Future-proofing your business: strategies for resilience

Executive Summary

- Business resilience depends on combining financial stability, smart automation, and ongoing capability-building, not just technology. Future-proofing involves fostering operational continuity, adaptability, and trust, with continuous management rhythms and scenario planning. Expert support, monitoring key KPIs, and disciplined strategy updates are crucial for long-term success.

Technology alone will not save your business when the economy shifts, load shedding disrupts operations, or a major client cancels overnight. Many South African SME owners invest in the latest software or slash costs at the first sign of trouble, believing that is enough. It is not. True future-proofing combines financial readiness, smart automation, and ongoing capability-building into a system that bends without breaking. This guide gives you practical, research-backed strategies to build that system, so your business stays adaptive and profitable regardless of what South Africa’s volatile environment throws at it.

Table of Contents

- Understanding what it means to future-proof your business

- Building a solid financial foundation for resilience

- Automating for accuracy, insight, and scalable operations

- Measuring what matters: KPIs, benchmarks, and ongoing support

- A smarter, people-focused approach to future-proofing your business

- Where to get expert help with future-proofing and automation

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Resilience means adaptability | True future-proofing combines resilience, adaptability, and continuity, not just cost savings or technology upgrades. |

| Financial discipline is essential | Maintaining a cash buffer, disciplined expenses, and ongoing forecasting are vital for weathering disruption. |

| Automate for value first | Start by automating processes linked to revenue and financial visibility before tackling low-value tasks. |

| KPIs drive long-term success | Use clear financial KPIs and regular benchmarks to guide decisions and measure progress over time. |

| Support networks matter | Mentorship and ongoing support are as crucial as adopting the right tools for business durability. |

Understanding what it means to future-proof your business

Most business owners hear “future-proofing” and immediately think of buying new software or upgrading hardware. That is a narrow view, and it sets you up for disappointment. A business that runs the latest accounting platform but has no cash reserve will still collapse when a debtor pays 90 days late. Real future-proofing is a different conversation entirely.

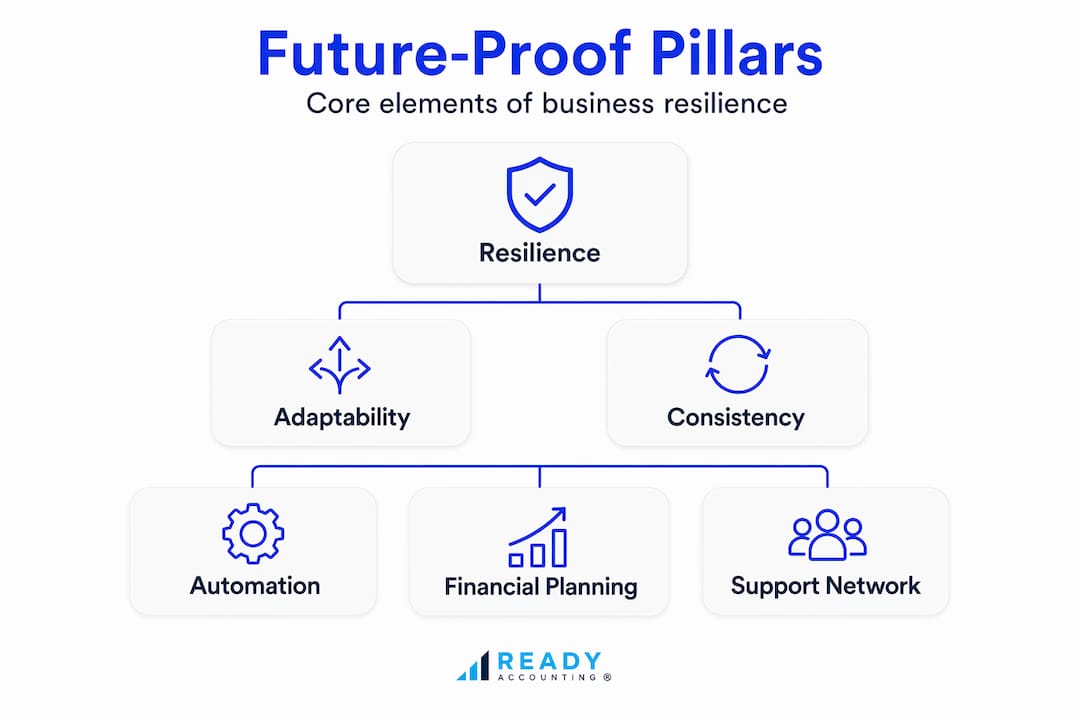

At its core, future-proofing is about building three things simultaneously: resilience, adaptability, and operational continuity. Resilience means your business can absorb a shock without going under. Adaptability means you can change direction quickly when the market demands it. Operational continuity means your core functions keep running even when one or two systems fail.

Future-proofing should combine resilience and adjustability with practical operating continuity under disruption, not just speed or cost-cutting. That distinction matters enormously for South African SMEs operating in an environment where power cuts, currency volatility, and regulatory changes can hit simultaneously.

Here is what genuine future-proofing looks like in practice:

- Building trust with clients, suppliers, and staff so that relationships hold even during difficult periods

- Running low-cost experiments before committing to expensive changes, whether that is a new revenue stream or a new software tool

- Implementing ongoing management rhythms such as monthly cash flow reviews, quarterly strategy sessions, and annual capability audits

- Separating short-term survival moves from long-term positioning decisions

“Future-proofing is not a project you complete. It is an operating discipline you maintain. The businesses that thrive over decades are the ones that treat adaptability as a daily habit, not an annual event.”

Thinking about future-proof payroll strategies and setting strategic financial goals are both practical entry points into this ongoing discipline. Neither is a once-off exercise. Both require revisiting as your business grows and as the external environment evolves.

Building a solid financial foundation for resilience

With the definition clear, the next priority is financial stability. Without it, every other strategy is built on sand. A cash flow crisis does not announce itself with enough warning to improvise. You need structures in place before the storm arrives.

Here is a step-by-step approach to building your financial foundation:

- Build a cash reserve covering 3 to 6 months of operating expenses. This is your single most important buffer. Start small if you must, even one month’s worth gives you breathing room.

- Audit every expense and cut those not directly tied to revenue generation. Subscriptions, software licences, and office perks are often the easiest targets without damaging your core operations.

- Delay major capital expenditure unless it has a clear, measurable payback period. If you cannot calculate the return on a purchase within 12 months, postpone it.

- Implement real-time cash flow monitoring. Knowing your position once a month is too slow. Weekly visibility, at a minimum, lets you spot problems while you still have options.

- Build scenario-based forecasts covering base case, worst case, and best case. Each scenario should model delayed payments, seasonal dips, and currency shifts relevant to your specific business.

A recession-proofing baseline for entrepreneurs starts with protecting liquidity through a cash reserve, tightening non-revenue-critical expenses, delaying major capex, and using real-time cash flow monitoring and forecasting. This is not conservative thinking. It is how businesses survive long enough to grow.

Pro Tip: Do not build just one financial forecast. Build three. Your base case is your most likely outcome. Your worst case assumes your two biggest clients pay 60 days late and one cancels. Your best case models a 20% revenue spike. Knowing all three helps you make faster, calmer decisions under pressure.

Working capital volatility is a specific South African challenge. Managing working capital through forecasting and scenario modelling that accounts for delayed payments, seasonal fluctuations, and load shedding impacts is essential. Digital tools and targeted financing options can help bridge gaps when cash is tight.

Here is a simple view of what scenario-based budgeting looks like for a typical South African SME:

| Scenario | Revenue assumption | Key action |

|---|---|---|

| Best case | +20% growth | Invest in team capacity |

| Base case | Flat or modest growth | Maintain reserves, monitor KPIs |

| Worst case | Major client loss or 60-day delays | Draw on reserve, cut discretionary spend |

Learning practical cash flow forecasting and understanding effective budgeting strategies are the two capabilities that will serve you across every economic cycle you face.

Automating for accuracy, insight, and scalable operations

Once your financial foundation is solid, you can look at operational improvements. Automation is the most powerful lever available to South African SMEs right now, but only when applied correctly. Most business owners start in the wrong place.

The common mistake is automating repetitive but low-value tasks first, things like sending reminder emails or formatting reports. Those automations save a little time. They do not materially change your business’s resilience or growth trajectory.

The smarter approach is to automate revenue-linked workflows first. These are the processes directly connected to cash coming in and cash going out.

Automating payments moves you away from manual payment processing, improves accuracy, and provides real-time cash flow visibility that directly supports liquidity management. That is not a convenience upgrade. That is a structural improvement to how your business operates.

Here is a comparison of manual versus automated approaches to key financial tasks:

| Task | Manual approach | Automated approach |

|---|---|---|

| Payment processing | Human entry, prone to error, delayed visibility | Real-time processing, instant records, reduced errors |

| Invoice generation | Created individually, often delayed | Triggered automatically, sent on schedule |

| Cash flow reporting | Compiled at month end | Updated daily or weekly in real time |

| Debtor follow-up | Chased manually by staff | Automated reminders sent at set intervals |

| Expense categorisation | Done by bookkeeper or owner | Automatically coded via cloud accounting rules |

Automation that future-proofs a business starts with high-impact, revenue-linked workflows such as lead capture, lead follow-up, and booking management, rather than automating lower-value tasks first. That sequencing is critical. Every rand and hour you spend on automation should connect directly to revenue protection or revenue growth.

Key areas where automation delivers the highest return for South African SMEs:

- Invoicing and payment collection: Automated invoicing reduces the gap between work delivered and cash received

- Lead capture and follow-up: No lead falls through the cracks because a team member was busy

- Bookkeeping reconciliation: Cloud tools match transactions automatically, reducing end-of-month scrambles

- Expense tracking: Real-time expense data feeds directly into your cash flow model

- Tax preparation data gathering: Automated record-keeping means fewer surprises at tax time

Pro Tip: Before automating any process, document it manually first. If you cannot describe each step clearly in writing, automating it will simply make a messy process faster and messier. Clean the process, then automate it.

Understanding automation’s impact on cash flow is the foundation. From there, building sustainable financial growth becomes a systematic process rather than a matter of luck or hustle.

Measuring what matters: KPIs, benchmarks, and ongoing support

Effective automation is only half the battle. Knowing whether it is actually delivering value requires tracking the right numbers and comparing them against meaningful benchmarks. Many SME owners track revenue and little else. That leaves you blind to a dozen early warning signs.

The financial KPIs that matter most for resilience are:

- Cash flow position: Updated weekly, not monthly. Know your runway at all times.

- Debtor days: How long does it take clients to pay you on average? Every additional day costs you money.

- Invoicing turnaround: How quickly do invoices go out after work is delivered? Delays here directly delay cash.

- Gross margin by product or service: Are your most popular offerings actually profitable?

- Operating expense ratio: What percentage of revenue goes to running the business before profit?

KPI benchmarks and practical performance metrics such as cash flow, invoicing trends, and payment cycles support future-proofing by turning performance tracking into an ongoing management discipline rather than a once-a-year exercise. Monthly KPI reviews beat annual reviews every time. Problems caught in month two are fixable. Problems caught at year end are often terminal.

The data point worth noting: Ongoing mentorship and business development support, combined with appropriate funding, correlates strongly with business durability and longer-term growth in South African entrepreneurship, not just cash injection alone. This finding underlines something that numbers cannot fully capture: the human dimension of resilience.

Mentorship and support networks matter for three specific reasons. First, an experienced mentor spots patterns you are too close to see. Second, being part of a business network gives you access to supplier relationships, funding leads, and market intelligence that formal channels do not provide. Third, ongoing capability-building, whether through courses, workshops, or peer learning, keeps your decision-making sharp as conditions change.

Pro Tip: Set a quarterly 90-minute “future-proofing review” in your calendar. Check your KPIs against benchmarks, revisit your worst-case scenario, update your cash forecast, and identify one process to improve or automate. Consistency here compounds over time.

Tracking useful SME financial KPIs and improving financial reporting are the practical next steps once your measurement framework is in place.

A smarter, people-focused approach to future-proofing your business

Here is an uncomfortable observation: the South African SMEs we see struggle most are often the ones that bought every software tool available and still could not hold it together when conditions got tough. The tools were fine. What was missing was judgment.

Software does not decide which clients to prioritise when cash is short. Automation does not renegotiate supplier terms during a crunch. A cloud dashboard does not tell you when to hold firm on pricing and when to flex. Those are human decisions, and they require financial literacy, experience, and support.

The “software saviour” mindset is genuinely dangerous because it creates false confidence. Owners assume that once the system is set up, the business runs itself. It does not. Every automated system requires oversight, exception handling, and periodic recalibration. The moment you stop paying attention, the model breaks down.

What actually underpins lasting resilience is a combination of three things working together. First, sound financial practices that give you clarity and control. Second, targeted automation that removes friction from your highest-value processes. Third, ongoing relationships with mentors, advisors, and peers who help you make better decisions faster.

Strategies need to be revisited, not set and forgotten. The forecasting for practical resilience you build today will need updating in six months as your revenue mix shifts, your team grows, or your market changes. The businesses that build genuine durability are the ones that treat strategy as a living document, not a filing cabinet item.

The most resilient business owners we work with are not the ones with the most sophisticated tech stacks. They are the ones who know their numbers cold, review them regularly, and surround themselves with people who tell them the truth.

Where to get expert help with future-proofing and automation

Ready to take the next step? Ready Accounting builds custom financial automation and advisory solutions tailored specifically for scaling South African SMEs and VC-backed startups. We replace manual bookkeeping with cloud infrastructure, real-time dashboards, and API-connected workflows that give you genuine financial control, not just a record of what already happened.

Explore how automation improves cash flow for businesses at every stage, get the full picture with our guide to accounting automation, and see exactly which processes deliver the most value in our breakdown of top accounting tasks to automate. Your finance function should be a competitive advantage. We help you build it that way.

Frequently asked questions

What is the most important first step for future-proofing my business?

Start by building a cash reserve and putting real-time cash flow monitoring in place. A financial baseline that protects liquidity gives every other strategy a stable platform to operate from.

Which business tasks should I automate first for real resilience?

Focus on revenue-linked workflows such as invoicing, payments, and lead management first. High-impact automation on these areas delivers far more business value than automating lower-priority admin tasks.

How much cash reserve should a South African SME keep?

Experts recommend 3 to 6 months of operating expenses in reserve for stability during disruptions. This liquidity buffer gives you time to respond rather than react when conditions deteriorate.

What KPIs should I track to ensure my business is future-proofed?

Track cash flow, invoicing turnaround, and debtor days as your core metrics, and use benchmarks and KPI tracking for ongoing performance management rather than year-end analysis only.

Is mentorship important for future-proofing a business?

Yes, significantly. Ongoing mentorship and support correlates with better business durability and longer-term growth in South African entrepreneurship, beyond what funding alone can achieve.