Execution Framework: create a cashflow forecast statement in 2026

Managing cashflow effectively separates thriving small businesses from those constantly scrambling to cover expenses. 60% of small to medium-sized enterprises struggle with cash flow management, making accurate forecasting essential for survival and growth. This guide walks you through creating a practical cashflow forecast statement tailored to South African small businesses, helping you anticipate cash shortages, plan investments confidently, and make smarter financial decisions. You’ll learn proven methods, avoid common pitfalls, and discover how automation transforms forecasting from guesswork into reliable financial planning.

Table of Contents

- Understanding The Importance Of Cashflow Forecasting For Small Businesses

- Preparing To Create Your Cashflow Forecast Statement

- Step-By-Step Guide To Building Your Cashflow Forecast Statement

- Common Mistakes And How To Verify Your Cashflow Forecast

- Enhance Your Cashflow Forecasting With Ready Accounting

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Cashflow forecasts track liquidity | They project expected cash inflows and outflows to help you anticipate when money enters and leaves your business. |

| Two main forecasting methods exist | Direct method itemizes transactions for short-term precision, while indirect method adjusts net income for longer-term planning. |

| Automation reduces forecast errors | Automated data collection eliminates manual entry mistakes and saves hours of repetitive work each week. |

| Regular reconciliation is critical | Comparing forecasted versus actual cash flows monthly catches errors early and improves future accuracy. |

| Accurate forecasts enable growth | Reliable forecasting supports confident financial decisions, prevents cash crunches, and identifies investment opportunities. |

Understanding the importance of cashflow forecasting for small businesses

Cashflow forecasting tracks actual money moving through your business, distinct from profit calculations that include non-cash items like depreciation and accrued revenue. While your income statement might show healthy profits, poor cash timing can leave you unable to pay suppliers or staff.

The statistics paint a sobering picture. Beyond the 60% of SMEs struggling with cash flow management, cash flow assistance ranks among the most requested types of small business funding after start-ups and expansion capital. This widespread need reflects how challenging forecasting becomes when juggling multiple revenue streams, seasonal fluctuations, and unpredictable customer payment patterns.

Poor cashflow forecasting creates cascading problems:

- Inability to meet payroll or supplier obligations on time

- Missed growth opportunities due to insufficient working capital

- Emergency borrowing at unfavorable terms

- Damaged business relationships from late payments

- Stress and reactive decision-making instead of strategic planning

South African SMBs face unique challenges including economic volatility, load shedding impacts on operations, and customers stretching payment terms during tough periods. These factors make accurate forecasting even more critical for maintaining stability.

“Without visibility into future cash positions, businesses operate blindly, unable to distinguish between temporary cash crunches and fundamental financial problems.”

Mastering cashflow forecasting protects against seasonal swings and unexpected disruptions. It transforms financial management from reactive firefighting into proactive planning. When you know exactly when cash arrives and departs, you can negotiate better terms with suppliers, time major purchases strategically, and build reserves for genuine emergencies. Understanding cash flow problems and solutions helps you recognize warning signs early. Common cash flow forecast problems and solutions include addressing timing mismatches and improving collection processes.

Accurate forecasting underpins every sound financial decision. It answers critical questions: Can we afford that new hire? Should we accept this large order? Is now the right time to expand? Without reliable forecasts, these decisions become gambles rather than calculated moves.

Preparing to create your cashflow forecast statement

Before building your forecast, gather the right inputs and tools. Quality forecasting depends entirely on accurate, complete data. Garbage in means garbage out, so invest time in this preparation phase.

Start by collecting these essential data types:

- Sales forecasts: Projected revenue by product, service, or customer segment with realistic timing

- Accounts receivable: Outstanding invoices, typical payment terms, and historical collection patterns

- Accounts payable: Upcoming bills, supplier payment terms, and recurring expenses

- Loan obligations: Principal and interest payments with exact due dates

- Planned expenses: Payroll, rent, utilities, taxes, and anticipated one-time costs

- Seasonal patterns: Historical data showing how cash flows vary throughout the year

| Data Type | Why It Matters | Common Sources |

|---|---|---|

| Historical cash flows | Establishes baseline patterns and seasonal trends | Bank statements, accounting software |

| Customer payment behavior | Predicts realistic collection timing | Aged receivables reports, payment history |

| Supplier terms | Determines when cash leaves the business | Purchase orders, vendor agreements |

| Recurring obligations | Ensures fixed costs are never overlooked | Loan documents, lease agreements |

Gathering accurate historical financial data dramatically improves forecast reliability. Review at least six months of bank statements and accounting records to identify patterns. Notice when customers typically pay, how seasonal demand affects revenue, and which months carry higher expenses.

For tools, you have two main options. Spreadsheets like Excel or Google Sheets work for simple businesses with straightforward cash flows. They’re free, flexible, and familiar. However, manual data entry is vulnerable to human error, with mistyped numbers and formula mistakes causing significant problems. Specialised forecasting software or cloud accounting platforms offer automation, real-time updates, and better accuracy but require investment.

Pro Tip: Automate data collection wherever possible. 76% of data entry workers spend up to three hours daily moving data between systems. Connecting your bank feeds, invoicing system, and accounting software eliminates repetitive manual work and slashes error rates. Learn how automation improves cash flow management efficiency.

Watch for common bookkeeping mistakes that corrupt your input data. Miscategorized transactions, forgotten expenses, and delayed recording all skew forecasts. Clean, current books are non-negotiable for reliable forecasting.

Errors at this stage cascade through your entire forecast, rendering it useless for decision-making. A single misplaced decimal or forgotten recurring payment can show false surplus or crisis. Double-check every input, verify totals against bank balances, and confirm that all regular obligations appear in your data.

Step-by-step guide to building your cashflow forecast statement

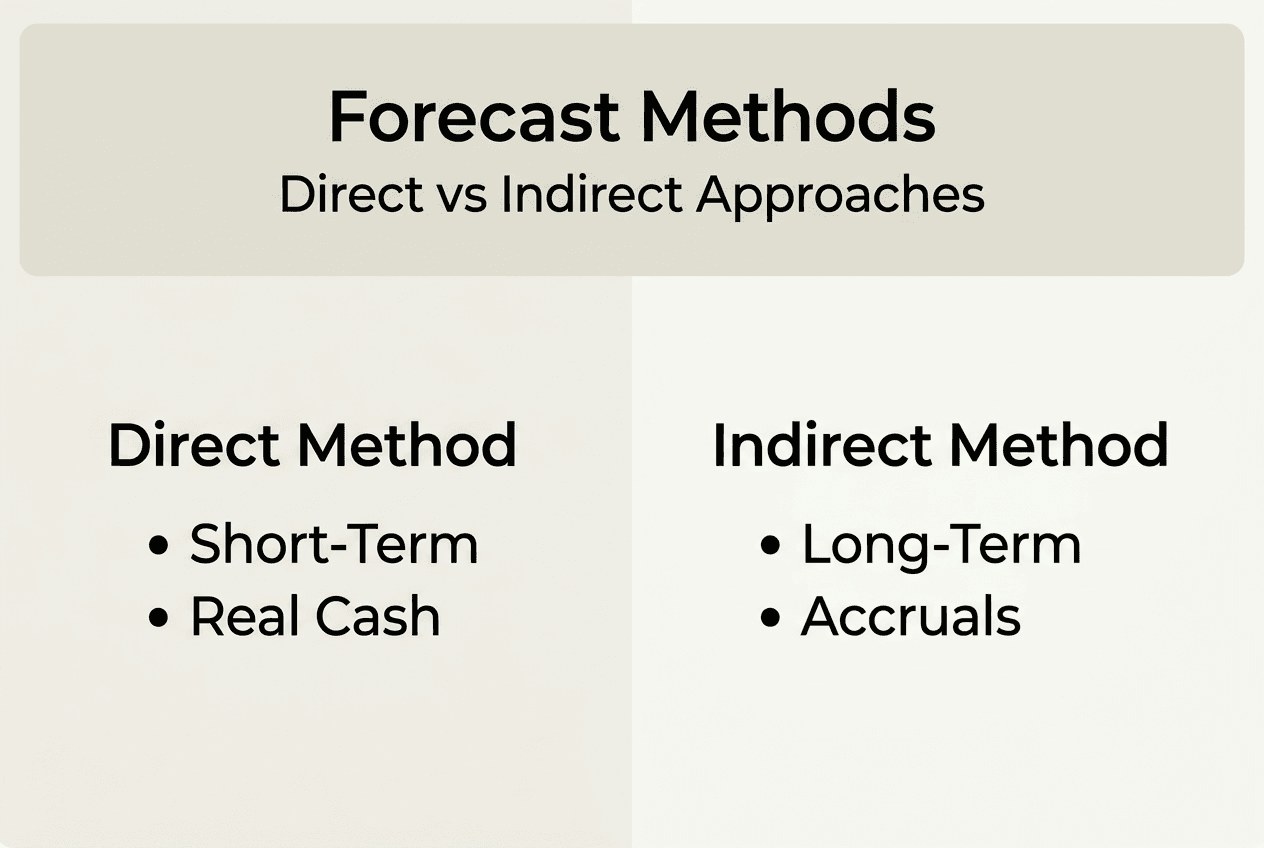

Now apply your preparation to construct the actual forecast. You’ll choose between two proven methods, each suited to different business needs and planning horizons.

| Method | Best For | Advantages | Disadvantages |

|---|---|---|---|

| Direct | Short-term operational planning, volatile cash flows | Precise transaction-level detail, easy to understand | Time-consuming, requires detailed tracking |

| Indirect | Longer-term strategic planning, stable businesses | Uses existing accounting data, aligns with standards | Less granular, harder to spot specific issues |

The direct method is ideal for SMBs needing precise, short-term cash visibility, especially during operational peaks and troughs. It itemizes every expected cash transaction: each customer payment, supplier bill, payroll run, and loan payment. This granular approach helps you manage daily or weekly cash positions with confidence.

For example, a seasonal retail business planning for December would forecast specific sales receipts based on historical holiday patterns, list every supplier payment for inventory purchases, schedule staff wages including holiday bonuses, and include rent, utilities, and loan payments with exact dates. This detail reveals precisely when cash tightens and when surplus accumulates.

The indirect method suits longer-term financial planning and aligns with accounting standards. It starts with projected net income, then adjusts for non-cash items like depreciation and changes in working capital based on historical ratios. This approach works well for monthly or quarterly forecasts when transaction-level detail becomes impractical.

Follow these steps to build your forecast:

- Choose your timeframe and method: Decide whether you need daily, weekly, or monthly forecasts and select direct or indirect method accordingly.

- Set your starting cash balance: Use your current bank balance as the opening position.

- Project cash inflows: List all expected receipts with realistic timing, accounting for typical payment delays.

- Project cash outflows: Detail every anticipated payment including fixed costs, variable expenses, and one-time items.

- Calculate net cash flow: Subtract total outflows from total inflows for each period.

- Determine ending balance: Add net cash flow to starting balance, which becomes the next period’s starting point.

- Identify shortfalls and surpluses: Highlight periods where cash dips below minimum operating levels or builds excess reserves.

- Plan responses: Decide how to address predicted shortfalls through financing, collection acceleration, or expense timing adjustments.

Pro Tip: Start simple with a basic three-month forecast using broad categories. As you gain confidence and refine your process, gradually add detail and extend your timeframe. Perfectionism at the start creates overwhelm and delays the benefits of forecasting.

Regularly comparing your forecast with actual results is crucial for improvement. Each month, review where predictions missed reality. Did customers pay slower than expected? Were expenses higher? Understanding these variances helps you adjust assumptions and improve future accuracy. Tracking key cash flow KPIs provides measurable benchmarks for forecast effectiveness.

Your forecast is a living document, not a one-time exercise. Update it as circumstances change, incorporating new information about sales, expenses, or business conditions. This ongoing refinement transforms forecasting from a compliance task into a strategic advantage.

Common mistakes and how to verify your cashflow forecast

Even well-intentioned forecasts fail when common errors creep in. Recognizing these pitfalls and implementing verification processes protects the reliability your business depends on.

Top forecasting mistakes include:

- Failing to update forecasts regularly: Stale forecasts based on outdated assumptions provide false confidence and mislead decisions.

- Ignoring timing differences: Recording revenue when invoiced rather than when cash actually arrives creates dangerous gaps between forecast and reality.

- Omitting small recurring transactions: Forgotten subscriptions, minor fees, and irregular expenses accumulate into significant amounts.

- Using overly optimistic assumptions: Hoping customers pay on time or sales exceed targets sets you up for cash shortfalls.

- Neglecting seasonal patterns: Failing to account for predictable fluctuations in revenue or expenses causes avoidable surprises.

- Mixing cash and accrual accounting: Confusing profit with cash flow by including non-cash items distorts your forecast.

“A common pitfall is failing to reconcile forecasted cash flows with actual cash flows regularly, leading to inaccurate assumptions that compound over time and erode forecast reliability.”

Monthly reconciliation comparing forecasted cashflow with actual bank and accounting data is non-negotiable. This process catches errors early, validates your assumptions, and builds confidence in your forecasting methodology. Set aside time each month-end to review variances, investigate significant differences, and update your model.

Create a simple variance analysis:

- Compare forecasted versus actual cash balance

- Identify the three largest variances in inflows and outflows

- Determine root causes: timing differences, incorrect assumptions, or missed transactions

- Adjust future forecasts based on lessons learned

- Document patterns to improve next period’s accuracy

Pro Tip: Manual tracking in Excel quickly becomes a bottleneck and error source. Automation is crucial for accuracy. Cloud accounting software with bank feed integration updates forecasts automatically, flags unusual transactions, and enables more frequent validation without additional work. The time saved pays for the software investment many times over.

Keep a forecast error log tracking recurring discrepancies. If customers consistently pay 10 days later than terms, adjust your collection assumptions. If a particular expense category always runs higher, revise your budgets. This systematic learning transforms forecasting from guesswork into science.

Verification builds the confidence needed for proactive financial management. When you trust your forecast, you can make bold moves like accepting larger orders, investing in equipment, or hiring ahead of growth. Without verification, doubt paralyzes decision-making. Understanding how to read cash flow statements helps you validate forecast accuracy against actual financial reports.

Consistent validation also reveals when external factors require forecast adjustments. Economic shifts, new competitors, regulatory changes, or operational disruptions all impact cash flows. Regular verification ensures your forecast reflects current reality rather than outdated assumptions.

Enhance your cashflow forecasting with Ready Accounting

Creating accurate cashflow forecasts requires the right tools, expertise, and systems. Ready Accounting provides South African small businesses with cloud-based solutions that transform forecasting from tedious spreadsheet work into automated, reliable financial intelligence.

Our cloud accounting benefits for small businesses include real-time visibility into cash positions, automated bank reconciliation, and integrated forecasting tools that eliminate manual data entry. These capabilities reduce errors, save hours each week, and provide the accuracy needed for confident decision-making.

Explore our comprehensive cloud-based accounting guide for South African SMB growth to understand how modern financial management platforms support better forecasting. Discover how automation improves cash flow by connecting your financial systems and providing instant insights.

Ready Accounting serves as your trusted partner in building financial systems that support growth. Our expertise in South African business requirements, combined with cutting-edge technology, helps you move from reactive cash management to proactive financial planning.

FAQ

How often should I update my cashflow forecast?

Update your cashflow forecast at least monthly to reflect current business conditions and actual results. Businesses with volatile cash flows, seasonal operations, or rapid growth benefit from weekly or even daily updates. More frequent updates improve accuracy, enable faster responses to emerging issues, and build forecasting discipline that strengthens financial management.

What is the difference between cash flow and profit?

Profit reflects earnings after expenses on your income statement, including non-cash items like depreciation and accrued revenue. Cash flow tracks actual money moving in and out of your business, not just accrued amounts. You can be profitable on paper while facing cash shortages if customers delay payments or you’ve invested heavily in inventory.

Which cashflow forecasting method is best for small businesses?

The direct method is ideal for SMBs needing precise, short-term cash visibility, especially when managing day-to-day operations and volatile cash flows. The indirect method suits longer-term financial planning and aligns with accounting standards for monthly or quarterly forecasts. Choose based on your timeframe, business complexity, and whether you need transaction-level detail or strategic overview.

What is a realistic cash buffer for small businesses?

Most financial advisors recommend maintaining cash reserves covering three to six months of operating expenses. This buffer protects against unexpected disruptions, seasonal downturns, and delayed customer payments. Start by calculating your average monthly fixed costs, then build reserves gradually through consistent forecasting and cash management discipline.

How do I improve collection timing to match my forecast?

Improve collections by invoicing immediately upon delivery, offering early payment discounts, sending payment reminders before due dates, and following up promptly on overdue accounts. Clear payment terms, multiple payment options, and building strong customer relationships also accelerate cash inflows. Track collection patterns to set realistic forecast assumptions rather than hoping for on-time payments.

Recommended

- Annual Financial Statements in South Africa: What Business Owners Need to Know for 2025 – Ready Accounting

- How Automation Improves Cash Flow – Ready Accounting

- Financial Statement Basics: A Guide for Business Owners – Ready Accounting

- How to Read Cash Flow Statement for Business Owners – Ready Accounting

- Placement de la trésorerie d’entreprise – Guide pratique et stratégies pour 2026 – Balmont Conseil

- Nectar | Case Study -Strategy For Long Term Growth