Boost retention with employee benefits for south african enterprises

Executive Summary

- Small businesses can improve staff loyalty with modest, well-structured benefits.

- Legal minimum benefits include leave, UIF contributions, and minimum wage requirements.

- Effective benefits are modular, affordable, and best communicated to enhance ROI.

Many small business owners in South Africa assume that meaningful employee benefits are reserved for large corporations with deep pockets. That assumption is costing you staff. Even modest, well-structured benefits can dramatically improve loyalty, reduce turnover, and make your business a place people want to stay. Benefits are a necessity, not a luxury, even for a five-person team. This guide walks you through what the law requires, what benefits actually cost, how to design a package that fits your budget, and how to measure the return on your investment as a South African SME.

Table of Contents

- Understanding mandatory employee benefits in South Africa

- Calculating the true cost of employee benefits

- How to design an effective employee benefits package

- Maximising the ROI of your employee benefits

- Why a small business mindset shift beats following big corporate playbooks

- Take the next step: enhance your benefits and financial management

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Legal minimums matter | You must meet South Africa’s statutory benefit requirements to avoid fines and keep staff satisfied. |

| Costs can be strategic | Affordable options like funeral cover or group risk can deliver strong value without breaking the bank. |

| Tailored packages win | Customise benefits to your team’s needs instead of copying big-company playbooks. |

| Strong communication boosts impact | Clear, regular communication drives employee engagement and increases the ROI of your benefits spend. |

Understanding mandatory employee benefits in South Africa

Before you think about extras, you need to know what the law already demands. The Basic Conditions of Employment Act (BCEA) sets the floor for every employment relationship in South Africa, and ignorance of it is not a defence.

Here are the core mandatory benefits under BCEA that every small business must provide:

- Annual leave: 21 consecutive days per year (or 1 day for every 17 days worked)

- Sick leave: 30 days paid sick leave in a 3-year cycle

- Maternity and parental leave: 4 months unpaid maternity leave; 10 days parental leave

- UIF contributions: 1% from the employee, 1% from the employer, capped at the monthly remuneration ceiling

- Work hours: Maximum 45 hours per week for a standard work week

- Overtime: Paid at 1.5 times the normal rate (or 2x on Sundays and public holidays)

- National minimum wage: R28.79 per hour as of the 2026 schedule

| Benefit | Legal minimum | Key notes |

|---|---|---|

| Annual leave | 21 consecutive days | Accrues from day one |

| Sick leave | 30 days per 3-year cycle | First 6 months: 1 day per 26 worked |

| Maternity leave | 4 months unpaid | Cannot be dismissed during leave |

| UIF | 2% of remuneration (split equally) | Capped at statutory ceiling |

| Overtime | 1.5x normal rate | 2x on Sundays and public holidays |

| Minimum wage | R28.79/hour | Updated annually |

Contributions to benefit funds must be paid within 7 days of the end of the month in which they were deducted. Miss that window and you face dual enforcement from both Labour Inspectors and the Financial Sector Conduct Authority (FSCA), with fines reaching up to ZAR 10 million. That is not a typo.

Understanding your small business tax obligations alongside these benefit requirements helps you plan cash flow more accurately. For a practical breakdown of how these obligations feed into your monthly numbers, the payroll management guide is a useful starting point.

Pro Tip: Set a recurring calendar reminder for the 7th of every month to review and confirm that all benefit fund contributions have been submitted. A simple system beats an expensive fine every time.

Calculating the true cost of employee benefits

Once you know what is legally required, the next question is what it will cost your business to provide a fuller benefits package. The numbers are more manageable than most owners expect.

For a typical SME benefits package, you can expect to spend between R5,000 and R10,000 per employee per month when combining statutory contributions with voluntary extras. Here is how that breaks down:

- Audit your current spend. List every deduction and employer contribution you already make per employee.

- Identify gaps. Compare your current offering to what competitors or industry norms suggest.

- Price optional add-ons. Get quotes for gap cover, group risk, and funeral cover from at least two providers.

- Model the total cost. Add voluntary benefit premiums to your existing payroll costs and express it as a percentage of total remuneration.

- Set a benefits budget. Decide what percentage of payroll you can sustainably allocate, then prioritise accordingly.

| Benefit type | Basic package | Comprehensive package |

|---|---|---|

| Statutory (UIF, leave) | Included by law | Included by law |

| Funeral cover | From R45/employee/month | R100–R200/employee/month |

| Gap cover | Not included | R300–R700/employee/month |

| Group risk (life/disability) | Not included | R1,000–R1,500/employee/month |

| Retirement fund | Optional | R500–R1,500/employee/month |

The indirect ROI is where the numbers get interesting. Replacing a single employee typically costs between 50% and 200% of their annual salary when you factor in recruitment, onboarding, and lost productivity. A R500 funeral cover premium that keeps a loyal employee for an extra two years pays for itself many times over. Avoiding common payroll mistakes also protects you from hidden costs that eat into your benefits budget before you even start.

If you are exploring business insurance options alongside staff benefits, some group risk products can be bundled with business cover for better pricing.

How to design an effective employee benefits package

Now that costs are demystified, let us look at how to actually build a package that works for your team and your budget.

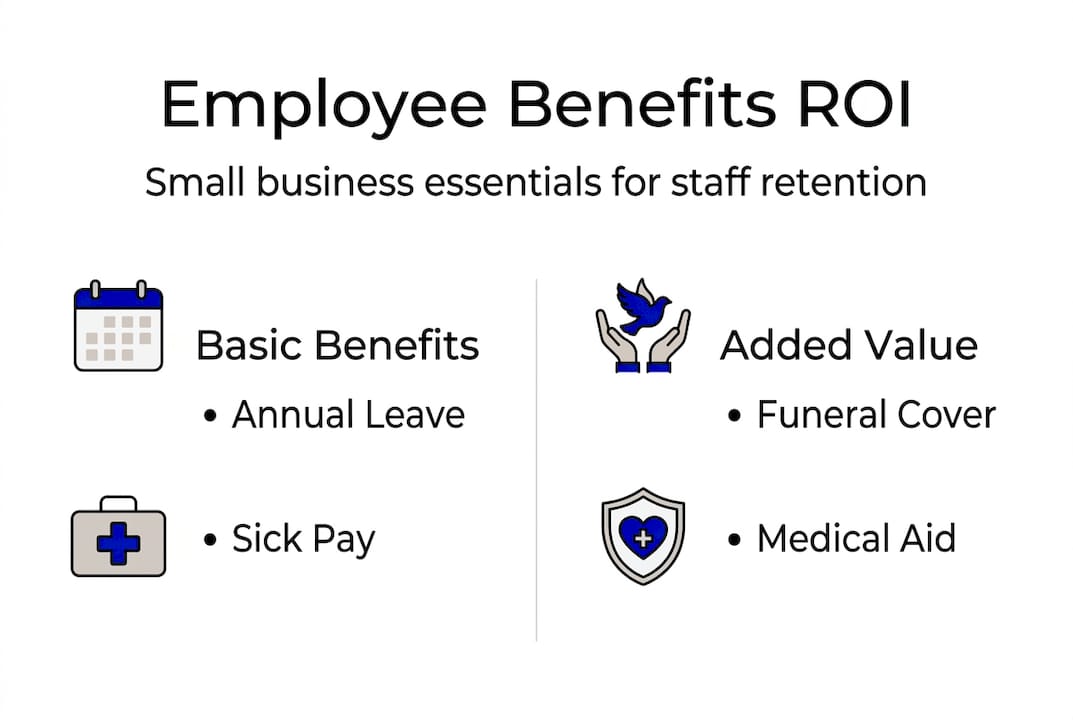

The smartest approach is modular. Start with affordable basics like funeral cover and a basic medical contribution, then add layers as your business grows. You do not need to launch a full corporate benefits suite on day one.

Here are the must-consider options and who they matter most to:

- Funeral cover: High perceived value, low cost. Matters to almost every employee, especially those supporting extended families.

- Group risk (life and disability cover): Critical for employees with dependants. Younger staff often underestimate its value until they see it explained clearly.

- Gap cover: Bridges the shortfall between medical aid payouts and actual hospital bills. Valued by older employees and those with families.

- Retirement fund contributions: Increasingly important for staff in their 30s and 40s. Even a small employer contribution signals long-term commitment.

- Employee wellness programmes: Low-cost mental health and counselling access. Reduces absenteeism and improves morale across all age groups.

Tailoring benefits to your team’s profile makes a real difference. A team of mostly younger employees will respond better to income protection and wellness perks. An older team will prioritise medical and retirement contributions. You do not need to guess: ask them.

“Clear communication is essential. Poor engagement erodes value. A benefit your staff do not understand or trust is a benefit they do not value.”

Pro Tip: Run a short anonymous survey asking staff to rank five benefit options by importance. The results often surprise owners and ensure your spend goes where it genuinely matters.

For group risk cover specifically, reviewing your business insurance options alongside group schemes can reveal bundling opportunities that reduce your per-employee cost.

Maximising the ROI of your employee benefits

Building the right package is only part of the solution. To reap the rewards, you need to maximise benefit take-up and track what you are getting back.

Structured benefits reduce three major business costs: staff turnover, absenteeism, and recruitment. But poor communication erodes value just as fast as a good package builds it. Here is how to make your investment count:

- Set clear ROI goals. Decide upfront what success looks like: lower sick day rates, reduced turnover, higher engagement scores.

- Communicate benefits at onboarding. New employees should receive a simple one-page summary of everything they are entitled to.

- Hold an annual benefits review. Walk the team through their package every year, especially after any changes.

- Measure staff responses. Use short pulse surveys twice a year to track satisfaction with the benefits package.

- Adjust based on feedback. Drop what is not valued, add what staff are asking for, and stay within budget.

Common mistakes that undermine ROI include:

- Under-communicating: Staff who do not know about a benefit cannot value it.

- One-size-fits-all thinking: A package designed for a 25-year-old does not serve a 45-year-old with three dependants.

- Ignoring uptake data: If only 30% of staff are using a benefit, find out why before renewing it.

- Delaying implementation: Waiting until you are “bigger” means losing good people right now.

“Group cover schemes pool risk across your entire team, making benefits far more affordable per person than individual policies. Even a team of five qualifies for group pricing with many providers.”

To streamline payroll operations alongside your benefits administration, automating deductions and contributions reduces errors and saves time every month.

Why a small business mindset shift beats following big corporate playbooks

Here is something most benefits guides will not tell you: copying what large corporates do with employee benefits is one of the most common and costly mistakes small business owners make.

Large companies design benefits for scale, compliance departments, and HR teams. Their packages are complex, layered, and often poorly understood even by the employees who receive them. When a small business tries to replicate that model, the result is usually an expensive, confusing package that staff do not engage with and owners cannot sustain.

What actually works for South African SMEs is simpler and more personal. A small retail business in Durban that introduced funeral cover and a basic wellness benefit saw staff turnover drop noticeably within 18 months, not because the package was impressive on paper, but because the owner explained it clearly, asked staff what they wanted, and delivered on a promise. That kind of trust is worth more than a corporate medical aid.

Think modular. Think affordable. Think communication first. A well-explained R45 funeral cover policy beats a poorly communicated R2,000 medical aid contribution every time. Tools like SimplePay for payroll and benefits make it easier to manage these contributions without a dedicated HR department, keeping your admin lean while your benefits deliver real value.

Take the next step: enhance your benefits and financial management

Smart employee benefits and smart financial management go hand in hand. When your payroll is accurate, your contributions are on time, and your books reflect the true cost of your team, you can make better decisions about where to invest next. Ready Accounting helps South African SMEs do exactly that, from cloud accounting for growth to streamlined payroll management and practical financial guidance. If you are ready to take control of your benefits costs and build a team that stays, explore our cloud accounting guide or book a consultation with our team today.

![CTA Image]

Frequently asked questions

What are the mandatory employee benefits for small businesses in South Africa?

The law requires annual leave, sick leave, UIF, unpaid maternity and parental leave, regulated work hours, overtime pay, and compliance with the national minimum wage for all employees, regardless of business size.

How much should a small business budget for employee benefits?

Expect to spend R5,000 to R10,000 per employee per month for a typical benefits package; funeral cover starts from R45 per employee and gap cover adds R300 to R700 per person.

What happens if I miss benefit fund contribution deadlines?

Missing the 7-day deadline triggers dual enforcement from Labour Inspectors and the FSCA, with fines reaching up to ZAR 10 million for persistent non-compliance.

Which employee benefits give the best ROI for South African SMEs?

Affordable basics like funeral cover and group schemes deliver the highest perceived value per rand spent and have a direct positive impact on staff loyalty and retention.

Recommended

- 7 Cloud Accounting Benefits for Small Business Growth – Ready Accounting

- Tax efficient structures for South African SMBs in 2026 – Ready Accounting

- How to register and use SimplePay – Ready Accounting

- Goal setting for entrepreneurs: strategies to boost success – Ready Accounting

- Employee Retention Solutions, Lower Turnover | OpenElevator

- Unlocking the Benefits of Non-Taxable Employee Perks – Nestlers Group