GAAP explained: a practical guide for South African SMEs

Executive Summary

- Many South African SMEs mistakenly believe “GAAP” refers to local standards, risking compliance issues. South African businesses typically apply IFRS for SMEs, a simplified, principles-based standard aligned with international norms. Proper application of the correct framework enhances tax compliance, financial clarity, and business credibility.

Many South African business owners use the word “GAAP” loosely, assuming it describes the accounting rules they must follow. That assumption can be expensive. GAAP stands for Generally Accepted Accounting Principles, a rules-based framework used primarily in the United States. South African SMEs operate under a completely different set of standards, and mixing up the two creates real compliance risk, reporting errors, and unnecessary friction with SARS. This guide will clear up the confusion, help you identify exactly which framework applies to your business, and show you where the most common mistakes happen.

Table of Contents

- What is GAAP, and how does it differ from IFRS and IFRS for SMEs?

- Which accounting standard applies to your South African business?

- Special features and common pitfalls with IFRS for SMEs

- Why these frameworks matter for tax and financial reporting in South Africa

- Is IFRS for SMEs still fit for purpose? A practical view

- Need help navigating SME accounting standards? Here’s your next step

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| GAAP versus IFRS for SMEs | South African SMEs should follow IFRS for SMEs, not US GAAP, for clearer compliance. |

| Know your obligations | Your business’s Public Interest Score determines the right reporting standard and audit requirement. |

| Common pitfalls and tips | Misapplying inventory or missing disclosure rules are frequent mistakes—use pro tips to avoid them. |

| Tax and credibility benefits | The right framework simplifies tax reports and boosts lender and investor trust. |

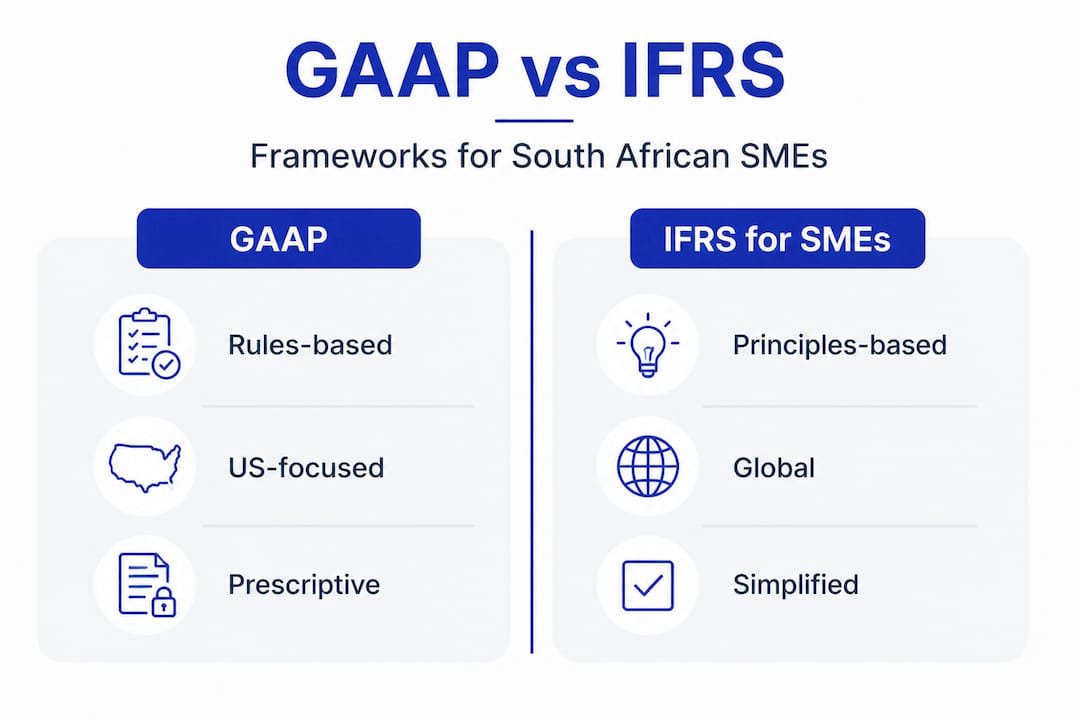

What is GAAP, and how does it differ from IFRS and IFRS for SMEs?

Let’s start with the basics, because the confusion here is understandable. Three distinct frameworks get thrown around in South African business conversations, and each one means something different.

GAAP is rules-based and US-driven. It provides specific, prescriptive rules for every scenario. Think of it as a rulebook where almost every situation has a pre-written answer. US-listed companies must use it, but South African companies do not.

Full IFRS (International Financial Reporting Standards) is the global framework used by large, publicly listed companies in South Africa and most of the world. It is principles-based, meaning it gives you the underlying logic and expects professional judgment to fill in the gaps. The Johannesburg Stock Exchange (JSE) requires listed entities to use full IFRS.

IFRS for SMEs is the version that most South African private companies actually use. It is a simplified standard with roughly 10% of full IFRS disclosure requirements, designed specifically for entities that do not have public accountability. Understanding your income statement and other core financial documents becomes much more manageable under this lighter framework.

Here is a direct comparison to make the differences concrete:

| Feature | US GAAP | Full IFRS | IFRS for SMEs |

|---|---|---|---|

| Origin | United States | International (IASB) | International (IASB) |

| Approach | Rules-based | Principles-based | Principles-based |

| Who uses it in SA | Nobody (not required) | JSE-listed companies | Most private SMEs |

| Document length | Thousands of pages | 3,000+ pages | ~230 pages |

| Disclosure burden | Very high | Very high | Reduced by ~90% |

| LIFO inventory method | Permitted | Prohibited | Prohibited |

The practical takeaway here is simple. If someone tells you your business needs to follow “GAAP,” ask them which GAAP they mean. In a South African context, what they almost certainly mean is IFRS for SMEs. Using the wrong framework is not just an academic problem. It affects how you recognise revenue, value inventory, and structure your balance sheet. You can review examples of financial statements prepared under each framework to see how different the outputs look in practice.

“The distinction between rules-based and principles-based accounting is not just philosophical. It changes how you handle judgment calls in your books every single month.”

Which accounting standard applies to your South African business?

Now that you understand the three frameworks, the next step is working out which one legally applies to your business. South Africa uses a system called the Public Interest Score (PIS) to determine your obligations under the Companies Act.

Your PIS is calculated based on four factors:

- Employees: Add one point for every employee your company has on average during the financial year.

- Third-party liability: Add one point for every R1 million owed to third parties at year-end (rounded to the nearest million).

- Turnover: Add one point for every R1 million in turnover during the financial year (rounded to the nearest million).

- Individual shareholders: Add one point for every individual (not company) who holds a beneficial interest in your shares.

Once you have your total score, your reporting obligations under the Companies Act are determined as follows:

| PIS Range | Audit Required? | Accounting Standard |

|---|---|---|

| 350 or above | Yes, mandatory audit | Full IFRS or IFRS for SMEs |

| 100 to 349 | Independent review | IFRS for SMEs or SA GAAP with review |

| Below 100 | Not required (if owner-managed) | IFRS for SMEs or simpler frameworks |

Here is a step-by-step process to work out your position:

- Pull your latest annual financial statements or management accounts.

- Count your average full-time-equivalent employees for the year.

- Add up your total third-party debt at year-end (bank loans, trade creditors, lease liabilities).

- Divide your turnover by R1 million and round to the nearest whole number.

- Count how many individual shareholders you have.

- Add all four numbers together to get your PIS.

- Match your score to the table above and confirm your reporting requirement with your accountant.

Pro Tip: If your business is owner-managed and your PIS sits below 100, you may qualify for a simpler reporting framework. However, if you have external investors, bank funding, or are planning to scale, voluntarily adopting IFRS for SMEs now will make future compliance far less disruptive. Pairing the right framework with solid tax planning removes a significant layer of year-end stress.

Special features and common pitfalls with IFRS for SMEs

After finding your framework, it is crucial to know what makes IFRS for SMEs distinct and where SA business owners most often stumble. The standard is shorter than full IFRS, but shorter does not mean simpler in every area.

Here are the key technical features that catch businesses off guard:

- No LIFO inventory method: IFRS for SMEs prohibits LIFO (Last In, First Out). You must use FIFO (First In, First Out) or the weighted average method. If you are importing goods or managing raw materials, this has a direct effect on your reported cost of sales and profit.

- Development costs can be capitalised: Unlike full IFRS, which requires strict criteria before capitalising development costs, IFRS for SMEs allows you to capitalise development costs under specific conditions. This matters if you are building software, creating new products, or investing in proprietary processes.

- Simplified lease accounting: The standard has less complex lease treatment than IFRS 16, which means less administrative burden for businesses with property or equipment leases.

- Reduced disclosure requirements: You do not need to produce every note and disclosure required under full IFRS, which cuts down the cost and time of preparing annual financial statements.

Where businesses most commonly go wrong:

- Using LIFO for inventory valuation because it was familiar from previous practice or from a US-based accounting system.

- Expensing all development spending immediately instead of evaluating whether capitalisation is appropriate.

- Ignoring the requirement to assess impairment of assets at each reporting date.

- Producing financial statements without the mandatory notes, assuming that shorter means fewer formal requirements.

Statistic callout: Less than 50% of South African SMEs adopted IFRS for SMEs after its introduction in 2007, largely due to perceived complexity. Yet the standard runs to only around 230 pages compared to 3,000 pages for full IFRS, with disclosures reduced by roughly 90%.

That adoption gap is a real problem. Businesses that avoid proper adoption do not escape the obligation. They just accumulate hidden non-compliance risk that surfaces during due diligence, audits, or loan applications. Paying attention to integrity in financial reporting is not optional once your business is past the micro-enterprise stage. The tax compliance pitfalls that come from poor financial reporting are avoidable, but only if you set the right foundation from the start.

Pro Tip: Build a simple IFRS for SMEs compliance checklist into your year-end process. At minimum, verify your inventory valuation method, check whether any development costs should be capitalised, and confirm that all required disclosure notes are included in your financial statements. This takes less than an hour and prevents expensive corrections later.

Why these frameworks matter for tax and financial reporting in South Africa

Understanding the differences is not just academic. The right framework has a direct impact on your tax compliance and day-to-day reporting workload. Here is where it gets particularly interesting for South African business owners.

South African tax law does not operate in isolation from IFRS. SARS increasingly uses IFRS-based concepts when interpreting financial results. For example, consolidation principles under IFRS 10 are referenced in tax rules affecting Controlled Foreign Companies (CFCs) and Real Estate Investment Trusts (REITs). The alignment between IFRS principles and SA tax reduces the need for dual reporting, where you produce one set of books for accounting and another for tax.

Here is why this matters in practice:

- Revenue recognition: IFRS for SMEs and SARS share similar logic on when income is recognised. If your accounting is right, your tax position is easier to defend.

- Asset values and depreciation: Using the correct accounting treatment for assets reduces the gap between accounting depreciation and SARS wear and tear allowances, making tax computations more straightforward.

- Provisions and liabilities: SARS does not always allow deductions for provisions in the same year they are raised, but having clean, IFRS-aligned books makes it much easier to track timing differences accurately.

- Audit trail quality: When your financial statements are prepared under the correct standard, the audit trail is cleaner, disputes with SARS are easier to resolve, and the risk of triggering a full audit decreases.

“Principles-based standards like IFRS give accountants and business owners the flexibility to reflect economic reality. Rules-based systems like US GAAP can produce technically correct outcomes that do not always represent what is actually happening in a business.”

Staying on top of reporting irregularities before they escalate is far easier when your accounting framework and tax compliance protocol are aligned from day one. Building that alignment is a core part of any serious tax compliance protocol for South African SMEs.

Is IFRS for SMEs still fit for purpose? A practical view

Here is an honest take, because the standard debate deserves more candour than it usually gets.

IFRS for SMEs is a genuine improvement over requiring every private company to apply full IFRS. The reduction in disclosure requirements alone saves smaller businesses thousands of rands in audit and preparation costs each year. For businesses that need to present credible financial statements to banks, investors, or trade creditors, the framework delivers real value. It signals that your numbers are prepared according to an internationally recognised standard. That credibility has a monetary value when negotiating loan terms or attracting equity investment.

But there is an uncomfortable reality. Many South African SMEs are not sophisticated enough in-house to apply the standard correctly, and the cost of outsourcing that expertise correctly is not trivial. The third edition of IFRS for SMEs brings it closer to full IFRS in several areas, which improves comparability but also risks adding back the very complexity the standard was designed to remove.

Our view is that the framework is fit for purpose for businesses that are genuinely scaling. If you have external funding, multiple shareholders, or aspirations to exit or expand, IFRS for SMEs is not a burden. It is a discipline that forces clarity in your numbers. However, for a sole trader with a simple operation and a PIS well below 100, the cost-benefit ratio shifts. Applying full IFRS for SMEs rigour to a business with three employees and R2 million in turnover creates administrative cost without proportional benefit.

The honest advice is this: invest in getting your framework right once, with proper guidance, rather than patching together a non-compliant set of accounts every year and hoping nobody looks too closely. Good financial reporting practices pay for themselves. The cost of getting it wrong compounds quietly until it does not.

Need help navigating SME accounting standards? Here’s your next step

Sorting out your accounting framework is not a once-off exercise. As your business grows, your PIS changes, your reporting obligations shift, and the complexity of your financial statements increases. At Ready Accounting, we work with South African SMEs to build cloud-based financial infrastructure that produces IFRS for SMEs compliant statements automatically, without manual rework at year-end. If you want to move from reactive compliance to proactive financial control, start by reading our practical guide to improving financial reporting. For businesses ready to remove the manual work entirely, our accounting automation guide shows you exactly how modern cloud accounting replaces outdated bookkeeping with real-time, audit-ready data.

Frequently asked questions

What does GAAP mean for South African small businesses?

GAAP refers to accounting principles broadly, but South African SMEs typically apply IFRS for SMEs, not US GAAP, which has no legal standing in South Africa.

How do I know if my business needs an audit or review?

Calculate your Public Interest Score using your employees, debt, turnover, and shareholders. A PIS above 350 requires a mandatory audit, while lower scores may only require an independent review or nothing at all.

What are the main benefits of using the correct accounting framework?

The right framework improves SARS compliance, simplifies your tax computations, and builds credibility with banks and investors, often making a measurable difference when you apply for funding.

Is IFRS for SMEs mandatory for all South African SMEs?

Not universally. Businesses with a PIS below 100 may use simpler frameworks, but most growing SMEs are required to apply IFRS for SMEs under the Companies Act.

Why is compliance with IFRS for SMEs sometimes low in South Africa?

Many SMEs find the standard difficult to apply without professional support. Less than half of SA SMEs adopted it after its 2007 introduction, even though the standard is only around 230 pages and reduces disclosure requirements by roughly 90%.