Forensic accounting: protect your business from fraud

South African businesses lose significant revenue to fraud every year, and small to medium businesses are not immune. Banking fraud losses hit R2.7B in South Africa in 2024, with digital fraud making up 65% of cases. Yet most SMB owners assume forensic accounting is reserved for large corporations or high-profile court cases. It is not. Forensic accounting is a practical, accessible tool that any business can use to detect fraud early, protect assets, and make smarter financial decisions. This guide breaks down exactly what forensic accounting is, how it works, and why it matters specifically for South African SMBs navigating real financial risk.

Table of Contents

- Understanding forensic accounting

- How forensic accountants detect fraud

- The impact of forensic accounting for South African SMBs

- Emerging risks and the future of forensic accounting

- Fresh perspective: what South African SMBs often get wrong about forensic accounting

- Get expert help with business risk and fraud prevention

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Forensic vs. audit | Forensic accounting investigates specific financial crimes, while audits focus on overall statement accuracy. |

| Fraud is widespread | South African SMBs face high fraud risks, often losing up to 5% of revenue annually. |

| Detecting fraud | Forensic accountants use data analytics, digital forensics, and legal evidence gathering to uncover fraud. |

| Prevention is best | Proactive forensic reviews and risk controls can prevent costly losses and protect your business. |

Understanding forensic accounting

Forensic accounting is not your standard year-end audit. It is a specialized practice examining financial records to detect fraud, support litigation, and produce evidence that holds up in court. The word “forensic” literally means “suitable for a court of law,” which tells you everything about its purpose.

Many business owners confuse forensic accounting with regular auditing. They are fundamentally different disciplines. Understanding the difference between accountant and auditor is a useful starting point, but forensic accounting goes even further. Where an audit provides broad assurance over your financial statements, forensic accounting is targeted and investigative. As research into financial fraud detection confirms, forensic work skips materiality sampling entirely and digs into specific transactions with surgical precision.

| Feature | Forensic accounting | Regular auditing |

|---|---|---|

| Purpose | Investigate specific fraud or disputes | Provide overall financial assurance |

| Scope | Targeted, transaction-level | Broad, sample-based |

| Output | Court-admissible evidence | Audit opinion |

| Trigger | Suspicion, litigation, dispute | Annual compliance requirement |

| Approach | No materiality threshold | Materiality-based sampling |

So when would an SMB actually need forensic accounting? More situations than you might think:

- A trusted employee is suspected of skimming cash or manipulating invoices

- A business partner dispute requires independent financial analysis

- You are buying or selling a business and need to verify the books

- A supplier relationship looks financially suspicious

- You face a tax dispute or regulatory investigation

- Insurance claims require documented financial loss evidence

“Forensic accounting shifts the question from ‘are the financials reasonable?’ to ‘what exactly happened, and can we prove it?’ That distinction is everything when money has gone missing.”

For SMBs that rely heavily on trust-based relationships with staff and suppliers, this targeted approach is not overkill. It is protection. Good financial reporting practices form the foundation, but forensic accounting is the safety net when something goes wrong.

How forensic accountants detect fraud

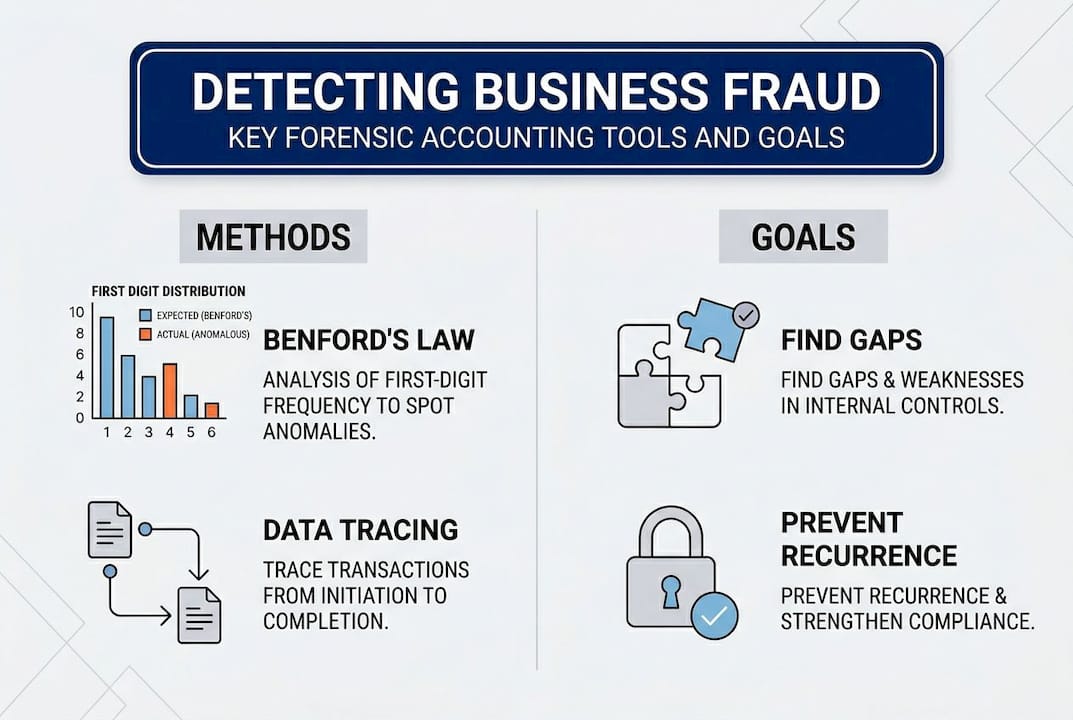

The methods forensic accountants use are far more sophisticated than simply checking receipts. Key methodologies include data analytics, Benford’s Law, transaction tracing, financial ratio analysis, asset tracing, and digital forensics, with specialist tools like IDEA and ACL used for large-scale data mining.

Let us make these practical. Benford’s Law is a surprisingly powerful tool. It states that in naturally occurring financial data, the number 1 appears as the first digit about 30% of the time, while 9 appears only 4.6% of the time. When an employee fabricates invoices, they tend to pick numbers that feel random, which creates a statistical fingerprint that stands out immediately against this expected distribution.

| Technique | What it does | SMB example |

|---|---|---|

| Benford’s Law | Flags statistically abnormal number patterns | Detects fabricated supplier invoices |

| Transaction tracing | Follows money through accounts step by step | Uncovers diverted payments |

| Digital forensics | Recovers deleted files, emails, metadata | Finds evidence of collusion |

| Financial ratio analysis | Spots unusual trends in key business metrics | Identifies unexplained margin drops |

| Asset tracing | Locates hidden or transferred assets | Supports recovery in fraud cases |

A typical SMB fraud investigation follows a structured process:

- Initial briefing to understand the suspected issue and scope the investigation

- Data collection from accounting systems, bank statements, and communication records

- Analysis phase using digital tools to identify anomalies and patterns

- Interview stage where relevant staff are questioned with findings in hand

- Evidence packaging to prepare findings in a format admissible in legal proceedings

- Reporting with clear conclusions and recommendations for internal controls

Pro Tip: Before calling a forensic expert, run a quick pre-screen. Export your supplier payment data and look for duplicate invoice numbers, payments just below approval thresholds, or a surge in payments to a single new vendor. These red flags are often visible in your existing financial statements without any specialist tools.

The goal is not just to catch the culprit. It is to understand how the fraud happened so you can close the gap permanently.

The impact of forensic accounting for South African SMBs

The ACFE estimates organisations lose approximately 5% of annual revenue to fraud. For a business turning over R5 million per year, that is R250,000 walking out the door, often undetected for months or years.

Forensic accounting directly addresses this by delivering measurable, practical outcomes for SMBs. Proactive forensic services help businesses quantify losses accurately, strengthen internal controls, conduct structured fraud risk assessments, and provide litigation support when legal action becomes necessary.

For South African businesses specifically, the regulatory dimension matters too. PRECCA Section 34A creates a corporate liability framework, meaning your business can face consequences if fraud occurs and you failed to implement reasonable preventive measures. King IV governance principles similarly require boards and business owners to take active responsibility for fraud risk. Forensic accounting helps you meet both obligations.

Here is what forensic accounting practically delivers for an SMB:

- Loss quantification: Precisely calculate what was stolen or misappropriated, which is essential for insurance claims and legal recovery

- Risk assessment: Identify which parts of your business are most vulnerable before fraud occurs

- Litigation support: Provide court-ready evidence if you pursue criminal charges or civil recovery

- Control improvement: Get specific, actionable recommendations to close the gaps that allowed fraud to happen

- Regulatory compliance: Demonstrate due diligence under PRECCA and King IV requirements

Pro Tip: When selecting a forensic accountant in South Africa, look for a Certified Fraud Examiner (CFE) designation or a CPA with forensic specialisation. Confirm they understand IRBA guidance and local legislation. Ask specifically about their experience with SMB cases, not just large corporate investigations. Good financial management practices and the right expert together form a strong defence.

It is also worth noting that forensic accounting is not only reactive. Many providers now offer fraud risk assessments as a standalone service, giving you a clear picture of your exposure before anything goes wrong. This is where accounting best practices for SA businesses and forensic awareness genuinely overlap.

Emerging risks and the future of forensic accounting

The fraud landscape is shifting fast, and traditional audits are not equipped to catch the newest threats. Deepfake scams, cryptocurrency fraud, procurement manipulation, and AI-driven financial crime are all growing risks that require specialist forensic skills to detect and investigate.

Here is what South African SMBs are increasingly facing:

- Deepfake voice and video scams impersonating executives to authorise fraudulent payments

- Business email compromise using AI to mimic supplier or management communication styles

- Cryptocurrency-based money laundering making fund tracing significantly more complex

- Procurement fraud involving collusion between staff and vendors, often invisible in standard reports

- AI-generated false documentation that passes visual inspection but fails digital forensic analysis

The shift happening in forensic accounting right now is from reactive to proactive. Rather than waiting for fraud to be discovered, forward-thinking businesses are commissioning regular fraud risk assessments as part of their annual financial cycle. This mirrors how forensic accounting techniques are evolving globally, with data analytics now running continuously rather than being triggered only by suspicion.

“The businesses that will be hardest hit by fraud in the next five years are those still treating forensic accounting as an emergency response rather than a routine control.”

A simple checklist to keep your SMB ahead of evolving fraud risks:

- Review your payment authorisation controls annually

- Implement two-factor verification for all banking transactions

- Train staff to recognise deepfake and email compromise tactics

- Include a fraud risk review in your annual accounting best practices cycle

- Establish a confidential whistleblower channel, since whistleblowers detect nearly 50% of fraud cases

Staying ahead of these threats does not require a large budget. It requires awareness and the right professional relationships.

Fresh perspective: what South African SMBs often get wrong about forensic accounting

Here is the uncomfortable truth: most SMB owners only think about forensic accounting after they have already lost money. By then, recovery is difficult, relationships are damaged, and the business has absorbed a hit that could have been avoided entirely.

The biggest myth we encounter is that forensic accounting is too expensive or complex for a small business. In reality, a targeted fraud risk assessment often costs far less than a single month of undetected employee theft. The maths are straightforward.

Another common misconception is that good bookkeeping is enough protection. It is not. Bookkeeping records transactions accurately. Forensic accounting asks whether those transactions were legitimate in the first place. These are completely different questions.

We have seen cases where a simple annual forensic review would have flagged a payroll ghost employee or a duplicate supplier scheme years before it became a crisis. The proactive integration of forensic services into your regular financial management is not a luxury. It is a practical risk management decision, just like insurance.

The mindset shift we recommend: treat forensic accounting as routine maintenance for your financial health, not as a crisis response. Build it into your financial management strategy the same way you build in tax compliance or cash flow planning.

Get expert help with business risk and fraud prevention

Protecting your business from fraud starts with having the right financial systems and expert support in place before problems arise. At Ready Accounting, we work with South African SMBs to build financial foundations that are both compliant and resilient. Whether you are looking to understand your current exposure or strengthen your controls, our team combines accounting expertise with practical risk awareness. Explore how cloud accounting benefits can improve your financial visibility, read our cloud accounting guide for SMBs, or learn what cloud accounting means for your day-to-day operations. Book a consultation and take the first step toward smarter, safer financial management.

Frequently asked questions

What is the main difference between forensic accounting and auditing?

Forensic accounting investigates specific issues like fraud to produce legal evidence, while auditing provides broad assurance over your overall financial statements. The scope, purpose, and output are entirely different.

When should my business use a forensic accountant?

Hire a forensic accountant when you suspect fraud, face a business dispute, or need court-admissible financial evidence. You should also consider one proactively for an annual fraud risk assessment.

What qualifications should a forensic accountant have in South Africa?

Look for a Certified Fraud Examiner (CFE) or CPA with forensic experience, and confirm they understand IRBA guidance and PRECCA requirements. Local regulatory knowledge is non-negotiable for South African cases.

Can forensic accounting prevent fraud in small businesses?

Yes. Proactive fraud risk assessments and data analytics guided by forensic experts can identify vulnerabilities before they are exploited, significantly reducing your exposure and potential losses.