Balance sheets explained: A South African SME owner’s guide

Executive Summary

- Many South African SME owners focus on income statements, but balance sheets reveal their true financial health.

- Understanding and regularly reviewing balance sheets enables better decision-making, risk management, and funding access.

Most South African SME owners spend their time watching the income statement, checking whether last month was profitable or not. It is a natural instinct. Profit feels real. But the income statement only tells you how your business performed over a period. The balance sheet tells you what your business actually is at this moment: what you own, what you owe, and what is left over for you. Ignoring it is like checking your speed while driving blind to the fuel gauge, oil pressure, and brake warning light. This guide breaks down balance sheets in plain language, with practical applications built for South African business owners who want to grow, not just survive.

Table of Contents

- What is a balance sheet and why does it matter?

- Inside the balance sheet: Breaking down the building blocks

- The South African perspective: Standards, complexity, and challenges

- How to use the balance sheet to grow and safeguard your business

- Why understanding balance sheets is a game changer for South African SME leaders

- Next steps to make financial reporting work for your business

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Snapshot of financial health | A balance sheet reveals what your SME owns, owes, and is worth at a specific point in time. |

| Local standards impact reporting | South African SMEs often follow IFRS for SMEs, but many find it complex and adopt simplified methods. |

| Use for smarter decisions | Regularly reviewing your balance sheet helps you spot risks and opportunities for growth early. |

| Consistency brings value | Applying consistent accounting policies lets you see trends and compare your business with others. |

What is a balance sheet and why does it matter?

A balance sheet is a financial snapshot. It captures your business’s financial position on a specific date, usually the last day of a month, quarter, or financial year. Unlike the income statement, which covers a period of activity, the balance sheet is a single frozen moment in time. Think of it as a photograph of everything your business owns and owes at that exact instant.

The core equation at the heart of every balance sheet is simple:

Assets = Liabilities + Equity

Everything your business owns (assets) is funded either by money you borrowed (liabilities) or by money you and your shareholders put in or earned (equity). This equation must always balance, which is where the name comes from.

For South African SME owners, the balance sheet matters for three concrete reasons. First, it proves solvency. When a bank or investor asks whether your business can repay a loan, the balance sheet answers that question directly. Second, it supports better decisions. Knowing that your short-term debts exceed your short-term assets is a warning you simply cannot get from a profit and loss statement alone. Third, it builds trust with external parties: auditors, financiers, and potential partners all use balance sheets to evaluate credibility.

“A balance sheet is not just a compliance document. It is the clearest signal your business sends to the outside world about its financial health.”

South African SMEs are guided by a specific set of rules when preparing balance sheets. The IFRS for SMEs framework is a simplified version of full International Financial Reporting Standards, and it requires businesses to distinguish between current and non-current items unless a liquidity-based presentation is more relevant to the business’s specific circumstances. It also requires notes covering accounting policies, contingencies, and related-party transactions.

If you are still unsure how the balance sheet fits alongside other reports, a solid financial statements overview will show you how everything connects. You can also explore financial statement examples tailored to South African SMEs to see real-world formats.

Key items that appear on a balance sheet:

- Assets: Cash, debtors (accounts receivable), inventory, equipment, property, and intellectual property

- Liabilities: Creditors (accounts payable), short-term loans, VAT payable, long-term debt, and deferred revenue

- Equity: Share capital, retained earnings, and any reserves

Each of these categories tells a story about your business, and knowing how to read that story is what separates reactive owners from strategic ones.

Inside the balance sheet: Breaking down the building blocks

Once you understand what a balance sheet is, the next step is knowing how to read it section by section. The structure follows a logical order, moving from the most liquid items at the top to the least liquid at the bottom.

Here is how the main categories break down for a typical South African micro-business:

| Category | Line item | Example amount (ZAR) |

|---|---|---|

| Current assets | Cash and cash equivalents | R 45,000 |

| Accounts receivable (debtors) | R 80,000 | |

| Inventory | R 30,000 | |

| Non-current assets | Equipment (net of depreciation) | R 120,000 |

| Vehicles | R 95,000 | |

| Current liabilities | Accounts payable (creditors) | R 55,000 |

| Short-term loan repayment | R 20,000 | |

| Non-current liabilities | Long-term business loan | R 110,000 |

| Owner’s equity | Share capital | R 50,000 |

| Retained earnings | R 135,000 |

Total assets: R 370,000. Total liabilities + equity: R 370,000. The equation holds.

Notice how current and non-current items are separated. This distinction is critical. According to IFRS for SMEs reporting rules, current items are those expected to be settled or realized within twelve months. Non-current items extend beyond that window. If your current liabilities consistently exceed your current assets, you have a liquidity problem brewing, even if your profit looks fine.

Here is a simple numbered process for reading your balance sheet from top to bottom:

- Start with current assets. How much cash do you have? What do your debtors owe you? Is inventory sitting too long?

- Check current liabilities. What do you owe in the next twelve months? Can your current assets cover it?

- Calculate working capital. Subtract current liabilities from current assets. A positive number means short-term breathing room.

- Review non-current assets. Is your equipment aging? Are you investing in long-term capacity?

- Assess long-term debt. Is your total debt growing faster than your equity? That is a structural risk.

- Look at equity growth. Rising retained earnings over time shows a business that generates and keeps value.

For a more detailed walkthrough of this process, reading a balance sheet the right way can shift how you interpret your numbers entirely. You can also compare your layout against established balance sheet examples to ensure your own reporting is structured correctly.

Pro Tip: If your accountant presents your balance sheet in a format that lists everything in order of liquidity rather than separating current from non-current, ask them why. Under IFRS for SMEs, this alternative presentation is allowed when it gives a clearer picture. For businesses with complex cash cycles, it often does.

The South African perspective: Standards, complexity, and challenges

Knowing the rules that govern your balance sheet is not just academic. It directly affects how useful your financial statements are, whether lenders trust them, and how consistently you can track your own performance over time.

Here is a quick comparison of the three reporting approaches South African SMEs commonly encounter:

| Approach | Who uses it | Key feature | Limitation |

|---|---|---|---|

| Full IFRS | Listed companies, large corporates | Highly detailed, globally comparable | Too complex and costly for most SMEs |

| IFRS for SMEs | Medium-sized private companies | Simplified, still rigorous | Still complex for micro businesses |

| Basic cashbook/management accounts | Micro businesses, sole traders | Simple, quick to produce | Not comparable, limited usefulness for funding |

The uncomfortable reality is that fewer than half of SMEs in South Africa adopted IFRS for SMEs after it was introduced in 2007. The primary reason cited was perceived complexity. This matters because inconsistent or non-compliant reporting limits comparability across periods and peers, which directly undermines your ability to use financial data for decisions.

The same research notes that IFRS for SMEs complexity remains a barrier for smaller entities, despite the framework’s simplifications relative to full IFRS. Critics argue it is still not simple enough for very small businesses, and low adoption rates reduce the value of industry-level comparisons.

“Consistent accounting policies applied over time are the foundation of meaningful trend analysis. Without them, your balance sheet numbers are comparable to nothing.”

What should South African SME owners prioritize despite these challenges?

- Consistency above all. Use the same accounting policies every year. Switching methods mid-stream destroys comparability.

- Get the current versus non-current distinction right. It is foundational to understanding liquidity.

- Include supporting notes. Even a brief note explaining your depreciation policy or a related-party loan adds enormous credibility.

- Invest in basic financial literacy. You do not need to be an accountant, but you do need to understand what you are signing off on.

- Seek professional support for first-time preparation. The cost of getting it wrong once is far higher than the cost of getting help upfront.

If you want to understand what integrity in financial reporting actually looks like in practice for local SMEs, there are specific steps that build credibility without overwhelming your team. For a broader foundation, learning to understand financial statements as a business owner, not just a reader, changes how you run your business.

How to use the balance sheet to grow and safeguard your business

Understanding the balance sheet is only half the job. The other half is using it. Here is a structured approach to turning this financial report into an active tool for growth and risk management.

-

Track trends over time. Pull three consecutive balance sheets side by side. Is your cash position improving? Are debtors growing faster than revenue, which could signal collection problems? Is equity expanding, which reflects genuine wealth building? Consistent policy application is what makes this comparison meaningful rather than misleading.

-

Calculate key ratios. Three ratios every SME owner should know:

- Current ratio: Current assets divided by current liabilities. Anything below 1.0 is a red flag.

- Debt-to-equity ratio: Total liabilities divided by total equity. Rising ratios mean growing financial risk.

- Return on equity: Net profit divided by total equity. This tells you how efficiently your business uses owned capital.

-

Benchmark against your industry. Comparing your balance sheet ratios to industry norms reveals whether your debt levels, asset base, or equity position are typical or outliers. Your industry association or a financial advisor can supply benchmark data for South African sectors.

-

Use it to secure funding. When approaching a bank or investor, your balance sheet is often the first document they examine. A clean, well-structured balance sheet prepared under a recognised standard signals that you are a serious operator. It demonstrates that your business is solvent, your debts are manageable, and your equity is real.

-

Spot liquidity risk early. A liquidity crunch rarely appears overnight. It builds over months through rising creditor balances, shrinking cash reserves, and mounting short-term obligations. Monthly balance sheet reviews let you catch these trends while you still have options to act.

-

Align with your income statement. The balance sheet and income statement work together. Rising inventory on the balance sheet paired with flat revenue on the income statement means stock is not moving. Falling equity despite strong profits might indicate undisclosed liabilities. Always read them as a pair. An income statement guide can help you do this comparison more effectively.

-

Connect to your budget. Your balance sheet projections should align with your budgeting for growth targets. If your plan requires significant asset investment, the balance sheet will show whether you have the equity or borrowing capacity to support it.

Pro Tip: Set a fixed review rhythm. Monthly balance sheet reviews work well for businesses with tight cash cycles or rapid growth. Quarterly reviews suit more stable operations. What matters most is consistency. A balance sheet you review every month is infinitely more useful than one you look at once a year during tax season.

Why understanding balance sheets is a game changer for South African SME leaders

Here is the honest truth that most financial advisors will not say out loud: the majority of South African SME owners who struggle to access funding, who get blindsided by cash crises, or who make poor acquisition and expansion decisions are not bad businesspeople. They are people who have been making decisions based on incomplete financial pictures.

Watching only profit and loss is like navigating a city using only yesterday’s weather forecast. It tells you something real, but it misses the terrain completely. The balance sheet is the terrain.

What we see repeatedly in scaling businesses is that the moment an owner truly starts reading their balance sheet, their decision-making quality improves dramatically. They stop confusing revenue growth with business strength. They start asking the right questions before signing leases, taking on debt, or extending credit to customers. They understand that a business can be profitable and still fail if its balance sheet is structurally weak.

The most competitive SMEs in South Africa are not necessarily the ones with the highest revenue. They are the ones with clean balance sheets, growing equity, and a track record of financial consistency that lenders and investors can evaluate with confidence.

A practical balance sheet guide can help you move from passive reader to active strategic user. But the real shift is cultural. When balance sheet literacy becomes part of how you run your business monthly, rather than an annual accounting exercise, it stops being a compliance document and becomes your most reliable growth tool.

Next steps to make financial reporting work for your business

The insights in this guide are the starting point. Implementing them in your business requires the right systems, the right support, and often, a fresh look at how your financial reporting is currently structured. Ready Accounting helps South African SMEs replace manual, inconsistent financial processes with automated cloud infrastructure that delivers real-time balance sheet visibility. If you want to explore improving financial reporting in your business, we can show you exactly where the gaps are. Discover how accounting automation can improve cash flow clarity and reduce administrative burden. You can also review the specific tasks to automate in 2025 to see where technology makes the biggest immediate difference for businesses like yours.

Frequently asked questions

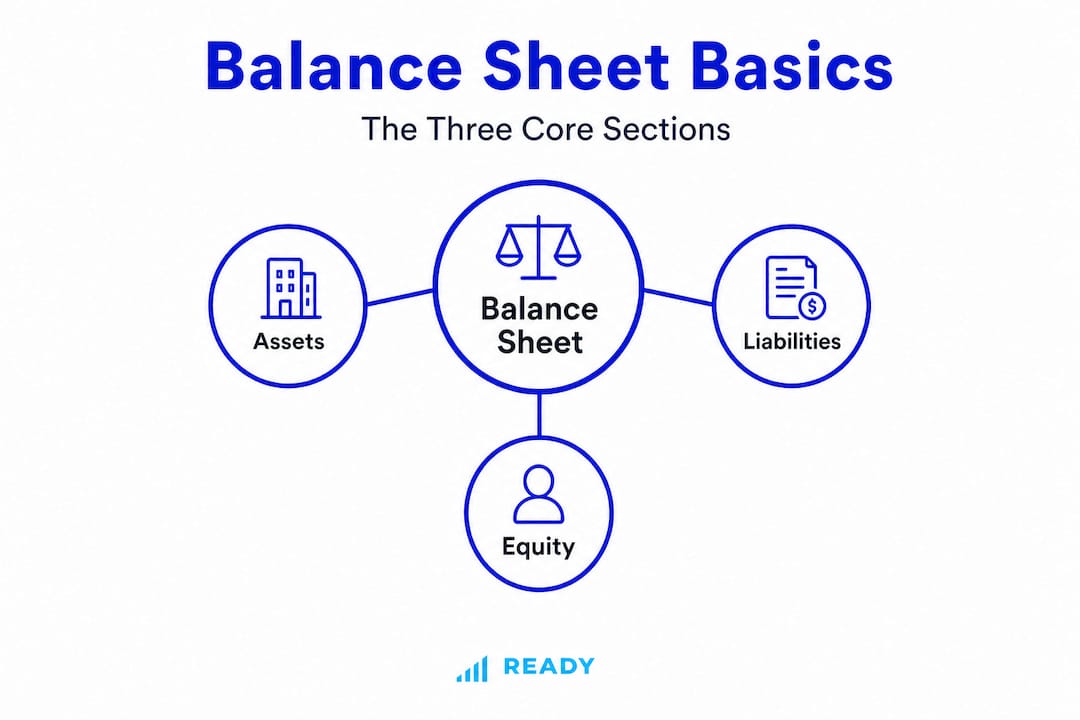

What are the three main sections of a balance sheet?

A balance sheet includes assets, liabilities, and owner’s equity, showing your business’s financial position at a specific date. Under IFRS for SMEs standards, each section is further broken down into current and non-current items.

Do all South African SMEs have to use IFRS for SMEs?

No, adoption is not universal. Less than 50% of SMEs in South Africa adopted IFRS for SMEs due to perceived complexity, meaning many smaller businesses operate with less rigorous reporting standards.

Why are balance sheets important for getting business funding?

They demonstrate your business’s solvency and give lenders a structured view of your ability to meet obligations. A balance sheet prepared under recognised reporting standards signals credibility and financial discipline to banks and investors.

How often should a South African SME review its balance sheet?

Monthly or quarterly reviews help identify risks early and track financial health accurately. The more dynamic your cash cycle, the more frequently you should review it to catch liquidity problems before they become crises.