Business solvency explained: the South African SME guide

Executive Summary

- Many South African SMEs confuse solvency with liquidity, risking severe financial trouble.

- Solvency assesses a business’s long-term ability to pay debts, while liquidity focuses on short-term cash flow.

Many South African business owners treat solvency and liquidity as the same thing. They are not, and confusing the two is one of the most common reasons SMEs run into serious financial trouble. Understanding what is business solvency, as distinct from whether you can cover next month’s salaries, is the difference between a business that survives a rough quarter and one that faces liquidation. This guide cuts through the confusion, gives you the ratios that actually matter, and shows you what to do with that information in a South African context.

Table of Contents

- What is business solvency and why it matters for your SME

- How to measure solvency: key ratios and quick checks

- Solvency versus liquidity: understanding the difference and why both matter

- Practical steps to maintain and improve business solvency in South Africa

- Why traditional solvency metrics might miss hidden risks for South African SMEs

- How Ready Accounting helps South African SMEs stay solvent and compliant

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Solvency definition | Business solvency is the ability to pay long-term debts and financial commitments on time. |

| Measure with ratios | Solvency can be assessed using shareholders’ equity and key ratios like debt-to-equity and interest coverage. |

| Solvency vs liquidity | Solvency focuses on long-term obligations while liquidity covers the short-term ability to pay bills. |

| South African context | Solvency has legal implications for SMEs, affecting directors’ responsibilities and insolvency risks. |

| Maintain solvency | Combine solvency ratios with cash flow forecasts and regular financial reviews to reduce business risk. |

What is business solvency and why it matters for your SME

Business solvency is a company’s ability to pay its long-term debts and financial commitments in a full and timely way. It is not about whether you can pay your electricity bill this Friday. It is about whether your business, when you look at the full picture, owes more than it owns.

Liquidity, by contrast, is the short-term version of that question. A business can be liquid but insolvent (plenty of cash today, but buried in long-term debt it will never repay), or solvent but illiquid (healthy on paper, but no cash available right now). Both matter. But solvency is the deeper measure of financial health, and it carries legal weight in South Africa.

Solvency is closely tied to legal concepts of insolvency under South African liquidation law. Trading while insolvent exposes directors to serious personal risk, including liability for company debts in certain circumstances. This is not theoretical. The Companies Act 71 of 2008 requires directors to ensure the business remains financially sound, and a failure to do so can result in personal liability.

Here is why business solvency deserves your attention as an SME owner:

- Business survival. A business with shrinking equity is on a slow slide toward failure, even if monthly cash flow looks manageable.

- Lender confidence. Banks and invoice financiers assess your solvency before extending credit. Poor solvency ratios mean higher rates or outright rejection.

- Compliance protection. Understanding your director responsibilities for SMEs includes knowing when your business is approaching insolvency and acting before legal thresholds are crossed.

- Investor attraction. No serious investor will back a business without reviewing its solvency position. A clean solvency picture makes fundraising significantly easier.

- Strategic decision-making. Knowing your solvency position informs how aggressively you can borrow, invest, or expand.

How to measure solvency: key ratios and quick checks

Now that you understand why solvency matters, the next question is how to actually measure it. The good news is you do not need a finance degree. You need your balance sheet and a few simple calculations.

The fastest solvency check is shareholders’ equity, which is simply your total assets minus your total liabilities. If the number is positive, your business is technically solvent. If it is negative, you are insolvent, regardless of how busy your business looks.

Beyond that quick check, key solvency ratios give you a sharper picture. Here are the main ones:

| Ratio | Formula | What it tells you | Healthy benchmark |

|---|---|---|---|

| Solvency ratio | (Net income + Depreciation) / Total liabilities | How well earnings cover all obligations | Above 20% |

| Debt-to-equity ratio | Total debt / Shareholders’ equity | How much you rely on borrowing vs. owner funds | Below 2:1 for most SMEs |

| Interest coverage ratio | EBIT / Interest expense | Whether profits cover your interest costs | Above 2x |

| Equity ratio | Shareholders’ equity / Total assets | Percentage of assets financed by owners, not debt | Above 50% |

To illustrate: if your business earns R200,000 net profit, claims R50,000 in depreciation, and carries R1,000,000 in liabilities, your solvency ratio is 25%. That sits in a healthy range. But if you also carry R800,000 in debt against R400,000 in equity, your debt-to-equity ratio is 2:1, which is right at the edge for a small business.

Understanding your balance sheets for SMEs is the foundation for all of this. Without accurate balance sheet data, none of these ratios mean anything.

Pro Tip: Start with the equity check every quarter. If equity is positive and growing, you are moving in the right direction. Once you are comfortable with that, layer in the debt-to-equity and interest coverage ratios for a more complete picture over time.

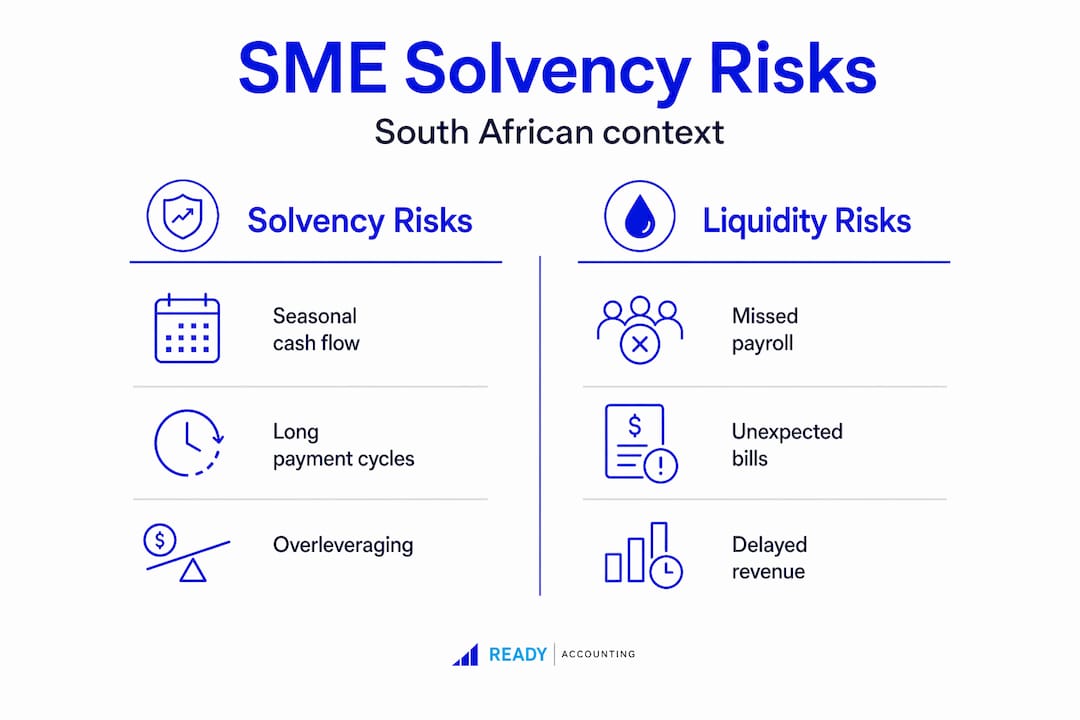

Solvency versus liquidity: understanding the difference and why both matter

These two concepts are often spoken about interchangeably in business conversations, and that is a problem. Solvency looks at long-term ability to pay debts, while liquidity measures your short-term ability to cover bills and expenses. They ask fundamentally different questions about your business.

Here are five core differences every South African SME owner should understand:

- Time horizon. Solvency is a long-term measure, looking at all debts and obligations. Liquidity focuses on the next 30 to 90 days.

- What you measure. Solvency compares total assets to total liabilities. Liquidity compares current assets (cash, debtors, inventory) to current liabilities (creditors, short-term loans).

- Risk type. Solvency risk means your business cannot survive over time. Liquidity risk means you cannot pay someone right now, even if you are fundamentally healthy.

- Key metrics. Solvency uses debt-to-equity and interest coverage ratios. Liquidity uses the current ratio and quick ratio.

- Practical example. A property developer in Cape Town may be perfectly solvent, owning far more than they owe, but illiquid during construction when cash is tied up in the project. A retailer may show strong daily cash flow but carry so much long-term debt that solvency is quietly collapsing.

“Solvency and liquidity are not competing priorities. They are two lenses on the same business. Looking through only one will always leave you partially blind.” This is exactly why SMEs that survive tough economic cycles in South Africa tend to monitor both simultaneously.

A business that ignores liquidity while celebrating solvency can miss payroll. A business that ignores solvency while managing cash flow carefully can still walk into insolvency over 18 months without realising it.

Pro Tip: Pair your budgeting and liquidity reviews with a quarterly solvency check. Cash flow forecasting tells you when problems are coming. Solvency ratios tell you whether those problems are symptoms of something deeper.

Practical steps to maintain and improve business solvency in South Africa

Understanding solvency measures is one thing. Taking action is another. Here are concrete steps tailored for South African SMEs to protect and improve their solvency position.

Start with the foundations:

- Maintain accurate accounting records updated at least monthly. You cannot monitor what you cannot measure, and outdated books will always give you a false sense of security.

- Track your equity trend quarterly. Consistent growth in shareholders’ equity means your business is creating value. Declining equity is a warning sign, even if cash flow feels fine.

- Reduce unnecessary debt. Every rand of long-term debt you carry increases your solvency risk. Prioritise paying down high-interest debt that drags on your ratios.

- Improve profitability first. The solvency ratio directly uses net income. Growing profit margins is the most direct lever you have on your solvency position.

- Negotiate lender terms proactively. If your solvency ratios are under pressure, approach lenders before they approach you. Restructuring repayment terms gives your equity time to recover.

South African law distinguishes between factual and commercial insolvency. Factual insolvency means liabilities exceed assets on the balance sheet. Commercial insolvency means you cannot pay debts as they fall due. You should test both positions before taking on significant new debt.

Combining solvency analysis with cash flow forecasts and debt service schedules is how you avoid being ambushed by financial problems that were visible months earlier.

Here is a simple quarterly solvency health check you can schedule into your calendar:

- Pull your latest balance sheet and calculate shareholders’ equity.

- Compute your debt-to-equity ratio and compare it to the previous quarter.

- Calculate your interest coverage ratio and confirm it is above 2x.

- Run a 13-week cash flow forecast and check for any periods where debt repayments create a shortfall.

- Review your financial reporting for SA SMEs against your tax planning strategies to ensure your obligations are fully accounted for.

Pro Tip: Cloud accounting software that connects to your bank feed in real time gives you balance sheet visibility on demand. You should not need to wait for month-end to know whether your equity is moving in the right direction.

Why traditional solvency metrics might miss hidden risks for South African SMEs

Here is something most financial guides will not tell you: a solvency ratio that looks fine today can still be quietly pointing toward failure. The problem is that most business owners, and even some accountants, treat solvency ratios as pass/fail scores rather than what they really are: trend indicators.

A snapshot of your debt-to-equity ratio on 31 March tells you where you stood at that moment. It tells you nothing about whether that ratio has been creeping upward for six consecutive quarters, which is the pattern that actually predicts distress.

South African SMEs face specific risks that amplify this problem. Uneven cash flows driven by seasonal industries, long payment cycles in sectors like construction and professional services, and currency exposure in import-dependent businesses all create timing mismatches. A business can show positive equity yet still suffer from cash flow timing issues severe enough to trigger commercial insolvency. Your balance sheet does not capture the gap between when you invoice and when clients actually pay.

The practical lesson is this: solvency ratios are most useful when you track them across at least four consecutive periods. A single reading is context-free. Four or more readings reveal a direction. Direction is what matters.

We also see SME owners make the mistake of focusing on one ratio in isolation. A healthy interest coverage ratio can mask a deteriorating equity position if you have refinanced debt at lower interest rates. You need the full set of metrics working together.

Catching these trends early is exactly what common bookkeeping mistakes often prevent. When your books are delayed, inaccurate, or disconnected from your real financial position, you lose the early warning system that solvency trend tracking provides.

How Ready Accounting helps South African SMEs stay solvent and compliant

Knowing your solvency position is one thing. Having the systems to monitor it in real time, and a team that knows what to do with that information, is what actually protects your business.

Ready Accounting builds custom cloud accounting infrastructure that gives South African SMEs real-time cash flow visibility rather than month-old reports. We connect your accounting data directly to dashboards that track your key solvency ratios, equity trends, and debt service positions automatically. The cloud accounting benefits go far beyond convenience: they give you the financial intelligence to act before problems escalate. As your outsourced accounting partner, we handle everything from SARS compliance and VAT submissions to Annual Financial Statement preparation, so your financial records are always accurate enough to trust.

Frequently asked questions

What is the difference between business solvency and liquidity?

Business solvency refers to the ability to pay long-term debts, while liquidity measures the capacity to cover short-term bills and expenses. Both matter, but they operate on different time horizons and use different financial metrics.

How can I quickly check if my South African business is solvent?

Check whether your assets minus liabilities give you a positive shareholders’ equity. A positive figure indicates solvency; a negative figure means your liabilities exceed your assets.

What risks does insolvency present for South African SME directors?

Insolvent trading can expose directors to personal liability and penalties under South African company law, making it essential for directors to monitor solvency continuously.

Why should I track solvency ratios over time instead of just once?

Solvency ratios are trend indicators, not pass/fail scores. Tracking them across multiple periods reveals whether your financial position is improving or deteriorating before problems become critical.

How does cash flow forecasting help with managing solvency?

Combining forecasts with solvency analysis helps you anticipate timing gaps between income and debt repayments, ensuring your business can meet obligations even when it appears solvent on paper.