasks. You gain real-time visibility into your property performance while we handle the technical compliance details.

Our cloud accounting expertise enables seamless collaboration regardless of location. Whether you need help with initial setup, ongoing bookkeeping, or year-end tax planning, we provide personalized support tailored to your specific situation. Discover what cloud accounting offers South African business owners seeking to optimize their investment property structures.

Frequently asked questions

What benefits does a trust-company structure offer over personal ownership?

This structure provides superior asset protection by separating personal liability from property risks. It enables tax-efficient income distribution among family members in lower tax brackets. The company pays a flat 27% tax rate compared to personal rates up to 45%, creating immediate savings on rental income.

Are there significant costs to maintaining a trust and company for property ownership?

Initial setup costs range from R15,000 to R30,000 including legal and registration fees. Annual ongoing costs typically run R20,000 to R40,000 for accounting, tax returns, and compliance services. These expenses are often offset by tax savings within the first few years, especially for properties generating substantial rental income.

How does dividends tax impact distributions from the company to the trust?

When the company distributes profits to the trust as dividends, a 20% dividends tax applies to the distribution amount. This tax is withheld by the company before paying the trust. Strategic planning around distribution timing and amounts helps minimize the overall tax impact while maintaining necessary cash flow for beneficiaries.

Can I be both the trustee and a beneficiary of the trust owning my company?

Yes, South African law permits you to serve as both trustee and beneficiary, though this creates potential conflicts of interest. You must maintain clear separation between your roles and document all decisions properly. Many advisors recommend having independent trustees or co-trustees to strengthen governance and demonstrate arm’s length decision making to SARS.

What are the key compliance risks to avoid with this structure?

The biggest risks include mixing personal and business funds, failing to maintain separate accounting records, and neglecting annual filing requirements. Missing company annual returns can result in deregistration. Poor documentation allows SARS to challenge the structure’s legitimacy. Regular professional reviews and systematic recordkeeping eliminate these risks. Implementing smart tax strategies with expert guidance ensures you maintain all benefits while staying fully compliant.

Recommended

- How to save tax in South Africa: smart strategies for SMEs in 2026 – Ready Accounting

- Year-End Tax Planning Guide for Small Businesses – Ready Accounting

- Small Business Tax Deductions: Complete 2025 Checklist – Ready Accounting

- Top Tax Questions Small Business Owners Ask in 2025 – Ready Accounting

- Investment Property Loans Australia | Rates From 5.20% | OptiCheck