Grasp the basic principles of auditing for SA SME success

Executive Summary

- Most South African SME owners view audits as burdens rather than strategic tools for growth and risk management.

- A well-conducted audit offers credible financial verification that can improve funding prospects, regulatory compliance, and internal control.

Most South African SME owners treat audits as a grudge obligation, something to survive every financial year rather than a tool to grow and protect the business. This mindset is both common and costly. When you misunderstand what an audit actually measures, you leave yourself exposed to SARS scrutiny, struggle to access funding, and miss early warnings about financial leaks inside your own company. This article breaks down what auditing principles mean in practical terms, when the law requires you to comply, and how a well-run audit process can become one of your strongest business assets.

Table of Contents

- What is an audit? Key definitions and objectives for SMEs

- Fundamental principles that drive effective audits

- The risk-based approach: How audits target what matters most

- Statutory audit triggers: When must South African SMEs comply?

- The business benefits of auditing: SARS, compliance, and beyond

- Our perspective: Stop treating audits as a once-a-year fire drill

- Ready Accounting can make your audit process effortless

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Audit clarity for SMEs | Understanding audit basics empowers you to comply with the law and build business credibility. |

| Focus on key principles | Ethics, skepticism, judgment, and risk-based focus are at the heart of every effective audit. |

| Know your obligations | Calculating your Public Interest Score reveals if you need a statutory audit or an alternative. |

| Compliance brings benefits | Audited accounts reduce SARS risk, support funding, and improve your business decision-making. |

What is an audit? Key definitions and objectives for SMEs

With those misconceptions in mind, let’s clarify exactly what an audit is and why it truly matters for your business.

An audit is an independent examination of your financial statements by a qualified professional. That professional reviews your records, tests your transactions, and then issues a formal opinion on whether your financials give a true and fair view of the business. It is not a tax return, not a bookkeeping cleanup, and not a punishment. It is, at its core, a structured process of verification that gives everyone who reads your financials, from banks to investors to SARS, confidence that the numbers are real.

In South Africa, auditing standards adopted.pdf) by the Independent Regulatory Board for Auditors (IRBA) are governed by the International Standards on Auditing (ISAs). This means your audit is not conducted arbitrarily. There is a globally aligned framework that your auditor must follow, which makes your financial statements credible not just locally but internationally.

The term “reasonable assurance” is central to understanding what an audit actually delivers. Per ISA 200, the overall objective is to obtain reasonable assurance that financial statements are free from material misstatement, whether caused by fraud or error, and to express an opinion based on the applicable financial reporting framework. Reasonable assurance does not mean perfection. It means that after thorough testing and evidence gathering, the auditor has a high level of confidence in what the statements show.

Below a full audit, you have two lighter options: an independent review and a compilation. A compilation is the most basic level, where an accountant simply organises your data into financial statement format with no assurance provided. An independent review sits in the middle, providing limited assurance using enquiries and analytical procedures rather than deep transaction testing. A full audit gives the highest level of assurance and is the most resource-intensive of the three.

“An audit is more than a checkpoint. It is a tool for business growth and risk reduction.” Understanding this reframes the entire exercise from a compliance headache into a strategic investment.

Building reporting integrity for SA SMEs starts with knowing which type of assurance your stakeholders actually need. A bank financing your expansion will almost certainly want audited statements. A private investor will too. Properly understanding audited financial statements is one of the quickest ways to improve your funding eligibility.

Main parties involved in an SME audit:

- The business owner or management: Responsible for preparing the financial statements and providing accurate, complete information

- The independent auditor: A registered CA(SA) or RA who conducts the audit according to ISAs and issues the audit opinion

- The audit committee (if applicable): Oversees the audit process and acts as a bridge between management and the auditor

- SARS and regulators: Use audited financials to assess tax compliance and regulatory adherence

- Funders and investors: Rely on the audit opinion to evaluate whether the business is worth backing

Fundamental principles that drive effective audits

Now that you know what an audit is, let’s explore the key principles that ensure audits genuinely serve your business.

Audits are not just technical exercises. They are built on a set of ethical and professional standards that every registered auditor must uphold. According to FRC SME support guidance, key principles include compliance with relevant ethical requirements such as integrity, objectivity, professional competence, and confidentiality, as well as professional skepticism and professional judgment throughout the audit process.

Here is how each principle plays out in your business:

| Principle | What it means | Practical SME example |

|---|---|---|

| Integrity | The auditor is honest and straightforward | Auditor flags a suspicious expense claim even if it embarrasses management |

| Objectivity | No bias or conflicts of interest | Auditor cannot audit a business where they are also a shareholder |

| Professional competence | Staying current with laws and standards | Auditor knows the latest SARS VAT rulings before reviewing your returns |

| Confidentiality | Your financial data stays private | Auditor cannot share your turnover figures with third parties |

| Professional skepticism | Questioning evidence rather than accepting it at face value | Auditor verifies a large supplier invoice instead of trusting it as genuine |

| Professional judgment | Applying expertise to complex decisions | Auditor decides whether an accounting estimate is within an acceptable range |

Professional skepticism deserves special attention because it is often misunderstood. It does not mean your auditor thinks you are dishonest. It means they maintain a questioning mindset and remain alert to inconsistencies, regardless of how trustworthy management seems. This protects you from errors and fraud that might otherwise go undetected. A business owner who understands this will cooperate openly, knowing the process is designed to protect them.

Pro Tip: Build the same healthy skepticism inside your own business. Require dual authorisation on payments, reconcile bank accounts monthly, and question unusual variances. Internal controls that mirror audit principles make external audits faster and far less stressful. Learn more about aligning your numbers with financial KPI examples that signal early when something is off.

Integrity in reporting is not just an ethical choice. It is a financial one. Businesses with strong internal controls get through audits faster, pay less in audit fees, and face fewer queries from SARS.

The risk-based approach: How audits target what matters most

Ethics and skepticism set the tone, but how is an audit conducted day to day in an SME? It all starts with targeting the real risks.

Modern auditing is risk-based. That means your auditor does not check every single invoice or transaction. Instead, they focus resources on higher-risk areas like specific transactions, account balances, and disclosures where mistakes or deliberate misstatements are most likely to occur. For an SME, this approach makes audits more efficient and more focused on the areas that actually matter.

For South African SMEs, the highest-risk areas typically include cash transactions (especially where cash sales are common), revenue recognition, intercompany loans, director drawings, tax liabilities, and stock or inventory counts. If your business handles large volumes of cash or has complex related-party dealings, expect your auditor to spend significant time in those areas.

The good news is that you can prepare for this. Knowing where auditors focus gives you a checklist for getting your own house in order before fieldwork begins. Strong preparation reduces audit time, reduces audit fees, and dramatically reduces the chance of a qualified opinion, which is the last thing you want on a set of financials you are about to show to a bank.

Understanding how to properly manage risk in accounting is one of the most practical skills an SME owner can develop. It feeds directly into how smoothly your audit runs.

Documents every SME should keep organised and ready:

- Signed bank statements for all accounts, reconciled monthly

- Supplier invoices and proof of payment for all expenses above R500

- Revenue records matched to bank deposits, with any cash sales logged separately

- Asset registers showing purchase dates, costs, and depreciation calculations

- Director loan accounts with full supporting schedules

- VAT returns and supporting calculations for the full financial year

- Payroll records including IRP5 submissions and UIF/SDL calculations

- Any contracts with major customers or suppliers that affect how income is recognised

Pro Tip: Run a mini internal audit at the six-month mark of your financial year. Pull a sample of 20 transactions, check that each one is supported by documentation, and reconcile your top five balance sheet accounts. This single habit can cut external audit fieldwork time by 30% or more.

Statutory audit triggers: When must South African SMEs comply?

Understanding core principles is key, but SME owners really want to know: Am I legally required to audit my business? Here’s how to find out.

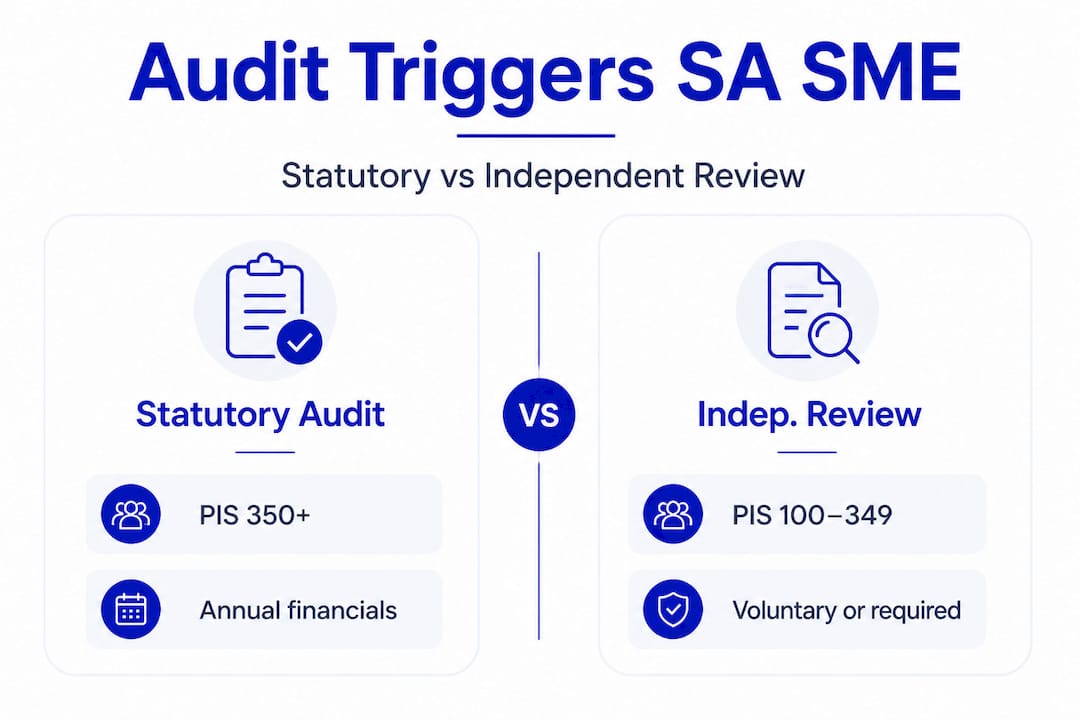

The answer depends on your Public Interest Score (PIS), a number calculated annually based on four factors: the number of employees (1 point each), third-party liabilities in millions of rand (1 point per R1 million), the number of shareholders who are not directors (1 point each), and annual turnover in millions divided by 10 (rounded to the nearest integer).

According to the Companies Act requirements, a full statutory audit is required when your PIS is 350 or more. If your PIS falls between 100 and 349 and your financial statements were compiled internally (by your own staff or management), you also need a full statutory audit.

Here is a comparison to help you decide which level of assurance applies to your business:

| Requirement | Audit | Independent review | Compilation |

|---|---|---|---|

| PIS threshold | 350 or above | 100 to 349 (independently compiled) | Below 100 |

| Assurance level | Reasonable (high) | Limited | None |

| Who performs it | Registered auditor (RA) | CA(SA) or RA | Any accountant |

| Typical cost | Highest | Moderate | Lowest |

| Stakeholder confidence | Strongest | Moderate | Minimal |

If your PIS sits between 100 and 349 and your statements were compiled by an independent accountant (not your own staff), you may qualify for an independent review under ISRE 2400, which provides limited assurance through analytical procedures and enquiries rather than full audit testing. This is a legitimate, cost-effective option for many smaller businesses.

Steps to determine your current compliance obligation:

- Calculate your PIS using the four factors above for your most recent financial year

- Identify whether your financial statements were compiled internally or by an independent party

- Match your PIS and compilation method to the table above

- Confirm with a registered accountant or auditor whether your calculation is correct

- Appoint the appropriate level of assurance provider before your financial year-end

Understanding your VAT and audit requirements is equally important here, because crossing VAT thresholds often signals that your PIS is climbing too.

The business benefits of auditing: SARS, compliance, and beyond

The legal triggers are only half the story. The practical business benefits of audits are just as important.

Let’s start with the number that should get every SME owner’s attention. SARS conducted 11,229 SME audits in the 2017/18 financial year alone, yielding R8.3 billion in additional revenue. That figure tells you two things: SARS has the capacity and appetite to audit small businesses at scale, and the average SME audit resulted in meaningful additional tax being assessed. Routine financial audits or independent reviews reduce your risk of landing in that group by keeping your records accurate, your reconciliations current, and your tax calculations defensible.

Beyond SARS compliance, audited financials open doors that are simply closed to businesses with unverified numbers. Banks require them for business loans above certain thresholds. Private equity investors and venture capital backers demand them before putting money in. Government tenders often require audited statements as part of the eligibility criteria. The business that has a clean audit opinion has a competitive advantage in funding conversations.

Auditing also improves internal decision-making. When your team knows the numbers will be independently verified, there is a natural incentive to keep records accurate and controls tight. Fraud and errors are caught earlier, cash flow is better understood, and financial forecasting becomes more reliable.

SME actions to reduce the risk of a SARS tax audit or penalties:

- Submit all tax returns on time, including VAT, PAYE, and income tax

- Reconcile your accounting records to your SARS e-filing submissions every month

- Maintain five years of supporting documents for all income and expense claims

- Avoid large, unexplained movements between personal and business bank accounts

- Ensure all related-party transactions are properly documented and at arm’s length

- Review your tax compliance protocol and check your SARS record-keeping rules obligations annually

Our perspective: Stop treating audits as a once-a-year fire drill

Here is the uncomfortable truth most accounting firms will not say out loud: if you only think about your audit when your auditor shows up, you have already failed the audit before it starts.

The businesses we work with that sail through audits share one habit. They treat their financial records as a live document, not an annual report. They reconcile in real time, they maintain documentation habits throughout the year, and they build internal controls that mirror what an auditor would test. By the time the auditor arrives, there is nothing to hide, nothing to find, and very little to fix.

The counterintuitive insight is that the cost of a good audit is mostly paid in the months before the audit, not during it. A business that invests in cloud-based bookkeeping, monthly reconciliations, and structured document management spends far less on external audit fees than one that scrambles to reconstruct a year of transactions in three weeks. The math is clear, even if the lesson takes a few painful audit cycles to land.

We also see too many SME owners avoid voluntary audits because they assume their business is too small to bother. But lenders, strategic partners, and even larger customers increasingly ask for assurance on financial data before they commit. An SME that can produce a clean set of reviewed or audited financials on short notice has a genuine edge. That is not a compliance win. That is a commercial one.

Ready Accounting can make your audit process effortless

At Ready Accounting, we work with South African SMEs and startups to build the financial infrastructure that makes audits a non-event rather than a crisis. Our cloud-based bookkeeping systems, real-time dashboards, and accounting basics frameworks are designed to keep your records audit-ready every single day of the year, not just in the weeks before your auditor arrives. Whether you need to understand your Public Interest Score, prepare for a SARS review, or build the financial credibility to unlock funding, our Fractional CFO team engineers the systems that give you that advantage. Explore how we can turn your finance function from a compliance burden into a growth engine at readyaccounting.co.za.

Frequently asked questions

What are the key ethical requirements in an audit?

Integrity, objectivity, professional competence, and confidentiality are the core ethical requirements for any SME audit, alongside professional skepticism and professional judgment.

How does professional skepticism impact an audit?

Professional skepticism means auditors maintain a questioning mindset and remain alert to potential fraud or error, rather than simply accepting management’s explanations at face value.

What is the minimum Public Interest Score for a statutory audit?

A statutory audit is required when your Public Interest Score reaches 350 or above, or between 100 and 349 if your financial statements were internally compiled.

How can auditing help reduce my SARS tax audit risk?

Routine audits keep your records accurate and reconciled, which directly reduces the risk factors that trigger a SARS SME audit and protects you from unexpected penalties.

Is an independent review enough for most SMEs?

If your Public Interest Score is below 350 and you meet the ISRE 2400 criteria, an independent review provides sufficient assurance at a significantly lower cost than a full audit.

Recommended

- Integrity in financial reporting: practical steps for SA SMEs | Ready Accounting

- Auditing financial statements: protocol for South African Corporate Assets | Ready Accounting

- Execution Framework: Audit Financial Records: Easy Protocol for SA Businesses | Ready Accounting

- Basic Accounting Principles for South African Businesses 2025 | Ready Accounting