How to manage business finances effectively for SMEs

Executive Summary

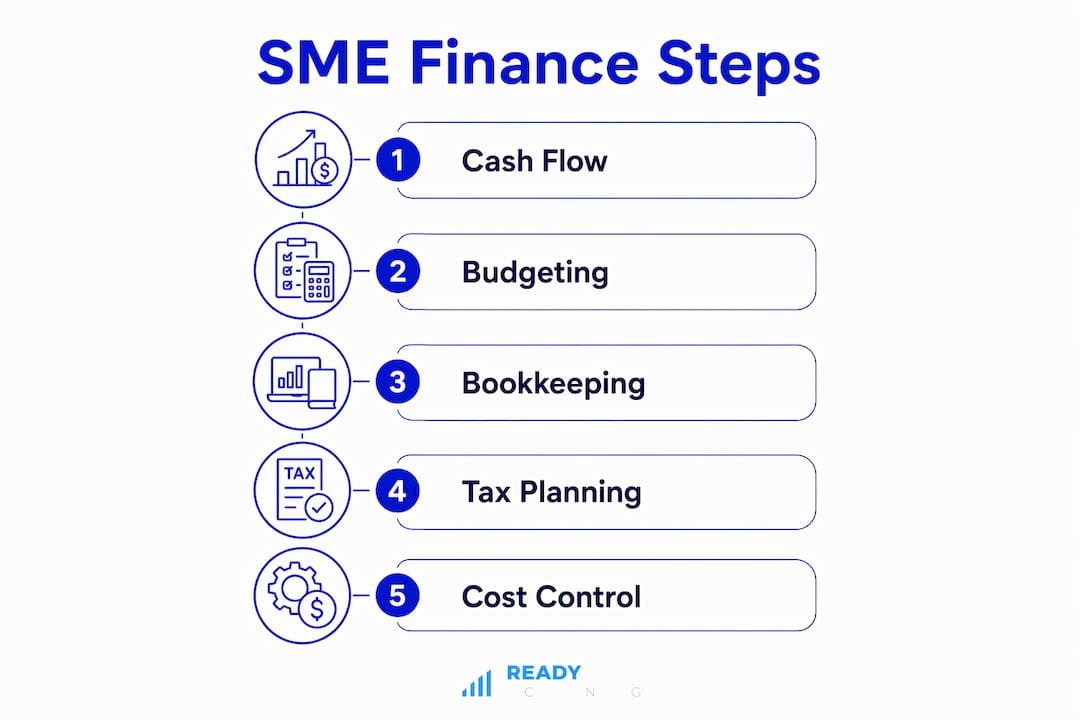

- Effective financial management for South African SMEs involves disciplined cash flow, budgeting, bookkeeping, tax planning, and cost control practices. Regularly updating forecasts, maintaining cash reserves, separating personal and business finances, and tracking key KPIs enable proactive decision-making and liquidity management. Automating processes with cloud tools like Xero or QuickBooks supported by expert guidance helps SMEs plan ahead and reduce SARS liabilities efficiently.

Effective financial management is the process of organizing, controlling, and analyzing your business’s money to sustain operations and drive growth. For South African SMEs, this means mastering five core disciplines: cash flow management, budgeting, bookkeeping, financial reporting, and tax planning. Without a structured approach to these areas, even profitable businesses run into liquidity crises or SARS penalties. Tools like Xero, QuickBooks, and cloud accounting platforms built for South Africa make it far more practical to manage business finances effectively for SMEs today than it was even five years ago.

How can SMEs improve cash flow management?

Cash flow is not the same as profit. A business can show a healthy net income on its income statement while simultaneously running out of money to pay suppliers. This disconnect kills more SMEs than poor sales do.

The most reliable tool for preventing cash shortfalls is a 13-week rolling cash flow forecast updated weekly. This forecast maps every expected inflow and outflow across the next quarter, giving you a clear view of gaps before they become crises. Weekly updates keep the model accurate as conditions shift.

Faster collections are equally critical. Automated invoice reminders sent at 7, 14, and 30 days past due recover outstanding payments without requiring awkward personal calls. Pair this with shorter payment terms on new contracts, and your average collection period drops meaningfully.

On the reserves side, SMEs should maintain cash reserves equal to at least three months of operating expenses. This buffer absorbs seasonal dips, late-paying clients, and unexpected costs without forcing you into emergency borrowing. For South African businesses dealing with load shedding costs and rand volatility, this reserve is not optional.

- Invoice immediately upon delivery, not at month end

- Offer early payment discounts of 1-2% to incentivize faster settlement

- Review your debtor book weekly, not monthly

- Keep a separate bank account for tax obligations so VAT and income tax funds are never accidentally spent

Pro Tip: Set aside 25-30% of net revenue into a dedicated tax account every month. This single habit eliminates the most common cash flow shock South African SMEs face: a large SARS bill with no funds to pay it.

You can explore more practical approaches in this guide on cash flow for SA SMEs.

What are the best budgeting practices for South African SMEs?

A budget is a fixed plan for a defined period. A forecast is a living estimate that updates as reality unfolds. SMEs need both, and confusing the two leads to either rigidity or chaos.

The most effective approach combines two methods. Hybrid budgeting applies zero-based budgeting to major fixed costs like rent, salaries, and equipment, where every rand must be justified from scratch. For stable recurring expenses, incremental budgeting applies small percentage adjustments to the prior year’s figures. This saves time without sacrificing accuracy where it matters most.

Here is a practical five-step process for building your annual budget:

- Start with revenue. Set targets based on confirmed contracts, historical trends, and realistic growth assumptions. Avoid optimism bias.

- List all fixed costs. Rent, insurance, salaries, and loan repayments go here. These do not change with revenue.

- Estimate variable costs. Cost of goods sold, commissions, and utilities scale with activity. Tie these to your revenue assumptions.

- Add a contingency buffer. A 5-15% contingency buffer on total expenses protects against surprises without requiring a full reforecast every time something unexpected happens.

- Allocate for tax and compliance. Budget explicitly for VAT submissions, provisional tax payments, and CIPC annual returns. These are not optional costs and should never be treated as residual.

Monthly reviews of management accounts against your budget are what turn a budget from a document into a decision tool. When actuals diverge from plan, you investigate the cause and adjust the rolling forecast for the next quarter. This discipline separates businesses that grow intentionally from those that grow by accident.

| Budget component | Recommended approach |

|---|---|

| Major fixed costs | Zero-based: justify every rand annually |

| Stable recurring costs | Incremental: adjust prior year by a set percentage |

| Variable costs | Tie directly to revenue forecast assumptions |

| Contingency | Add 5-15% buffer on total expense line |

| Tax obligations | Allocate monthly; never treat as residual |

Pro Tip: Update your rolling forecast quarterly, not just annually. A 12-month rolling forecast updated every quarter keeps your financial picture current and reduces the shock of year-end surprises.

For a deeper look at why this discipline matters, read Readyaccounting’s guide on SME budgeting for growth.

How does accurate bookkeeping support better decisions?

Bookkeeping is the foundation every other financial discipline rests on. If your records are incomplete or delayed, your cash flow forecast is guesswork, your budget comparisons are meaningless, and your tax submissions are a liability.

The first rule is non-negotiable: separate personal and business finances from day one. Mixing the two creates compliance risk with SARS, distorts your profitability picture, and makes an audit genuinely painful. Open a dedicated business bank account and route every business transaction through it.

Cloud accounting software removes most of the manual burden. Xero and QuickBooks both offer South African localization, including VAT return preparation and SARS-compatible reporting. Cloud accounting tools like these give you real-time visibility into your financial position rather than a monthly snapshot that is already three weeks old by the time you see it.

The three financial statements every SME owner must understand are:

- Profit and loss (income statement). Shows revenue, expenses, and net profit over a period. Use it to track whether the business is generating surplus.

- Balance sheet. Shows assets, liabilities, and equity at a point in time. Use it to assess solvency and net worth.

- Cash flow statement. Shows actual money in and out. Use it alongside the P&L to understand why profit and cash sometimes move in opposite directions.

Beyond these statements, track a small set of KPIs monthly. A current ratio between 1.5 and 2.0 signals healthy liquidity. Gross profit margin, net profit margin, and accounts receivable days round out a dashboard that tells you whether the business is healthy before problems become visible to the naked eye.

For a practical introduction to reading these reports, the financial statement guide from Readyaccounting is a useful starting point.

What tax planning steps should South African SMEs follow?

Tax planning and tax filing are not the same activity. Filing is what you do when a deadline arrives. Planning is what you do every month to reduce what you owe legally and avoid penalties.

South African SMEs typically deal with four main tax obligations: VAT (submitted bi-monthly or monthly depending on turnover), provisional income tax (paid twice yearly to SARS), employees’ tax (PAYE submitted monthly), and capital gains tax on asset disposals. Each has its own deadlines, and missing any of them triggers interest and penalties that compound quickly.

Year-round tax planning that includes monthly tax set-asides and quarterly reviews with a tax advisor reduces both your liability and your stress. The businesses that get hit hardest by SARS bills are those that treat tax as an annual event rather than a monthly discipline.

Key practices to implement:

- Set aside 25-30% of net income monthly into a dedicated tax account

- Review your provisional tax estimate quarterly and adjust if revenue has shifted significantly

- Claim all legitimate deductions: home office costs, business travel, equipment depreciation, and professional fees

- Consider your entity structure. A (Pty) Ltd often offers tax advantages over a sole proprietorship once turnover exceeds a certain threshold, and a SAIPA or SAICA-registered accountant can advise on the right structure for your situation

- Use the Small Business Corporation (SBC) tax regime if you qualify. The SBC rate structure is more favorable than the standard corporate rate for businesses with turnover below R20 million

Pro Tip: Quarterly SARS reviews with your accountant catch under-provisioning early. Adjusting your provisional tax payment before the deadline costs nothing. Paying interest and penalties after the fact costs significantly more.

Which cost control strategies keep SMEs financially healthy?

Cost control is not about cutting everything. It is about knowing exactly what you spend, why you spend it, and whether each rand is generating a return.

Start by classifying every expense as fixed or variable. Fixed costs like rent and salaries continue regardless of revenue. Variable costs like raw materials and delivery fees scale with output. This classification matters because your response to a revenue shortfall differs depending on which type of cost is driving your burn rate.

Tracking KPIs aligned to your business stage gives you early warning before problems become crises. The operating expense ratio (operating costs divided by revenue) tells you how efficiently the business converts revenue into profit. A rising ratio over three consecutive months is a signal to investigate, not ignore. The cash conversion cycle measures how long it takes to turn inventory and receivables into cash. A lengthening cycle means capital is getting trapped in the business.

Practical cost control measures that work for South African SMEs include:

- Set spending approval thresholds. Any expense above a defined amount requires sign-off, which prevents uncontrolled discretionary spending

- Review your supplier contracts annually. Loyalty rarely translates into the best price, and renegotiating terms is often easier than owners expect

- Monitor your gross profit margin monthly. A declining margin usually signals either pricing pressure or rising input costs, both of which require a strategic response

- Use your accounting software’s budget alerts to flag when a cost category exceeds its monthly allocation

The goal is not to run a lean business at the expense of growth. Strategic investment in people, technology, and capacity generates returns. The discipline is in distinguishing between spending that builds the business and spending that simply maintains the status quo.

Key takeaways

Effective SME financial management requires consistent discipline across cash flow, budgeting, bookkeeping, tax planning, and cost control, not a single fix applied once.

| Point | Details |

|---|---|

| Cash flow before profit | Maintain a 13-week rolling forecast and a 3-month cash reserve to prevent liquidity crises. |

| Budget with a buffer | Apply hybrid budgeting and add a 5-15% contingency buffer to absorb unexpected costs. |

| Separate finances from day one | Keep personal and business accounts apart to protect compliance and reporting accuracy. |

| Plan tax monthly, not annually | Set aside 25-30% of net income monthly and review your SARS position quarterly. |

| Track 5-10 core KPIs | Monitor gross margin, current ratio, and receivables days to catch problems early. |

Why most SMEs manage finances reactively, and how to change that

From working with South African SMEs across multiple sectors, the pattern I see most often is not ignorance of financial principles. It is the habit of reacting to financial information rather than using it to make decisions in advance.

Most business owners look at their bank balance to decide whether they can afford something. That is not financial management. That is financial archaeology. By the time the bank balance reflects a problem, the decisions that caused it were made weeks or months ago.

The shift that changes everything is moving from monthly retrospective reviews to weekly forward-looking ones. A 13-week cash flow forecast reviewed every Monday morning changes how you think about every decision that week. A monthly budget-versus-actual review that happens on the 5th of the following month, not the 25th, gives you time to respond rather than just record.

I also see too many SME owners avoid accounting software because they find it intimidating, then spend hours on manual spreadsheets that are always out of date. Xero and QuickBooks are not complicated once set up correctly, and the time saved in the first month alone justifies the subscription cost. If setup feels like a barrier, that is exactly the kind of friction a firm like Readyaccounting is built to remove.

Start simple. Separate your accounts. Build the forecast. Review it weekly. The sophistication can come later. The habit has to come first.

— Johan

How Readyaccounting helps SMEs take control of their finances

Readyaccounting works with scaling South African SMEs to replace manual financial processes with cloud infrastructure that delivers real-time visibility and tax protection. If your current setup means you are always catching up rather than planning ahead, that is a structural problem, not a discipline problem.

The team at Readyaccounting can automate your cash flow tracking, set up accurate financial reporting, and build a tax strategy that reduces your SARS liability legally and proactively. Explore how accounting automation improves cash flow for SMEs, or see the practical steps to improve your financial reporting for better decision-making. For tax-specific guidance, the page on reducing tax liability for SA SMEs covers the strategies most relevant to your situation.

FAQ

What is the most important financial habit for SMEs?

Separating personal and business finances from the start is the single most impactful habit. It protects SARS compliance, clarifies profitability, and makes every other financial process more accurate.

How often should SMEs review their budget?

Review management accounts against your budget every month and update your rolling forecast quarterly. Monthly reviews catch variances early enough to act on them.

What cash reserve should a South African SME maintain?

Aim for a cash reserve equal to three months of operating expenses. This buffer covers seasonal gaps, late-paying clients, and unexpected costs without requiring emergency credit.

Which accounting software suits South African SMEs best?

Xero and QuickBooks both offer South African VAT and SARS-compatible features. The right choice depends on your business size and integration needs, but either platform outperforms manual spreadsheets significantly.

How can SMEs reduce their SARS tax bill legally?

Year-round tax planning, including monthly set-asides, claiming all legitimate deductions, and reviewing your entity structure with a SAIPA or SAICA-registered accountant, reduces your liability without risk. Quarterly provisional tax reviews prevent under-provisioning penalties.