Debt vs equity financing: what South African SMEs must know

Executive Summary

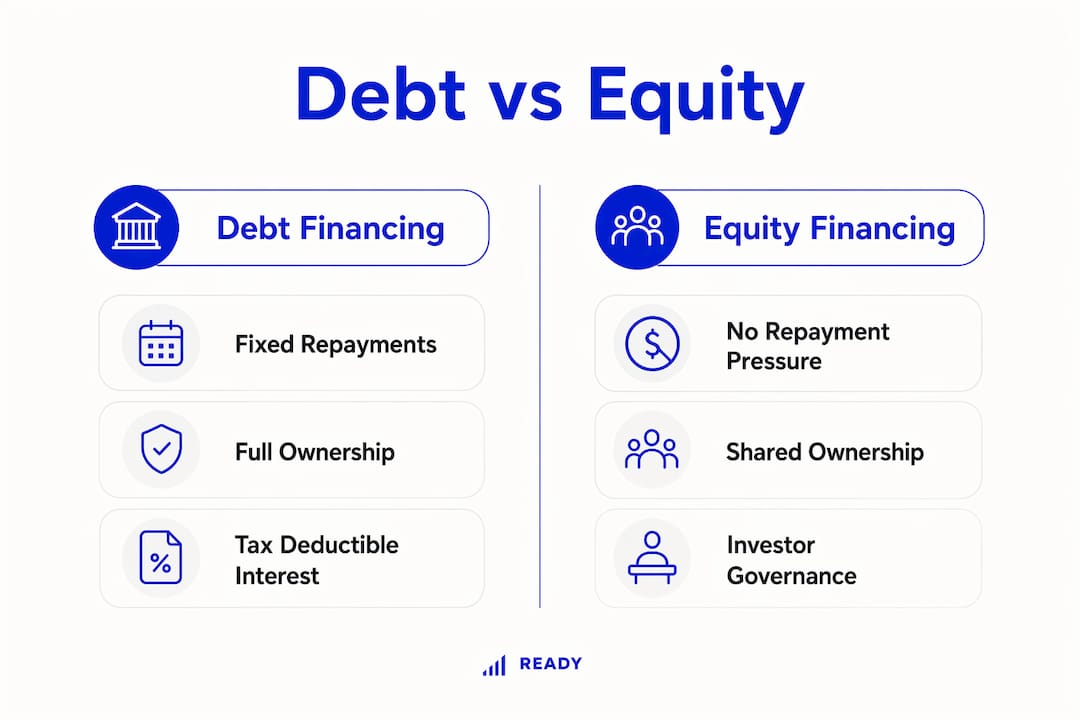

- Debt financing allows South African SMEs to retain full ownership and benefit from tax-deductible interest, but it creates fixed repayment obligations that can pressure cash flow. Equity financing eliminates repayment risks and offers strategic support, but it dilutes ownership and increases governance responsibilities. The best choice depends on the business’s stage, cash flow stability, and growth plans.

Debt vs equity financing is the fundamental choice between borrowing capital with a repayment obligation and selling ownership in your business to raise funds without mandatory repayment. For South African SMEs, this decision shapes your tax position with SARS, your control over day-to-day operations, and your ability to grow through different business stages. Interest on debt is tax-deductible, which lowers your effective cost of borrowing, while dividends paid to equity investors come from after-tax profits and offer no deduction. Getting this choice right from the start protects your cash flow, your ownership stake, and your long-term growth strategy.

What is debt vs equity financing for South African SMEs?

Debt financing means borrowing money from a bank, development finance institution, or alternative lender, then repaying it with interest over an agreed term. Debt carries a stated maturity for repayment, which creates a fixed financial obligation regardless of how your business performs in any given month.

Equity financing means selling a share of your business to an investor, such as a venture capitalist, angel investor, or private equity fund. The investor receives ownership rights and a share of future profits, but you owe them nothing in the form of scheduled repayments. This distinction is the core of capital structure analysis for any SME.

The right choice depends on your business stage, cash flow predictability, and how much control you are willing to share. A bakery with steady monthly revenue faces a very different decision than a tech startup with no revenue yet. Both options have real costs, and neither is universally better.

What are the advantages and disadvantages of debt financing?

Debt financing gives you one powerful benefit above all others: you keep 100% ownership of your business. No investor sits on your board, no shareholder votes on your decisions, and no one shares in your profits once the loan is repaid.

The tax advantage is equally significant. Interest payments reduce your taxable income under SARS rules, which lowers the real cost of the loan. A business paying 12% interest on a loan may effectively pay closer to 8% after the tax deduction, depending on its tax rate. That gap matters when you are comparing the true cost of debt against equity.

Advantages of debt financing:

- Retains full ownership and management control

- Interest payments are tax-deductible, reducing the cost of borrowing

- Repayment terms are fixed and predictable, making financial planning easier

- Common instruments include bank loans, credit lines, and venture debt

- Venture debt allows startups to borrow against investor backing rather than physical assets

Disadvantages of debt financing:

- Fixed repayments create cash flow pressure, especially during slow trading periods

- Debt can force operational cutbacks when revenue dips but repayments remain due

- Lenders often impose covenants that restrict how you run your business

- Covenant breaches can trigger technical default and immediate repayment demands, even if you have never missed a payment

The covenant risk is the most underestimated danger in debt financing. A lender might restrict your ability to take on additional debt, pay dividends, or sell assets. Breaching any of these conditions, even unintentionally, can put your entire loan at risk.

Pro Tip: Before signing any loan agreement, have your accountant review every covenant clause. A single restriction on capital expenditure can block a growth investment you had not yet planned.

What are the advantages and disadvantages of equity financing?

Equity financing removes the pressure of fixed repayments entirely. Equity eliminates default risk associated with scheduled debt payments, which makes it the better fit for businesses with unpredictable or early-stage revenue. A startup burning through its runway does not need a monthly loan repayment adding to the pressure.

Beyond capital, equity investors often bring something debt providers never offer. Investors contribute networks, mentorship, and credibility that can open doors to new clients, partnerships, and future funding rounds. A well-connected investor in your sector can accelerate growth faster than any loan could.

Advantages of equity financing:

- No repayment obligation, preserving cash flow for operations and growth

- Suitable for pre-revenue, early-stage, and high-growth businesses

- Investors bring strategic value beyond capital, including industry networks

- Reduces financial risk during periods of uncertain or volatile revenue

- Strengthens your balance sheet by adding permanent capital without liabilities

Disadvantages of equity financing:

- Dilutes your ownership percentage and voting rights

- Investors require governance involvement, including board reports and milestone reviews

- Founders lose some autonomous decision-making as investor oversight increases

- Profit sharing continues indefinitely, unlike a loan that ends at repayment

- CIPC filings and shareholder agreements add administrative complexity

The governance burden surprises many first-time equity recipients. Reporting to investors, attending board meetings, and justifying strategic decisions takes real time. For a founder who values speed and autonomy, this trade-off deserves serious thought before signing a term sheet.

Pro Tip: When evaluating an equity offer, look beyond the valuation. Ask the investor for three references from founders they have backed. How they behave as a shareholder matters as much as the capital they bring.

How do debt and equity affect your financial statements and SARS obligations?

The financing choice you make shows up directly on your financial statements and changes your tax position with SARS. Understanding these effects helps you read your balance sheet accurately and plan your tax strategy.

With debt, the loan principal appears as a liability on your balance sheet. Interest expense appears on your income statement and reduces your taxable profit. This is the mechanism that makes debt tax-efficient under South African tax law. Your cash flow statement reflects the repayment of principal under financing activities and interest under operating activities.

With equity, no liability appears on the balance sheet. Instead, the investment increases your equity section. Dividends, if declared, are paid from after-tax profits and do not reduce your taxable income. Your income statement impact is therefore higher with equity than with debt, because you lose the interest deduction.

| Financial statement item | Debt financing | Equity financing |

|---|---|---|

| Balance sheet | Increases liabilities | Increases equity |

| Income statement | Interest expense reduces taxable profit | No deduction; dividends paid after tax |

| Cash flow statement | Repayments under financing activities | Dividends under financing activities |

| SARS tax impact | Interest is deductible | Dividends are not deductible |

| Ownership structure | Unchanged | Diluted by investor share |

The practical implication for South African SMEs is clear. If your business is profitable and paying a meaningful corporate tax rate, debt financing delivers a real tax saving that equity cannot match. If your business is pre-profit, that tax benefit is irrelevant, and equity becomes the more logical choice.

Which financing option fits your business stage and growth goals?

Debt suits established SMEs with predictable cash flows, while equity suits pre-revenue or high-growth businesses that cannot support fixed repayments. This is the clearest rule in capital structure analysis, and it holds across most South African SME contexts.

Use this framework to match your financing choice to your business reality:

-

Pre-revenue or early-stage startup. Equity is the right fit. You have no cash flow to service debt, and the governance trade-off is worth the capital injection. Look at angel investors, venture capital funds, or the SEFA (Small Enterprise Finance Agency) equity programmes.

-

Established SME with stable monthly revenue. Debt is the better choice. You can service repayments, you benefit from the tax deduction, and you retain full ownership. Bank loans, credit lines, and asset finance are all accessible options.

-

High-growth SME scaling rapidly. A combination often works best. Use debt for specific assets or working capital where cash flows are predictable. Use equity to fund growth initiatives where the return timeline is uncertain. Managing cash flow during rapid growth becomes the critical skill at this stage.

-

SME facing a cash flow crisis. Neither option is ideal under pressure. Equity investors will demand a lower valuation. Lenders will tighten terms. Addressing the cash flow problem first, before approaching funders, produces better outcomes on both sides.

-

Owner prioritising control above all else. Debt is the only path that preserves 100% ownership. Accept the repayment obligation and manage it carefully. Practical strategies to reduce and manage debt can help you stay on top of obligations without sacrificing growth.

The over-leveraging risk is real. South African SMEs that stack multiple loans without matching revenue growth create a debt service burden that can collapse the business in a single bad quarter. Equity dilution, by contrast, is permanent but does not threaten solvency.

Key takeaways

Debt financing preserves ownership and delivers tax savings through SARS-deductible interest, while equity financing removes repayment pressure but dilutes ownership and introduces investor governance obligations.

| Point | Details |

|---|---|

| Tax efficiency of debt | Interest on loans is SARS-deductible, reducing your effective borrowing cost. |

| Equity removes default risk | No fixed repayments means no technical default, making equity safer for pre-revenue businesses. |

| Covenant risk in debt | Loan covenants can restrict operations and trigger default even without a missed payment. |

| Investor governance trade-off | Equity investors require board reporting and milestone reviews, reducing founder autonomy. |

| Match financing to business stage | Debt fits stable cash flows; equity fits early-stage or high-growth businesses with uncertain revenue. |

What I have learned about financing choices for South African SMEs

Working with South African SME owners, I see the same mistake repeated. Founders treat the financing decision as purely a cost calculation. They compare interest rates to equity dilution percentages and pick the cheaper number. That approach misses the real risk on both sides.

The covenant risk in debt agreements is genuinely dangerous. I have seen profitable businesses forced into technical default because they exceeded a debt-to-equity ratio threshold written into a loan agreement three years earlier. The business was paying every instalment on time. The lender still had the right to demand full repayment. That is a scenario most owners never consider when they sign.

On the equity side, the governance burden grows faster than founders expect. Reporting obligations, investor approvals for major decisions, and board dynamics consume time that should go into running the business. This is not a reason to avoid equity. It is a reason to choose your investors as carefully as you choose your business partners.

The local regulatory environment adds another layer. SARS scrutinises thin capitalisation, which is the practice of loading a business with related-party debt to maximise interest deductions. If your debt structure looks aggressive, expect SARS to look closely. Getting outsourced CFO guidance before you structure a deal can save you from a costly audit later.

My honest advice: assess the long-term strategic fit of your investor or lender before you assess the cost. A patient lender with flexible covenants is worth more than a marginally lower interest rate. An investor who adds genuine sector value is worth more than one who offers a higher valuation.

— Johan

How Readyaccounting helps South African SMEs make smarter financing decisions

Choosing between debt and equity is only the first step. Managing the financial obligations that follow, whether that means tracking loan repayments, reporting to investors, or staying SARS-compliant, requires accurate, real-time financial data. Readyaccounting replaces manual bookkeeping with cloud-based financial infrastructure that gives you a clear picture of your cash position at any moment. Our automation improves cash flow visibility so you can meet repayment obligations, prepare investor reports, and reduce your tax liability with confidence. Contact Readyaccounting to find out how a Fractional CFO approach can support your financing strategy from day one.

FAQ

What is the main difference between debt and equity financing?

Debt financing involves borrowing money that must be repaid with interest, while equity financing involves selling ownership in your business with no repayment obligation. Debt preserves ownership; equity removes repayment pressure but dilutes your stake.

Is interest on a business loan tax-deductible in South Africa?

Yes. SARS allows businesses to deduct interest on qualifying loans from taxable income, which lowers the effective cost of debt financing. Dividends paid to equity investors are not deductible and come from after-tax profits.

When should a South African SME choose equity over debt?

Equity suits pre-revenue, early-stage, or high-growth businesses that cannot reliably service fixed loan repayments. It also suits businesses where the investor’s networks and mentorship add strategic value beyond the capital itself.

What is a debt covenant and why does it matter?

A debt covenant is a condition written into a loan agreement that restricts how you operate your business. Breaching a covenant can trigger technical default and immediate repayment demands, even if you have never missed a scheduled payment.

Can a South African SME use both debt and equity financing?

Yes. Many SMEs use a combination, applying debt for assets or working capital with predictable returns and equity for growth initiatives with uncertain timelines. The key is matching each financing type to the specific use of funds and the cash flow profile it generates.